Coupang's RS 86 Surge: A Momentum Play in the Evolving E-Commerce Landscape

Coupang (CPNG) has recently captured the attention of momentum investors, with its Relative Strength (RS) Rating surging to 86—a significant jump from 79 in early 2025[1]. This metric, calculated by Investor's Business Daily (IBD), evaluates a stock's 52-week performance relative to the market, with scores above 80 historically signaling strong growth potential[2]. For CoupangCPNG--, this improvement reflects not only improved price action but also a broader re-rating of its value proposition in the post-pandemic e-commerce landscape.

Drivers of the RS 86 Surge

Coupang's ascent to RS 86 is underpinned by a combination of financial resilience and strategic innovation. In Q3 2024, the company reported a 23% year-over-year revenue increase, driven by a 146% surge in Coupang Eats and Coupang Pay revenue (excluding Farfetch's contribution)[3]. This diversification into adjacent services—such as food delivery and digital payments—has insulated the company from pure-play e-commerce volatility. Meanwhile, the acquisition of Farfetch has expanded Coupang's footprint in luxury fashion, a high-margin segment critical for long-term growth[4].

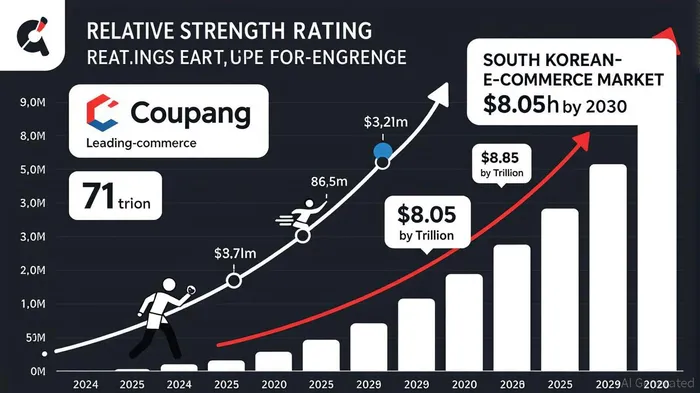

The RS improvement also aligns with Coupang's dominance in South Korea's hyper-competitive e-commerce market. With 22.5 million active customers in 2024—a 11% year-over-year increase—the company has solidified its position as the nation's top online retailer[5]. Its logistics network, including same-day delivery via Coupang Wow and a dense network of fulfillment centers, remains a key differentiator. Analysts note that these operational efficiencies have allowed Coupang to maintain profit margins while competitors like AmazonAMZN-- struggle to gain traction in the region[6].

Momentum Investing and Re-Rating Potential

The RS 86 rating places Coupang in the top 10% of IBD's universe, a threshold often associated with stocks poised for sustained outperformance. Historical data suggests that companies with RS ratings above 80 are more likely to lead market rallies, particularly in sectors with strong growth tailwinds[7]. For Coupang, this momentum is further amplified by the broader e-commerce boom in South Korea, where the market is projected to grow at a 20.04% CAGR through 2030[8].

However, the company faces headwinds. International rivals like Temu, owned by PDD HoldingsPDD--, are leveraging aggressive pricing and social media-driven marketing to target price-sensitive consumers. Coupang's response has been to double down on its logistics infrastructure and expand into high-margin categories. For instance, its Singapore and Taiwan logistics hubs are now generating cross-border revenue, while its bundled subscription services (e.g., Coupang Plus) aim to lock in customer loyalty.

Post-Pandemic Positioning and Earnings Outlook

Coupang's re-rating potential is also supported by its improving earnings profile. While 2024 saw flat EPS growth, analysts project a dramatic turnaround in 2025, with adjusted EPS expected to rise from $0.01 to $0.49—a 4,800% increase. This optimism is rooted in the company's ability to scale its super-app ecosystem and capitalize on the shift toward mobile commerce.

Yet, investors must weigh these positives against macroeconomic risks. Rising interest rates and global supply chain disruptions could pressure margins. Still, Coupang's strong balance sheet and recurring revenue streams from subscriptions and digital services provide a buffer.

Conclusion: A Momentum Play with Long-Term Legs

Coupang's RS 86 rating is more than a technical indicator—it reflects a company that has adapted to post-pandemic consumer behavior while maintaining its edge in a rapidly evolving sector. For momentum investors, the stock offers a compelling blend of short-term price strength and long-term re-rating potential. As the South Korean e-commerce market expands and Coupang continues to innovate, the company is well-positioned to sustain its leadership—and its RS rating—well into 2026.

Comentarios

Aún no hay comentarios