Crypto Market Volatility and Exchange Risk Management: Lessons from Binance's $300M Payout and Liquidity Stress Testing

The October 2025 Crash: A Case Study in Systemic Fragility

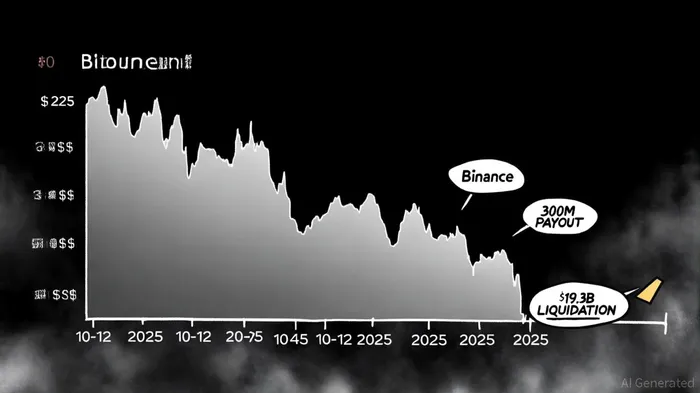

The crypto market's volatility reached a boiling point on October 10, 2025, when a confluence of macroeconomic shocks—President Trump's 100% China tariff threat, a global carry trade unwind, and yen appreciation—triggered the October Crypto Crash of 2025, a $20 billion liquidation event. Binance, the largest exchange by spot trading volume, became the epicenter of this crisis. Synthetic stablecoins like USDeUSDe-- and BNSOLBNSOL-- depegged, while algorithmic price distortions exploited vulnerabilities in Binance's updated pricing mechanisms, creating a self-reinforcing selloff, which preceded Binance's $300M payout.

Binance's response—a $300 million compensation plan under its "Together Initiative"—was both a lifeline for affected traders and a PR maneuver to restore trust. However, the payout raised critical questions about risk management. By reimbursing users who lost 30% or more of their net assets, Binance inadvertently created a moral hazard: traders might now assume exchanges will bail them out during crises, encouraging riskier leverage use, according to a Onesafe analysis. This is compounded by the fact that Binance's auto-deleveraging mechanisms, designed to stabilize markets, instead accelerated the selloff by triggering cascading liquidations, as noted in a Brave New Coin analysis.

Liquidity Stress Testing: A Missed Opportunity?

Traditional financial institutions have long used liquidity stress testing to prepare for extreme scenarios. The U.S. Federal Reserve's 2025 stress test scenarios, for instance, simulate severe global recessions and asset price collapses to evaluate banks' resilience. Yet, crypto exchanges like Binance have lagged in adopting similar frameworks. The October 2025 crash exposed this gap: Binance's liquidity buffers and margin systems were unprepared for a $19.3 billion liquidation event, leading to frozen accounts, failed stop-loss orders, and flash crashes, according to a ScienceDirect article.

Academic research underscores the importance of integrating solvency and liquidity risk in stress testing. For example, kurtosis-based models, which account for fat-tail risks in crypto markets, could have flagged the likelihood of a Terra-style collapse in synthetic stablecoins like USDe. Binance's failure to apply such methodologies highlights a broader industry issue: many exchanges prioritize growth over robust risk controls, assuming they can "compensate" their way out of crises rather than prevent them.

The Binance Paradox: Compensation vs.

Systemic Stability

Binance's $300 million payout and $283 million depegging compensation were lauded as gestures of goodwill, according to a Decrypt report, but criticized for their limited scope. The exchange excluded losses from normal market movements, leaving many traders uncompensated. Worse, the payout window (24–96 hours) coincided with ongoing volatility, forcing users to navigate a chaotic redemption process. This inconsistency eroded trust, with critics arguing that Binance's actions prioritized reputation management over systemic stability.

The incident also revealed a strategic misstep: while Binance dominates spot trading volume, platforms like Gate.ioIO-- and OKX outperformed it in BTC liquidations during the crash. This was not due to superior risk management but to liquidity dynamics—exchanges with faster position unwinding mechanisms became default venues for distressed traders. Binance's reliance on legacy systems, in contrast, left it vulnerable to cascading failures.

Implications for the Future of Crypto Risk Management

The October 2025 crash serves as a wake-up call for the industry. Regulators, including the European Banking Authority (EBA) and Basel Committee, are now pushing for crypto-specific liquidity stress testing frameworks under MiCAR and global banking standards. These will likely mandate scenario analyses for extreme price drops, stablecoin depegging, and algorithmic manipulation risks.

For exchanges, the lesson is clear: compensation payouts are not substitutes for proactive risk management. Binance's recent steps—introducing minimum price thresholds for stablecoins and increasing risk parameter reviews—are a start, but more is needed. Exchanges must adopt real-time on-chain analytics, machine learning-driven volatility forecasts, and diversified liquidity buffers to withstand future shocks.

Conclusion: A Call for Institutional Maturity

The crypto market's volatility is here to stay, but its systemic risks can be mitigated. Binance's $300 million payout, while symbolic, underscores the need for institutional maturity in risk management. As traditional finance increasingly engages with crypto, exchanges must align with global stress testing standards to avoid becoming the next FTX. For investors, the takeaway is simple: diversify leverage exposure, scrutinize exchange risk disclosures, and prepare for worst-case scenarios. In a market where liquidity can vanish overnight, preparedness is the only safety net.

Comentarios

Aún no hay comentarios