CrowdStrike's Long-Term Growth Potential: Navigating Cybersecurity Tailwinds and Market Positioning

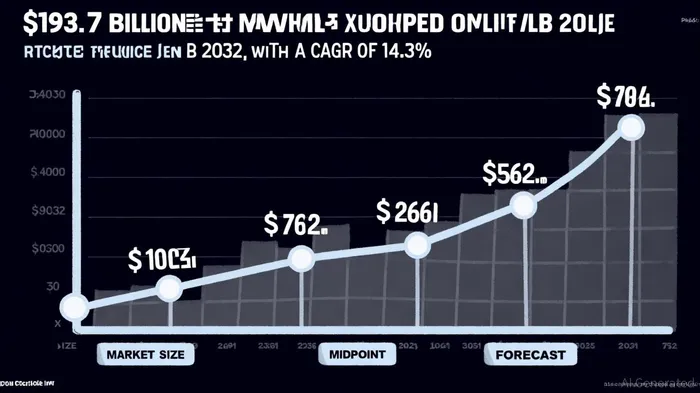

The cybersecurity industry is undergoing a seismic shift, driven by escalating cyber threats, digital transformation, and technological innovation. As the global cybersecurity market expands from $193.7 billion in 2024 to an estimated $562.7 billion by 2032[1], companies like CrowdStrikeCRWD-- (NASDAQ:CRWD) are positioned to capitalize on this tailwind. However, investors must weigh the firm's long-term potential against competitive pressures and valuation concerns. Recent analysis from Mizuho Securities offers a nuanced perspective, raising its price target for CrowdStrike to $475 while maintaining a "Neutral" rating[2].

Cybersecurity Tailwinds: A Boon for CrowdStrike

The cybersecurity market's 14.3% CAGR[1] is fueled by three key drivers:

1. Escalating Cyber Threats: The FBI's Internet Crime Complaint Center reported 880,418 complaints in 2023 alone[3], a 10% increase from 2022. As attacks grow in frequency and sophistication, demand for advanced solutions like CrowdStrike's Falcon platform—designed for endpoint detection and response (EDR)—is surging.

2. Digital Transformation: Cloud adoption, IoT proliferation, and 5G deployment are expanding attack surfaces. Cloud security, a segment expected to grow faster than the overall market[4], aligns with CrowdStrike's strategic pivot into cloud application security and identity protection.

3. AI Integration: Artificial intelligence and machine learning are revolutionizing threat detection. CrowdStrike's AI-driven threat intelligence and Microsoft's AI-powered Defender for Cloud exemplify this trend, with generative AI enabling real-time anomaly detection[5].

Mizuho's Upgrade: Confidence in CrowdStrike's Execution

Mizuho's price target increase to $475 reflects optimism about CrowdStrike's ability to outperform industry benchmarks. At the Fal.Con 2025 investor meeting, the company guided for over 20% net new ARR growth in fiscal 2027[2], significantly exceeding consensus estimates. Mizuho praised CrowdStrike's "very differentiated" cloud security platform and its go-to-market strategy, which emphasizes cross-selling into higher-growth markets like identity and cloud workload protection[2].

However, the firm's "Neutral" rating underscores caution. Moderated channel checks in recent quarters—likely due to the July 2024 outage that disrupted 8.5 million Windows machines[6]—and a valuation of nearly 20x 2026 estimated enterprise value to ARR[2] create a "balanced risk/reward profile." This suggests that while CrowdStrike's fundamentals are strong, investors should remain mindful of execution risks and valuation multiples.

Competitive Landscape: Strengths and Vulnerabilities

CrowdStrike's dominance in endpoint security is well-established, with its Falcon platform adopted across industries. Yet, the market is fiercely competitive:

- SentinelOne leverages autonomous AI and partnerships (e.g., with Lenovo[6]) to attract clients seeking alternatives post-2024 outage.

- Microsoft Defender for Endpoint benefits from deep integration with Windows environments and cost advantages for Microsoft 365 users[6].

- Palo Alto Networks differentiates with Cortex XDR, which correlates network, endpoint, and cloud data to detect sophisticated threats[6].

Despite these challenges, CrowdStrike's leadership in threat intelligence and its first-mover advantage in cloud security provide a moat. Its 34.26% year-over-year revenue growth to $3.28 billion in the twelve months ending April 2024[6] underscores its ability to scale.

Valuation and Market Volatility: A Double-Edged Sword

CrowdStrike's valuation remains a point of contention. At 20x 2026 EVA/ARR[2], it trades at a premium to peers like SentinelOne (15x) and Palo Alto (12x). This premium reflects high expectations for its cloud and AI initiatives but also exposes the stock to volatility during macroeconomic downturns or earnings misses.

The broader market's sensitivity to interest rates and tech sector cyclicality further complicates the outlook. While cybersecurity is a defensive sector, CrowdStrike's growth story hinges on reinvestment in R&D and M&A, which could strain margins if execution falters.

Conclusion: A Long-Term Play with Caution

CrowdStrike's long-term growth potential is anchored in the cybersecurity industry's structural tailwinds and its leadership in endpoint and cloud security. Mizuho's upgraded price target signals confidence in the company's ability to deliver above-consensus ARR growth, but the "Neutral" rating serves as a reminder of the risks. Investors should monitor CrowdStrike's ability to retain clients post-2024 outage, execute its cloud and AI strategies, and manage valuation expectations. For those with a multi-year horizon and a tolerance for volatility, CrowdStrike remains a compelling, albeit cautious, bet in the cybersecurity space.

Comentarios

Aún no hay comentarios