Daktronics: Leveraging Small-Cap Exposure and Strategic Visibility to Fuel Growth in a Competitive Market

Daktronics (NASDAQ: DAKT), a leading provider of LED video displays, has emerged as a compelling case study in small-cap growth strategies. The company's recent participation in the Sidoti Small-Cap Virtual Conference on March 19, 2025, underscored its commitment to enhancing investor engagement and leveraging its market visibility to drive long-term value. With a robust order backlog of $342 million at fiscal year-end 2025 and a strategic pivot toward global expansion, DaktronicsDAKT-- is positioning itself to capitalize on its unique strengths in a competitive landscape.

Financial Performance: Mixed Results, Strong Forward Guidance

For Q2 2025, Daktronics reported earnings per share (EPS) of $0.08, aligning with analyst estimates but falling short on revenue, which came in at $172.55 million versus the expected $189.10 million [1]. The trailing EPS remains negative at -$0.44, reflecting ongoing operational challenges. However, the company has reconfirmed its three-year forward sales growth target of 7%-10% and anticipates a 12.5% EPS increase to $1.08 per share in the coming year [1]. These metrics suggest a focus on long-term stability over short-term volatility.

Sidoti Conference: A Strategic Pivot to Global Markets

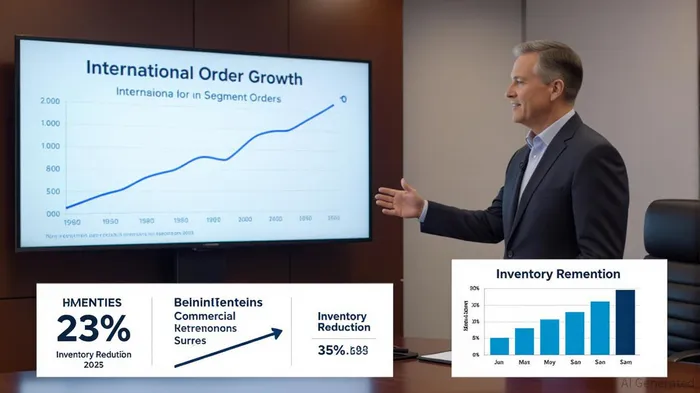

The Sidoti Small-Cap Conference marked a pivotal moment for Daktronics. During its presentation, the company emphasized its leadership as the top North American LED video display provider and third globally, according to FutureSource data [2]. Management outlined a clear strategic vision: enhancing operational efficiency, diversifying revenue streams to mitigate seasonality, and reducing exposure to Chinese tariffs through supply chain optimization [2]. These initiatives align with the company's 23% inventory reduction in FY2025, achieved through manufacturing efficiencies [1].

The conference also highlighted Daktronics' aggressive international expansion. International orders surged by 32% in FY2025, with Q4 orders nearly doubling to $25 million [1]. Commercial segment orders grew 31% for the fiscal year and 44% in Q4, reflecting strong demand in sectors like sports arenas and digital signage [1]. Carla Gatzke, Vice President of Investor Relations, stressed that these gains are critical for sustaining investor engagement and market visibility [1].

Investor Sentiment: Mixed Signals Amid Strong Fundamentals

Despite a recent downgrade from Wall Street to a “Hold” rating, Daktronics retains a “Strong Buy” consensus with an average price target of $26.00 [2]. Analysts at Craig-Hallum reaffirmed their “Buy” rating, citing the company's differentiated market position as the only U.S. manufacturer of scale with a global footprint [1]. This duality in sentiment reflects both caution over near-term revenue shortfalls and optimism about long-term growth catalysts.

Historically, however, a simple buy-and-hold strategy around DAKT's earnings releases has shown limited short-term efficacy. From 2022 to September 2025, 14 earnings announcements were analyzed, revealing that one-day and two-day returns were slightly negative and statistically insignificant. While the average post-event drift over 30 trading days was modestly positive (+7.7%), it lacked statistical significance relative to the benchmark. This suggests that short-term trading based on earnings surprises has not yielded consistent advantages for investors during this period.

Future Outlook: Backlog-Driven Growth and Tariff Resilience

Daktronics' $342 million order backlog, expected to convert into FY2026 revenue, provides a clear runway for growth. The company's strategic focus on reducing inventory and optimizing supply chains—particularly in light of U.S.-China trade tensions—positions it to navigate macroeconomic headwinds [1]. Additionally, record-high orders in the High School Park and Recreation segment (19% YoY growth in FY2025) demonstrate untapped potential in niche markets [1].

Risks and Considerations

While Daktronics' strategic initiatives are promising, investors should remain cautious. The Live Events segment saw a decline in Q4 FY2025 orders, attributed to an atypical delay in baseball season [1]. Management's ability to sustain international growth and execute on acquisition opportunities will be critical.

Conclusion

Daktronics' participation in the Sidoti Small-Cap Conference has amplified its market visibility, aligning with its strategic goals of global expansion and operational efficiency. With a strong order backlog, a clear three-year growth roadmap, and a resilient supply chain, the company is well-positioned to capitalize on its small-cap exposure. For investors seeking long-term value in a sector poised for digital transformation, Daktronics offers a compelling, albeit cautious, opportunity.

Comentarios

Aún no hay comentarios