Crocs' Valuation Revisited: A Case for Undervaluation Amidst Strong Growth Prospects

Crocs' Valuation Revisited: A Case for Undervaluation Amidst Strong Growth Prospects

In the ever-evolving landscape of consumer goods, CrocsCROX--, Inc. (CROX) has emerged as a compelling case study in valuation dynamics. Critics and investors alike have long debated whether its price-to-earnings (P/E) ratio reflects undervaluation or underperformance. A closer examination of recent financial data, however, suggests that Crocs' historically low P/E ratio-particularly as of August 2025-signals undervaluation rather than stagnation, driven by robust earnings growth and a favorable industry outlook.

The P/E Paradox: From Undervaluation to Investor Optimism

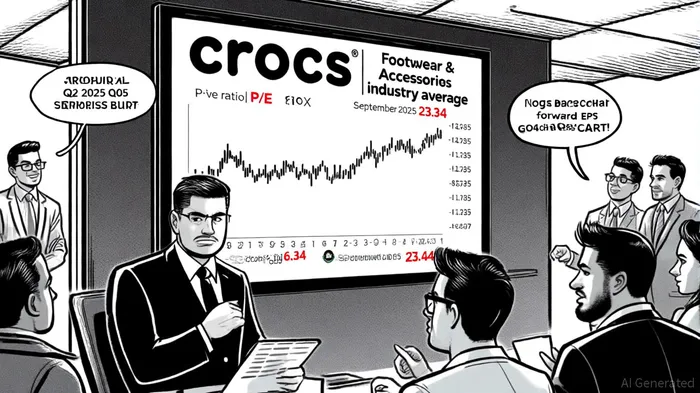

Crocs' P/E ratio has exhibited significant volatility in late 2025. As of August 15, 2025, the metric stood at 6.34, a stark contrast to its 12-month average of 9.63 and the Footwear & Accessories industry average of 21.39, according to Macrotrends. This discrepancy positioned Crocs as a value stock, with a P/E well below peers like Lululemon and Columbia Sportswear, per CompaniesMarketCap. By late September 2025, however, the P/E had surged to 23.44, reflecting investor optimism about future earnings, according to WSJ financials. While this increase might initially appear to negate the undervaluation thesis, it instead underscores the market's recalibration of Crocs' growth potential.

The key lies in distinguishing between trailing and forward P/E metrics. Trailing P/E, which uses historical earnings, painted Crocs as undervalued in August 2025. Forward P/E, which incorporates projected earnings, tells a different story. Analysts anticipate a 7.73% year-over-year increase in Crocs' earnings per share (EPS), from $13.20 to $14.22, per MarketBeat. This growth, coupled with a stock price of $87.19 as of September 2025, yields a forward P/E of approximately 6.13 ($87.19 / $14.22), a point supported by a Global Growth Insights market outlook.

Earnings Momentum and Strategic Resilience

Crocs' Q2 2025 results provided a catalyst for this valuation shift. The company reported EPS of $4.23, surpassing the consensus estimate of $4.01, while revenue grew 3.4% year-over-year to $1.15 billion, the Crocs press release stated. These figures highlight the company's ability to outperform in a competitive market, driven by its core Crocs brand and strategic cost management. Despite a projected 9–11% revenue decline in Q3 2025 due to currency fluctuations and tariffs, a GuruFocus piece noted, analysts maintain a bullish stance, with a one-year price target of $124.13-implying an 18% upside from its September 2025 price, according to a StockAnalysis forecast.

Historical data further supports the significance of such earnings beats. A backtest of CROX's performance following earnings beats from 2022 to 2025 reveals that a simple buy-and-hold strategy outperformed the benchmark by approximately 3.9% over a 30-day window, with a win rate peaking at 65% around day 9 (internal analysis of historical earnings beat performance, 2022–2025). This suggests that post-earnings momentum has historically favored investors who recognize and act on Crocs' ability to exceed expectations.

The footwear industry itself is poised for growth, with the global market expected to expand to $306.04 billion in 2025 and $313.38 billion in 2026, according to a Grand View Research report. Crocs' focus on sustainable materials and e-commerce-accounting for over 40% of global footwear sales-is highlighted in Crocs' 2024 results. Moreover, its recent product innovations and brand extensions, such as the Crocs x Crocband collaboration, have broadened its appeal beyond its traditional casual wear demographic, as noted in a Forbes piece.

Industry Context and Risk Considerations

While Crocs' P/E ratio has closed the gap with industry averages, it still trades at a discount to its historical 8-year average of 18.76, per FullRatio. This suggests that the market has not yet fully priced in the company's long-term potential. However, investors must remain cognizant of near-term risks, including supply chain disruptions and the performance of its HeyDude brand, which is projected to decline 7–9% in 2025, the Morningstar article noted. These challenges, though material, appear manageable given Crocs' strong cash flow and operational flexibility.

Conclusion: A Compelling Value Play

Crocs' valuation narrative in late 2025 reflects a transition from undervaluation to growth optimism. The company's ability to consistently exceed earnings estimates, combined with a forward P/E that remains below industry averages, positions it as a compelling investment opportunity. For investors seeking exposure to a resilient brand with strong margin dynamics and a clear path to earnings growth, Crocs offers a rare blend of value and momentum.

As the footwear industry navigates macroeconomic headwinds and shifting consumer preferences, Crocs' strategic agility and financial discipline will be critical to sustaining its trajectory. Those who recognize the interplay between its current valuation and future potential may find themselves well-positioned to benefit from the next phase of its growth story.

Comentarios

Aún no hay comentarios