U.S. Crypto Regulatory Developments and Market Implications: How New Laws Catalyze Institutional Adoption and Bullish Momentum

The U.S. crypto landscape in 2025 has undergone a seismic shift, driven by landmark legislative reforms that are reshaping institutional participation and market dynamics. The GENIUS Act and CLARITY Act, signed or advanced in 2025, have provided long-awaited regulatory clarity, reducing ambiguity and fostering a framework that aligns digital assets with traditional financial systems. These developments are not merely procedural—they represent a tectonic shift in how institutions perceive and engage with crypto, unlocking new avenues for innovation, capital flows, and systemic integration.

Regulatory Clarity as a Catalyst for Institutional Adoption

The GENIUS Act, enacted in July 2025 under President Trump, has redefined the stablecoin market by mandating 100% reserve backing with high-quality liquid assets such as U.S. dollars or short-term Treasuries[1]. This requirement has transformed stablecoins from speculative instruments into trusted, institutional-grade assets. For example, JPMorgan ChaseJPM-- and CitigroupC-- have launched stablecoin-based services—JPMD and CitiC-- Token Services—leveraging the Act's legal certainty to streamline cross-border payments and enhance liquidity[3]. According to a report by Cointelegraph, the Act has also spurred the creation of “institutional-grade stablecoin integration” for programmable treasury instruments and DeFi applications[4].

The CLARITY Act, passed by the House with bipartisan support, further solidifies this momentum by delineating jurisdiction between the SEC and CFTC. By classifying digital assets as either securities or commodities, the Act eliminates regulatory overlap and provides a clear compliance pathway for institutions[2]. This clarity has already prompted major players like Fidelity Investments and Franklin Templeton to deepen their engagement with stablecoins[4]. As noted by the EY Parthenon 2025 survey, 84% of institutional investors are now using or planning to use stablecoins, citing their superior risk-return profiles and inflation-hedging potential[5].

Market Performance and Institutional Capital Flows

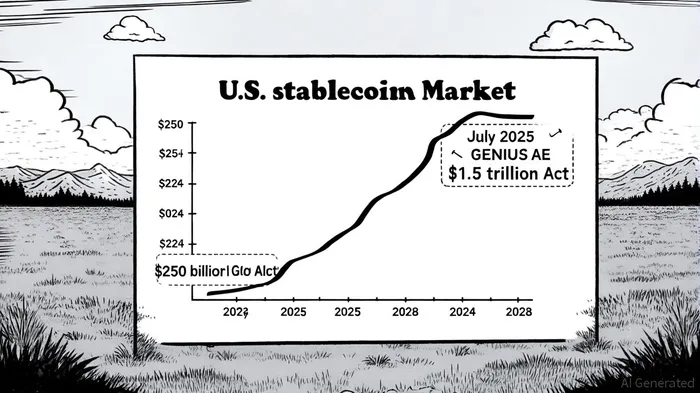

The regulatory tailwinds are translating into tangible market outcomes. The U.S. stablecoin market, valued at $250 billion in early 2025, has surged to $208 billion in circulation, facilitating over $4 trillion in transactions—a 45% year-over-year increase[4]. USDCUSDC--, in particular, has seen its market cap reach $60 billion, driven by institutional demand for its compliance with the GENIUS Act[4]. Meanwhile, Tether's USDTUSDT--, though still dominant at $144 billion, faces growing competition from federally regulated alternatives.

Institutional capital is flowing into stablecoins at an unprecedented rate. Q3 2025 data reveals $47.3 billion in institutional stablecoin deployments, with 58.4% allocated to lending protocols and 26.8% to real-yield products[1]. Conservative institutions, such as pension funds, favor overcollateralized lending on platforms like Anchorage Digital Bank, the first federally chartered stablecoin issuer post-GENIUS Act[1]. Aggressive strategies, including yield farming and leveraged positions, are being pursued by crypto-native funds and family offices, further diversifying the market's risk profile.

Systemic Implications and Broader Market Impact

The rise of stablecoins is not confined to the crypto ecosystem—it is influencing traditional financial markets. A report by the Bank for International Settlements (BIS) highlights that stablecoin inflows reduce three-month U.S. Treasury yields by 2–2.5 basis points within 10 days, while outflows can raise yields by 6–8 basis points[5]. This demonstrates stablecoins' growing role as safe-haven assets and their potential to act as a liquidity buffer in times of stress.

Moreover, the GENIUS Act's emphasis on AML/KYC compliance and reserve transparency has elevated stablecoins to a level of institutional trust previously reserved for sovereign debt. As noted by Arnold & Porter, the Act prioritizes stablecoin holder claims in insolvency, a critical factor for institutional investors seeking legal recourse[1]. This has spurred innovation in hybrid TradFi-DeFi solutions, such as retrieval-augmented finance (RAF) protocols that tokenize short-term Treasury yields[1].

Challenges and the Road Ahead

Despite these gains, challenges persist. The Anti-CBDC Act, which seeks to block a U.S. central bank digital currency (CBDC) without congressional approval, introduces uncertainty around privacy and innovation[3]. Additionally, tax policies and international coordination remain unresolved, with regulatory arbitrage a risk if other jurisdictions lag in reform.

However, the momentum is undeniable. With the stablecoin market projected to reach $1.5 trillion by 2028[5] and institutional allocations expanding, the U.S. is positioning itself as the global leader in crypto innovation. The GENIUS and CLARITY Acts have not only mitigated risks but also created a fertile ground for sustained adoption, bridging the gap between traditional finance and the digital asset revolution.

Comentarios

Aún no hay comentarios