Decarbonization in Industrial Sectors: Strategic Resilience and Cost-Competitive Innovation

The industrial sector, responsible for nearly a third of global carbon emissions, faces an urgent imperative to decarbonize. For energy-intensive industries like steel, cement, and chemicals, this transition is not merely an environmental obligation but a strategic necessity. As climate policies tighten and markets demand cleaner products, firms must balance decarbonization with cost competitiveness. Recent advancements in resource efficiency, green hydrogen, and AI-driven optimization offer pathways to achieve this balance, but the journey remains fraught with challenges.

Strategic Resilience Through Efficiency and Innovation

Resource and energy efficiency (REEE) remains the cornerstone of near-term decarbonization. By optimizing machinery and processes, industries can slash energy use and material waste without major capital outlays. For example, microwave-driven catalytic upgrading of waste engine oil has increased regenerated oil yields by 30%, while Pt/MXene-enabled CO₂ conversion technologies leverage industrial waste heat to produce methane and carbon monoxide at low temperatures, according to a Deep decarbonization study. These innovations underscore the value of circular economy principles in reducing emissions and costs.

Electrification is another critical lever, particularly in steel production. Electric arc furnaces (EAFs) powered by renewables can cut emissions by up to 99% compared to traditional methods, and emerging technologies like the HIsarna process-paired with carbon capture and storage (CCS)-promise an 80% reduction, according to Powered for Change 2025. Meanwhile, green hydrogen is gaining traction as a clean feedstock and fuel, especially in hard-to-abate sectors. Its adoption, however, hinges on cost parity with grey hydrogen, a target now projected to be achieved six years earlier than previously expected due to multigenerational scaling strategies, according to the same Accenture analysis.

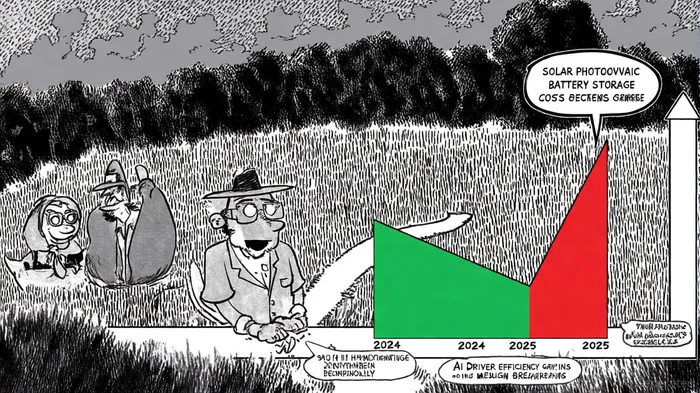

Cost Dynamics: Progress and Persistent Pain Points

The cost landscape for decarbonization is mixed. Solar photovoltaic costs fell by 21% globally in 2024, and battery storage dropped 25% year-on-year, according to Goldman Sachs Research. These declines have pulled the lower end of the decarbonization cost curve downward, with the average cost of abating a ton of CO₂ falling 7% in 2025. However, technologies in hard-to-abate sectors, such as hydrogen-dependent systems, have become 5% more expensive year-on-year, highlighting the uneven pace of progress per the Goldman Sachs analysis.

To bridge this gap, industries are adopting portfolio-driven strategies that prioritize compounding efficiencies. Modular designs and standardized components reduce deployment costs, while AI accelerates knowledge preservation and project execution. For instance, AI-powered tools can personalize stakeholder communication, easing community resistance to large-scale projects, as highlighted in the Accenture report. A strong digital core also enables real-time analytics, allowing firms to optimize operations and predict maintenance needs, further driving down costs, according to the same Accenture report.

Policy and Collaboration: The Missing Link

Despite technological promise, decarbonization requires robust policy frameworks. Governments must incentivize REEE alongside innovation to avoid stranded assets and social disruption, as noted in the Deep decarbonization study. Collaborative efforts, such as joint industry projects and decarbonization roadmaps, are essential for scaling solutions. For example, the European Union's Industrial Decarbonization Strategy provides subsidies for green hydrogen hubs, while China's recent circular economy policies mandate waste-to-energy conversions in key sectors, as reported in a Mechsynergy article.

Investors, too, play a pivotal role. A multigenerational approach-focusing on repeatable systems rather than one-off projects-can unlock compounding returns. Accenture's analysis shows that such strategies can reduce green hydrogen costs by 35% by 2035, achieving price parity with grey hydrogen six years earlier, according to the Powered for Change 2025 report.

Conclusion: A Path Forward

Decarbonization in energy-intensive industries is no longer a choice but a strategic imperative. While cost challenges persist, the convergence of efficiency gains, AI, and policy support is creating a more viable path. For investors, the key lies in backing scalable, modular solutions and fostering cross-sector collaboration. As the Goldman Sachs cost curve suggests, the future of industrial decarbonization will be defined not by a single breakthrough but by the compounding effects of incremental innovation and strategic resilience.

Comentarios

Aún no hay comentarios