CrowdStrike's Investor Day Guidance and Its Implications for Cybersecurity Growth: Assessing the Sustainability and Scalability of Key Metrics

CrowdStrike's 2025 investor day guidance has ignited a critical debate among investors: Can the cybersecurity leader sustain its hypergrowth in a maturing market? The company's updated roadmap, financial targets, and strategic bets on AI and quantum-resistant tech suggest a nuanced answer.

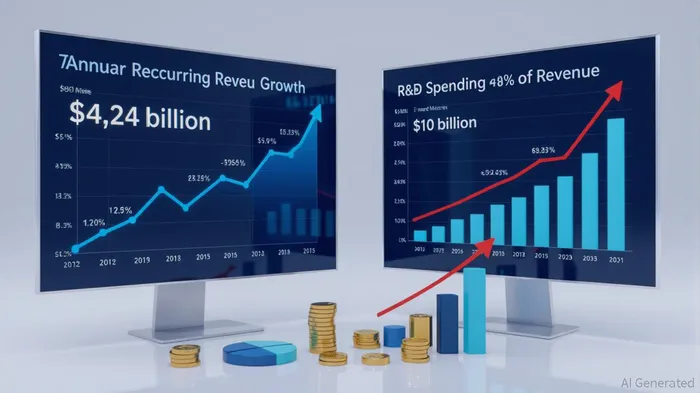

Revenue Projections and ARR Growth: A Double-Edged Sword

CrowdStrike reported $4.24 billion in ARR for fiscal 2025, a 23% year-over-year increase, with $224.3 million in net new ARR added in Q4 alone[2]. CEO George Kurtz's $10 billion ARR target by 2031 implies a compound annual growth rate (CAGR) of ~14% from 2025 to 2031—a steep slope for a company already dominating the endpoint security space. While the Falcon platform's modular design drives cross-selling (66% of customers use five or more modules[4]), the core endpoint market's slowing growth could constrain scalability.

The company's short-term optimism hinges on AI-driven threat detection and XDR expansion. For instance, Charlotte AI Detection Triage and Falcon Identity Protection for MicrosoftMSFT-- Entra ID aim to monetize niche use cases[2]. However, these innovations must offset declining growth in legacy endpoint segments.

Customer Retention: Resilience Amid Crisis

CrowdStrike's gross retention rate of 97% in Q4 2025[1] underscores its platform stickiness, but the dollar-based net retention rate dipped to 115% in Q3 2025, down from 125% in 2024[2]. This decline, attributed to the July 2024 global IT outage caused by a faulty CrowdStrikeCRWD-- update[4], highlights a vulnerability: over-reliance on a single platform. Yet, the cybersecurity industry's average retention rate of 71%[3] pales in comparison to CrowdStrike's performance, suggesting its land-and-expand strategy remains robust.

R&D Investment: Fueling Innovation or a Costly Gamble?

CrowdStrike allocated 27% of Q3 2025 revenue to R&D[2], a 40% year-over-year increase in total spending ($1.077 billion in 2025)[6]. This commitment to innovation is critical in a sector where AI and quantum-resistant cryptography are becoming table stakes[3]. However, investors must weigh whether these investments will translate into sustainable margins. For context, the cybersecurity sector's average R&D spend is ~15–20% of revenue[5], making CrowdStrike's approach aggressive but potentially necessary for long-term differentiation.

Competitive Landscape: Leadership Under Pressure

CrowdStrike's 20.65% market share in endpoint protection[2] dwarfs competitors like McAfee (16.47%) and Microsoft Defender (10.85%). Yet, the July 2024 outage exposed systemic risks of platform-centric security strategies[4]. Meanwhile, rivals like Palo Alto NetworksPANW-- and Check PointCHKP-- are closing gaps in cloud and AI capabilities[2]. CrowdStrike's SASE expansion and $200 million acquisition of Adaptive Shield[2] aim to counter this, but execution risks remain.

Conclusion: A Calculated Bet on the Future

CrowdStrike's investor day guidance reflects a company balancing short-term pragmatism with long-term ambition. Its Falcon platform's modular architecture and AI-native roadmap position it to capitalize on the $300+ billion cybersecurity TAM[5], but scaling to $10 billion in ARR will require navigating slowing endpoint growth, competitive pressures, and reputational risks. For investors, the key question is whether CrowdStrike's R&D-driven innovation and sticky customer base can offset these headwinds—a bet that hinges on the company's ability to evolve from a product to a platform.

Comentarios

Aún no hay comentarios