CSPC Pharmaceutical's Share Repurchase Strategy: A Test of Capital Allocation Discipline and Investor Confidence

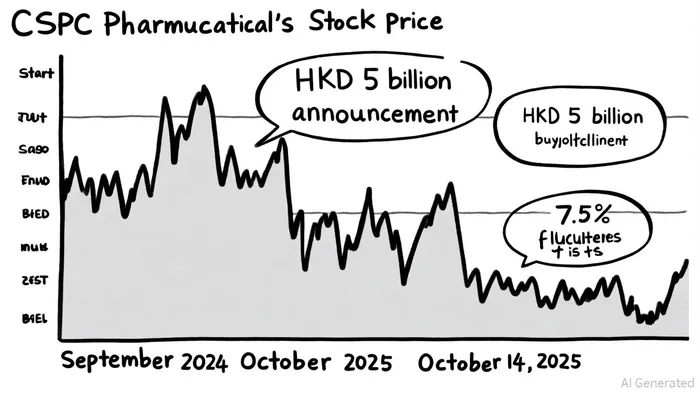

CSPC Pharmaceutical Group Limited's HKD 5 billion share repurchase program, announced in September 2024, represents a bold statement of confidence in its long-term value proposition. By committing to cancel repurchased shares and using cash reserves to execute the buyback, the company signals a disciplined approach to capital allocation-a critical factor for investors evaluating its strategic resilience amid recent financial headwinds. According to a report by Reuters, the program aims to "enhance shareholder returns and stabilize the stock price" by addressing what management perceives as undervaluation[3]. This move aligns with historical patterns where large-scale buybacks, such as Apple's $110 billion 2024 program, have driven immediate market optimism[2]. However, CSPC's case is more nuanced, given its recent revenue and profit declines.

Capital Allocation Discipline: Balancing Past Strength and Present Challenges

CSPC's capital allocation history reveals a company accustomed to aggressive growth. Between 2015 and 2025, it achieved a 25.0% compounded annual growth rate, outpacing GDP growth[3]. This track record, however, contrasts with recent performance: in 2025, revenue fell by 18.5%, and profit attributable to shareholders dropped 15.6%[1]. Despite these declines, the company's free cash flow of RMB 520 million in the last 12 months provides a buffer for the buyback[4]. The decision to prioritize share repurchases over other capital expenditures-such as R&D or debt reduction-raises questions about its strategic priorities. Yet, the cancellation of repurchased shares (64.3 million as of June 2025) directly reduces diluted share count, potentially boosting EPS and signaling a focus on shareholder value over short-term operational expansion[1].

Signaling Effect: Investor Confidence and Market Reactions

The buyback announcement initially bolstered investor sentiment. By August 2025, CSPC had repurchased 1.07% of its shares for HKD 634 million, demonstrating execution speed[6]. Analysts at CLSA upgraded the stock to High-Conviction Outperform, citing improved growth outlooks and recurring revenue streams from R&D-driven innovations[5]. However, the stock's 7.5% drop on October 14, 2025, underscores lingering uncertainties. Technical indicators, including bearish moving averages and a dividend warning, suggest short-term volatility[4]. This volatility contrasts with the broader market's positive reception of buybacks, as seen in Alphabet's $70 billion 2024 program, which drove a 7% stock jump[2].

CSPC's financial health, however, remains a stabilizing factor. With a Debt/Equity ratio of 0.01 and cash reserves of 1.35 billion, the company is well-positioned to sustain the buyback without compromising operational flexibility[2]. Morningstar analysts note that its flagship drug, NBP, and expanding chemotherapy portfolio provide a foundation for future growth[3]. The current P/E ratio of 25.9x, while above industry averages, is still below its estimated fair value of 27.3x, suggesting the market may be cautiously optimistic about its long-term prospects[3].

Long-Term Implications and Risks

The success of CSPC's buyback hinges on two factors: its ability to reverse recent revenue declines and the sustainability of its R&D pipeline. While the company's 25.48% 52-week stock price increase indicates growing investor optimism[2], the 4.9% revenue drop in the first nine months of 2024 highlights structural challenges in its core finished drug and functional food segments[5]. If R&D milestones-such as the approval of new formulations or generics-materialize, the buyback could amplify earnings growth. Conversely, a failure to innovate may render the repurchase a temporary fix for deeper operational issues.

For investors, the key takeaway is that CSPC's buyback reflects a calculated bet on its intrinsic value. While short-term volatility is inevitable, the company's strong balance sheet and strategic focus on share cancellation suggest a commitment to long-term capital discipline. As CLSA analysts argue, the buyback is not just a financial maneuver but a signal of confidence in CSPC's ability to navigate a competitive pharmaceutical landscape[5].

Comentarios

Aún no hay comentarios