Credit Card Debt: The Silent Killer of Financial Stability

Generado por agente de IAHarrison Brooks

viernes, 21 de marzo de 2025, 11:08 pm ET2 min de lectura

NRDS--

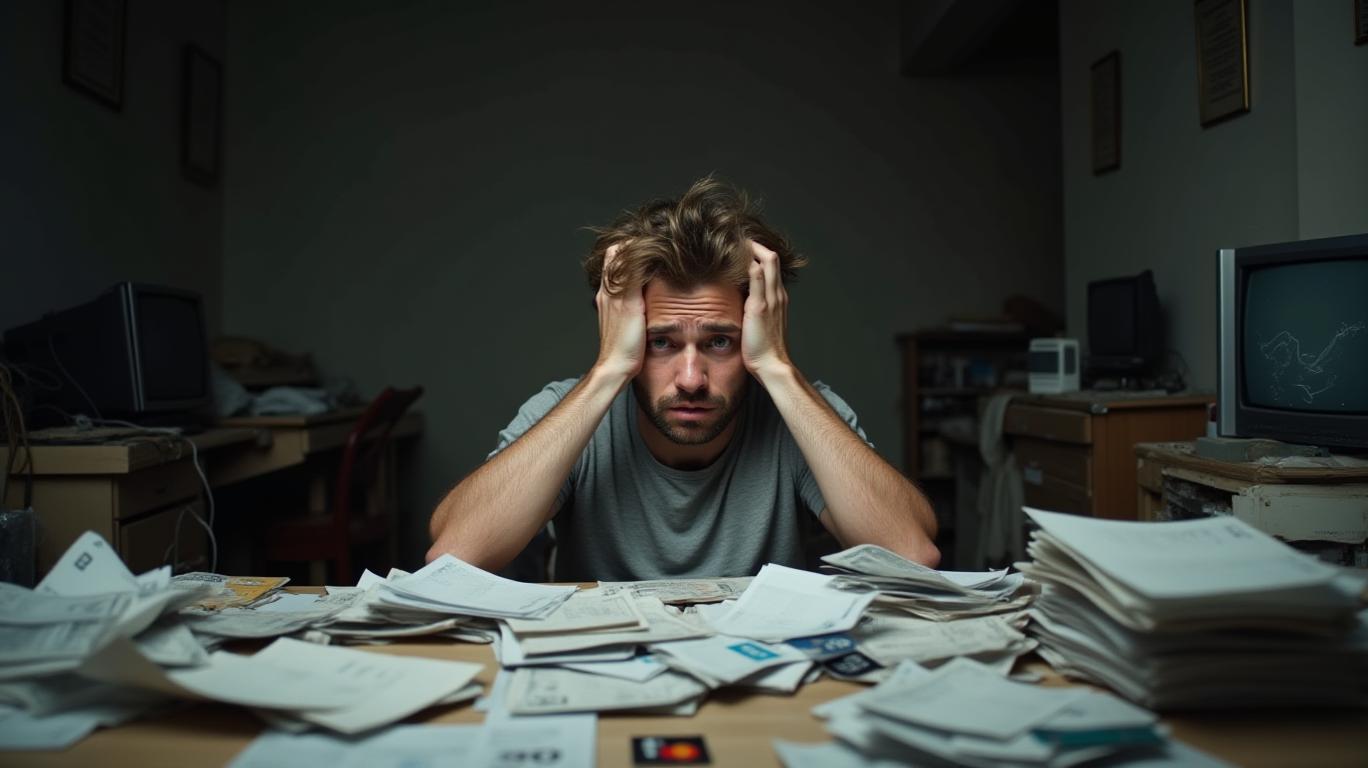

In the realm of personal finance, credit card debt is often seen as a necessary evil, a tool to bridge the gapGAP-- between income and expenses. However, as the Philadelphia Federal Reserve's recent data reveals, this tool has become a double-edged sword, with the share of active credit card accounts making just the minimum payment hitting a 12-year high of 10.75% from July through September 2024. This alarming trend signals a deeper issue: the silent killer of financial stability is lurking in the shadows, and it's time to shine a light on it.

The average American household with revolving credit card debt owes $10,563, according to a NerdWalletNRDS-- survey. This figure is not just a number; it represents the financial burden that millions of Americans carry daily. The consequences of this debt are far-reaching, affecting not only individual financial health but also the broader economic stability.

One of the most telling indicators of unsustainable credit card debt is the credit utilization rate. Experts recommend keeping this rate below 30%. However, with the average credit card balance reaching $6,380 and interest rates hovering around 20.27%, many consumers find themselves in a cycle of debt that seems impossible to break. For instance, if a consumer only makes the minimum payments, they could end up paying $9,344 in interest over 218 months (more than 18 years). This is a stark reminder that carrying a large balance month to month results in high interest charges, making it harder to repay what you owe.

The debt-to-income ratio is another critical indicator. The 28/36 rule suggests that consumers should spend no more than 28% of their gross monthly income on housing and a maximum of 36% on all debt payments. However, with the cost of living rising and median household income lagging behind, many consumers find themselves paying significantly more than this, indicating that their debt is too high and unsustainable.

The psychological burden of debt is another often-overlooked consequence. The stress associated with high debt levels can lead to conservative financial habits, focusing on repayment and saving. While this shift can reduce personal debt, it may also dampen consumer spending, further affecting economic activity. This is evident from the fact that lower and middle-income household saving rates turned negative in early 2022 as those consumers drew down rainy-day funds for the better part of two years. Savings are positive again but below pre-pandemic levels, indicating that what appears as stout spending today comes at the cost of more vulnerable finances for the working poor.

The increasing reliance on credit cards for everyday expenses has significant implications for consumer spending patterns and overall economic stability. As credit card balances swell, the share of delinquent balances is also worsening. This trend suggests that consumers are not only spending more but also paying off less, increasing revolving amounts and potentially leading to a cycle of debt that can be difficult to break.

To mitigate potential risks associated with high levels of consumer debt, investors can employ several strategies. One effective approach is to diversify their investment portfolios to include assets that are less sensitive to consumer spending, such as bonds or real estate. Additionally, investors can focus on sectors that are less reliant on consumer discretionary spending, such as healthcare or utilities, which tend to be more stable during economic downturns.

Another strategy is to invest in companies that have strong balance sheets and low levels of debt. These companies are better positioned to weather economic storms and continue to generate profits even during periods of reduced consumer spending. For instance, companies with high cash reserves and low debt-to-equity ratios are more likely to maintain their dividend payments and stock prices during economic downturns.

Investors can also consider investing in financial institutionsFISI-- that offer debt consolidation or credit counseling services. These institutions can help consumers manage their debt more effectively, reducing the risk of default and improving overall financial stability. For instance, ClearOneCLRO-- Advantage specializes in offering customized debt settlement programs aimed at helping individuals manage unsecured debt effectively.

In conclusion, the increasing reliance on credit cards for everyday expenses can lead to reduced consumer spending and economic instability. Investors can mitigate these risks by diversifying their portfolios, focusing on stable sectors, investing in companies with strong balance sheets, and supporting financial institutions that offer debt management services. It's time to recognize the silent killer of financial stability and take action to address it before it's too late.

In the realm of personal finance, credit card debt is often seen as a necessary evil, a tool to bridge the gapGAP-- between income and expenses. However, as the Philadelphia Federal Reserve's recent data reveals, this tool has become a double-edged sword, with the share of active credit card accounts making just the minimum payment hitting a 12-year high of 10.75% from July through September 2024. This alarming trend signals a deeper issue: the silent killer of financial stability is lurking in the shadows, and it's time to shine a light on it.

The average American household with revolving credit card debt owes $10,563, according to a NerdWalletNRDS-- survey. This figure is not just a number; it represents the financial burden that millions of Americans carry daily. The consequences of this debt are far-reaching, affecting not only individual financial health but also the broader economic stability.

One of the most telling indicators of unsustainable credit card debt is the credit utilization rate. Experts recommend keeping this rate below 30%. However, with the average credit card balance reaching $6,380 and interest rates hovering around 20.27%, many consumers find themselves in a cycle of debt that seems impossible to break. For instance, if a consumer only makes the minimum payments, they could end up paying $9,344 in interest over 218 months (more than 18 years). This is a stark reminder that carrying a large balance month to month results in high interest charges, making it harder to repay what you owe.

The debt-to-income ratio is another critical indicator. The 28/36 rule suggests that consumers should spend no more than 28% of their gross monthly income on housing and a maximum of 36% on all debt payments. However, with the cost of living rising and median household income lagging behind, many consumers find themselves paying significantly more than this, indicating that their debt is too high and unsustainable.

The psychological burden of debt is another often-overlooked consequence. The stress associated with high debt levels can lead to conservative financial habits, focusing on repayment and saving. While this shift can reduce personal debt, it may also dampen consumer spending, further affecting economic activity. This is evident from the fact that lower and middle-income household saving rates turned negative in early 2022 as those consumers drew down rainy-day funds for the better part of two years. Savings are positive again but below pre-pandemic levels, indicating that what appears as stout spending today comes at the cost of more vulnerable finances for the working poor.

The increasing reliance on credit cards for everyday expenses has significant implications for consumer spending patterns and overall economic stability. As credit card balances swell, the share of delinquent balances is also worsening. This trend suggests that consumers are not only spending more but also paying off less, increasing revolving amounts and potentially leading to a cycle of debt that can be difficult to break.

To mitigate potential risks associated with high levels of consumer debt, investors can employ several strategies. One effective approach is to diversify their investment portfolios to include assets that are less sensitive to consumer spending, such as bonds or real estate. Additionally, investors can focus on sectors that are less reliant on consumer discretionary spending, such as healthcare or utilities, which tend to be more stable during economic downturns.

Another strategy is to invest in companies that have strong balance sheets and low levels of debt. These companies are better positioned to weather economic storms and continue to generate profits even during periods of reduced consumer spending. For instance, companies with high cash reserves and low debt-to-equity ratios are more likely to maintain their dividend payments and stock prices during economic downturns.

Investors can also consider investing in financial institutionsFISI-- that offer debt consolidation or credit counseling services. These institutions can help consumers manage their debt more effectively, reducing the risk of default and improving overall financial stability. For instance, ClearOneCLRO-- Advantage specializes in offering customized debt settlement programs aimed at helping individuals manage unsecured debt effectively.

In conclusion, the increasing reliance on credit cards for everyday expenses can lead to reduced consumer spending and economic instability. Investors can mitigate these risks by diversifying their portfolios, focusing on stable sectors, investing in companies with strong balance sheets, and supporting financial institutions that offer debt management services. It's time to recognize the silent killer of financial stability and take action to address it before it's too late.

Divulgación editorial y transparencia de la IA: Ainvest News utiliza tecnología avanzada de Modelos de Lenguaje Largo (LLM) para sintetizar y analizar datos de mercado en tiempo real. Para garantizar los más altos estándares de integridad, cada artículo se somete a un riguroso proceso de verificación con participación humana.

Mientras la IA asiste en el procesamiento de datos y la redacción inicial, un miembro editorial profesional de Ainvest revisa, verifica y aprueba de forma independiente todo el contenido para garantizar su precisión y cumplimiento con los estándares editoriales de Ainvest Fintech Inc. Esta supervisión humana está diseñada para mitigar las alucinaciones de la IA y garantizar el contexto financiero.

Advertencia sobre inversiones: Este contenido se proporciona únicamente con fines informativos y no constituye asesoramiento profesional de inversión, legal o financiero. Los mercados conllevan riesgos inherentes. Se recomienda a los usuarios que realicen una investigación independiente o consulten a un asesor financiero certificado antes de tomar cualquier decisión. Ainvest Fintech Inc. se exime de toda responsabilidad por las acciones tomadas con base en esta información. ¿Encontró un error? Reportar un problema

Comentarios

Aún no hay comentarios