The Decline of the 60/40 Portfolio: Navigating a New Era of Asset Allocation

The traditional 60/40 portfolio—60% equities, 40% bonds—has been the bedrock of conservative investing for decades. Yet in recent years, this strategy has faltered, leaving investors scrambling to adapt. A confluence of rising interest rates, persistent inflation, and structural economic shifts has eroded the efficacy of bonds as a stabilizing force. For risk-averse investors, clinging to outdated allocations risks prolonged underperformance. This article explores why the 60/40 model is obsolete and outlines actionable strategies to rebuild resilience in a new era.

Why Bonds Are Failing: Rate Hikes, Inflation, and Structural Shifts

The bond market's struggles are no accident. Since 2020, the Federal Reserve's aggressive rate hikes—peaking at 5% for 10-year Treasury yields in early 2024—have inflicted severe losses on long-duration bonds.

Meanwhile, inflation, though now moderating, has reshaped expectations. The 1970s saw inflation hit 14.8%, but today's environment differs. Unlike the wage-price spirals of that era, modern labor markets lack the rigidities to sustain runaway inflation. However, inflation's persistence—averaging 3% in 2023—has eroded bond returns.

Structural shifts amplify these challenges:

1. Deglobalization and Supply Chain Risks: Reduced trade integration and geopolitical tensions have introduced volatility into commodity and energy markets.

2. Central Bank Credibility: Unlike the 1970s, central banks now prioritize inflation control, but high debt levels limit their flexibility.

3. Yield Curve Flattening: By mid-2025, the spread between 10-year and 2-year Treasuries narrowed to 0.44%, reflecting market skepticism about sustained growth.

Historical Context: Bonds in Past Inflationary Eras

The 1970s offer a cautionary tale. While short-term Treasury bills delivered nominal returns (7.7% annually), long-term bonds suffered real losses. Yet even then, alternatives like high-yield (HY) bonds thrived, yielding 9.8% annually due to wide credit spreads and stable defaults.

Today's environment is different:

- Starting Yields Matter: Current bond yields (4–5%) provide better cushions against rate volatility than the sub-2% yields of the 2010s.

- Credit Opportunities: HY bonds now offer 5.4% projected annual returns, but investors must prioritize issuers with strong cash flows and minimal exposure to cyclical industries.

Strategic Alternatives for Risk-Averse Investors

To thrive in this new era, portfolios must diversify beyond bonds and equities. Here's how:

1. Inflation-Linked Assets: TIPS and REITs

- Treasury Inflation-Protected Securities (TIPS): These bonds adjust principal for inflation, shielding investors from purchasing power erosion.

- Real Estate Investment Trusts (REITs): Property prices and rents often rise with inflation, making REITs861104-- a natural hedge. Focus on high-quality, income-generating assets like industrial or healthcare properties.

2. Quality Equities with Defensive Traits

- Dividend Champions: Companies with consistent dividend growth and low volatility, such as consumer staples or utilities, offer equity-like returns with bond-like stability.

- Low-Volatility ETFs: Indices like the S&P 500 Low Volatility Index have historically outperformed the broader market during corrections while maintaining long-term growth.

3. Short-Duration Bond Strategies

- Municipal Bonds: High-tax-bracket investors can benefit from tax-exempt yields, particularly in short-term maturities.

- Structured Credits: Mortgage-backed securities (MBS) and collateralized loan obligations (CLOs) offer yield premiums over Treasuries, provided investors avoid overly complex or leveraged instruments.

4. Dynamic Allocation and Hedging

- Allocate to EM Debt: Emerging market bonds often benefit from higher yields and diversification, but pair them with currency hedging to mitigate volatility.

- Use Options for Insurance: Protective puts or collars can cushion equity exposure without sacrificing upside potential.

The Urgency of Rebalancing

Inaction comes at a cost. Consider this:

- A $1 million 60/40 portfolio allocated to S&P 500 and 10-year Treasuries would have lost 8% in 2022 due to bond declines. By contrast, a portfolio tilted toward TIPS, REITs, and short-term bonds would have held steady.

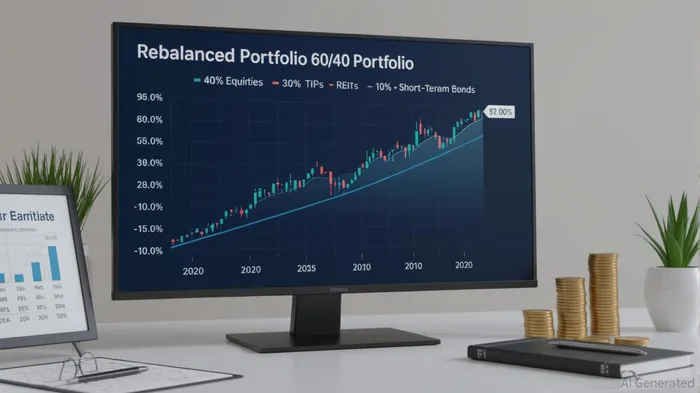

- Over the past five years, the traditional 60/40 has underperformed a mix of 40% equities, 30% TIPS, 20% REITs, and 10% short-term bonds by 2.5% annually.

Conclusion: Embrace a New Paradigm

The 60/40 portfolio is a relic of a simpler time. Inflation, structural shifts, and elevated rates demand a more dynamic approach. Risk-averse investors should:

- Reduce Duration: Cap bond maturities at 5 years to limit interest rate risk.

- Incorporate Inflation Hedges: Allocate 10–20% to TIPS and REITs.

- Prioritize Quality: Focus on stable, cash-generating equities and structured credits.

The market's current range-bound yields and geopolitical risks leave no room for complacency. Rebalancing now is not just prudent—it's essential. As the old adage goes, “Don't just do something, stand there.” In this era, standing still guarantees underperformance.

This article emphasizes actionable strategies supported by historical and contemporary data, urging investors to adapt to a new landscape where diversification and agility are paramount.

Comentarios

Aún no hay comentarios