Daiichi Sankyo's Strategic Reinvention: Assessing Long-Term Value Creation in the ADC Era

Daiichi Sankyo's recent special call on June 2, 2025, underscored its transformation into a global leader in antibody-drug conjugate (ADC) innovation, a position that could redefine its long-term value creation potential. The company's strategic focus on expanding its ADC portfolio, coupled with robust financial performance and strategic partnerships, positions it to capitalize on a rapidly growing market. However, challenges such as developmental delays and competitive pressures necessitate a nuanced evaluation of its trajectory.

ADC Pipeline: A Cornerstone of Growth

Daiichi Sankyo's recent FDA approval of Datopotamab deruxtecan (Datroway) for HR-positive, HER2-negative metastatic breast cancer marks a pivotal milestone in its ADC portfolio[3]. This achievement, alongside the continued success of Enhertu—a HER2-targeting ADC that has redefined breast cancer treatment—highlights the company's ability to address unmet medical needs. As of 2025, the company anticipates top-line results from eight registrational trials, including potential new indications for Enhertu and expanded applications for Datroway[3]. These developments align with its broader strategy to pioneer next-generation ADCs, such as bispecific ADCs, which could further differentiate its offerings in a crowded market[3].

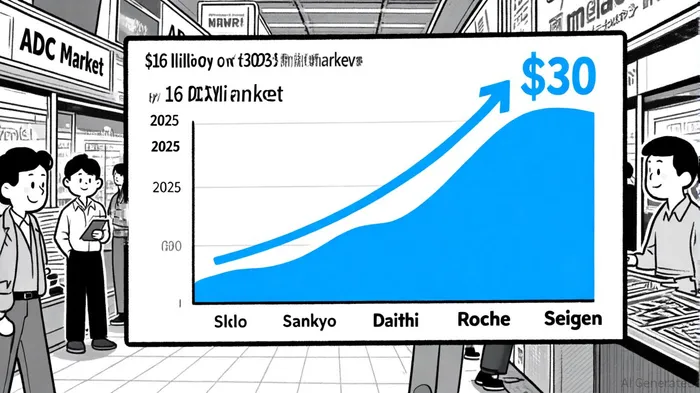

The company's scientific advancements were further emphasized during the special call, where CEO Hiroyuki Okuzawa highlighted data presentations from the AACR 2025 conference, showcasing preclinical and clinical progress in ADC research[1]. This focus on innovation is critical, as the ADC market is projected to surpass $16 billion in 2025 and grow to $30 billion by 2035[2].

Financial Resilience Amid Challenges

Daiichi Sankyo's Q3 FY2025 results demonstrated strong financial resilience, with revenue rising 16.6% year-over-year to ¥1.368 trillion, driven by global oncology sales—particularly Enhertu's performance[1]. Core operating profit increased by 33%, and profit attributable to owners grew by 27.5%, reflecting efficient cost management and pricing power[1]. However, the company acknowledged delays in Datopotamab deruxtecan's development, which have impacted its FY2025 outlook[1]. Despite these hurdles, management remains confident in achieving its five-year strategic KPIs, a testament to its long-term vision[1].

Historically, the market's reaction to Daiichi Sankyo's earnings releases has been mixed. While some reports have driven positive price movements—such as when the company exceeded revenue or profit expectations—others have led to declines, particularly when guidance was cautious or results fell short of forecasts[1]. This variability underscores the importance of aligning investor expectations with the company's evolving pipeline and operational execution.

Strategic Collaborations and Competitive Positioning

Daiichi Sankyo's partnership with MerckMRK-- to co-develop three DXd ADC candidates—patritumab deruxtecan (HER3-DXd), ifinatamab deruxtecan (I-DXd), and raludotatug deruxtecan (R-DXd)—exemplifies its strategy to leverage global commercialization capabilities while retaining exclusive rights in Japan[2]. This collaboration not only diversifies its pipeline but also mitigates risks associated with standalone development.

In a competitive landscape dominated by Roche, Seagen (Pfizer), and AstraZenecaAZN--, Daiichi Sankyo's ADC sales are forecasted to exceed $10 billion by 2029, outpacing Seagen's $5.8 billion and Roche's $3.6 billion[3]. This dominance is attributed to Enhertu's success in targeting HER2-low patients—a previously underserved population—and the company's exclusive ownership of HER3-DXd, which is not shared with AstraZeneca[3]. Analysts at GlobalData note that Daiichi's ability to innovate beyond hematological cancers into solid tumors, such as lung and ovarian cancers, further strengthens its market position[2].

Risks and Opportunities

While Daiichi Sankyo's ADC portfolio is a growth engine, the company must navigate challenges such as developmental delays, regulatory scrutiny, and intense competition. For instance, the recent setbacks in Datopotamab deruxtecan's timeline highlight the inherent risks in ADC development[2]. Additionally, the acquisition of Seagen by PfizerPFE-- could reshape the competitive landscape, potentially intensifying pressure on Daiichi to maintain its edge[3].

However, the company's focus on bispecific ADCs and combination therapies—areas where startups and incumbents are investing heavily—positions it to lead in the next phase of ADC innovation[2]. With eight registrational trials expected to yield top-line data in 2025, Daiichi Sankyo's ability to translate these results into approvals will be critical to sustaining its growth trajectory[3].

Conclusion: A High-Stakes Bet on ADC Leadership

Daiichi Sankyo's strategic reinvention as an ADC leader is underpinned by a robust pipeline, strong financials, and a collaborative approach to innovation. While challenges persist, the company's ability to address unmet needs in oncology and its projected dominance in a $30 billion market by 2035[2] suggest significant long-term value creation potential. For investors, the key will be monitoring the outcomes of its registrational trials and its capacity to maintain its first-mover advantage in a rapidly evolving therapeutic space.

Comentarios

Aún no hay comentarios