Credit Risk in a Post-Tricolor Bust Era

The collapse of Tricolor Holdings in September 2025-dubbed the "Tricolor Bust"-has exposed systemic vulnerabilities in overleveraged corporates and regional banks, particularly within the subprime auto lending sector. This event, driven by fraudulent double-pledging of loan portfolios and a fragile economic backdrop, has sent shockwaves through structured credit markets and reignited fears of a broader financial crisis. For investors, the fallout underscores the risks of lax underwriting standards, opaque collateral practices, and the interconnectedness of regional banks with high-risk asset classes.

The Mechanics of the Tricolor Bust

Tricolor's business model hinged on packaging high-interest auto loans for low-income and undocumented borrowers into asset-backed securities (ABS), a strategy that became untenable as delinquency rates soared. According to a report by DealershipGuy, the company allegedly pledged identical loan portfolios as collateral for multiple warehouse credit lines with institutions like JPMorgan ChaseJPM--, BarclaysBCS--, and Fifth ThirdFITB-- Bancorp[1]. This double-pledging scheme, now under DOJ investigation, left creditors facing potential losses in the hundreds of millions[2].

The company's Chapter 7 bankruptcy-unusual for a multibillion-dollar entity-highlighted the fragility of its operations. A Bloomberg Law analysis noted that Tricolor's sudden liquidation bypassed Chapter 11 restructuring, leaving a trustee to manage a complex portfolio of 100,000 auto loans and securitized assets across six states[3]. The fallout has already triggered a revaluation of AAA-rated ABS tranches tied to Tricolor, with some trading at as low as 12 cents on the dollar, exposing the opacity of structured credit markets[4].

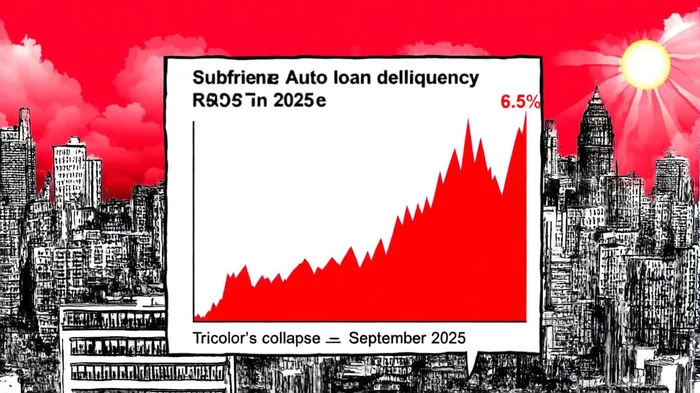

Systemic Risks for Regional Banks and Structured Credit

Regional banks, often the backbone of subprime lending, face disproportionate risks. Tricolor's collapse has forced institutions like Fifth Third and JPMorganJPM-- to reassess their exposure to subprime ABS, which now face heightened scrutiny. A SaferBankingResearch report warns that the banking system may be "starting to crack" as lenders with similar portfolios brace for write-downs[5].

The subprime auto loan market, valued at over $1.7 trillion, is particularly vulnerable. Fitch data cited by Axios reveals that subprime delinquency rates for 60+ day defaults hit 6.5% in Q2 2025-the highest since 1994[6]. This trend is exacerbated by rising interest rates, which have pushed average monthly payments for new vehicles to $745 and used vehicles to $521[7]. For borrowers with no credit scores or unstable incomes, these payments are unsustainable, leading to a cascade of defaults that ripple through the credit chain.

Regulatory and Economic Implications

Regulators are now scrutinizing underwriting standards in the subprime sector. The Texas Department of Motor Vehicles and the Texas Office of Consumer Credit Commissioner are investigating consumer complaints tied to Tricolor[8], while broader calls for tighter lending rules are growing. Such measures could reduce credit access for marginalized communities but may also stabilize the sector by curbing predatory practices.

Economically, the Tricolor Bust mirrors the 2008 mortgage crisis in its reliance on opaque collateral and overleveraged borrowers. A Vogon Today analysis draws parallels between the two events, noting that both were fueled by lax oversight and a reliance on securitization to mask risk[9]. With inflation, elevated rates, and a slowing labor market compounding pressures, the risk of further instability looms large.

Conclusion: Navigating the New Credit Landscape

For investors, the post-Tricolor Bust era demands caution. Overleveraged corporates and regional banks with exposure to subprime ABS or high-risk borrowers are prime candidates for stress. Diversification into prime loans or alternative credit instruments may offer safer havens. Meanwhile, policymakers must balance regulatory tightening with the need to preserve credit access for underserved populations.

The Tricolor Bust is not an isolated event but a symptom of deeper structural weaknesses. As delinquency rates climb and scrutiny intensifies, the lessons of 2008 remain starkly relevant.

Comentarios

Aún no hay comentarios