Corporate Fairness in Mergers: Evaluating First Savings Financial Group's Deal for Shareholder Value

The recent proposed merger between First Merchants CorporationFRME-- (FRME) and First Savings Financial GroupFSFG--, Inc. (FSFG) has sparked debate about whether public shareholders of the latter are receiving fair value. This analysis evaluates the deal's fairness by examining valuation metrics, corporate governance practices, and post-merger synergies.

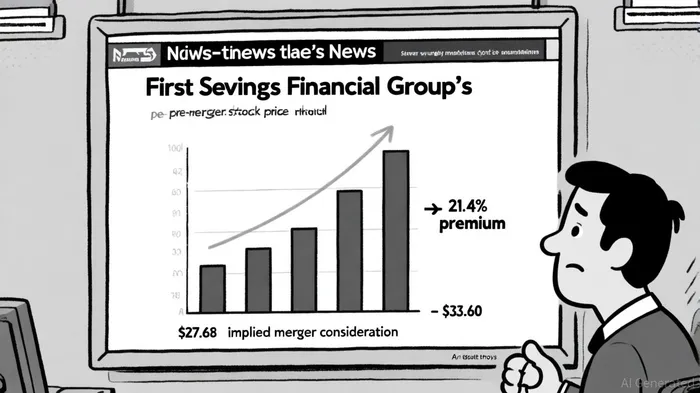

Premium and Valuation Metrics: A Mixed Signal

First Savings shareholders will receive 0.85 shares of FRMEFRME-- for each share of FSFGFSFG--, implying a merger consideration of $33.60 per share based on FRME's closing price of $39.53 on September 24, 2025 [1]. This represents a 21.4% premium over FSFG's pre-merger stock price of $27.68 [2], a significant uplift that suggests the deal offers immediate value. However, the fairness of this premium must be contextualized against FSFG's financial performance and valuation ratios.

As of June 30, 2025, FSFG reported $2.4 billion in total assets, $1.9 billion in loans, and $1.7 billion in deposits, alongside a robust 13.7% return on average equity for the quarter [1]. Its trailing price-to-earnings (PE) ratio stands at 10.54, while its forward PE is 9.65 [3], indicating the stock was trading at a discount relative to earnings before the merger announcement. The $33.60 consideration, therefore, appears to reflect a re-rating of FSFG's intrinsic value, particularly given its recent 51% year-over-year net income growth and a 2.99% net interest margin [1].

Governance Concerns: No-Shop Clause and Shareholder Rights

Despite the premium, the merger agreement includes a restrictive no-shop clause that prohibits FSFG from soliciting competing bids, with penalties for noncompliance [1]. This raises questions about whether the board acted in shareholders' best interests by potentially limiting opportunities for a higher offer. The Ademi Firm has already initiated an investigation into this matter, scrutinizing whether the merger terms adequately protect public shareholders [1].

Furthermore, while the merger requires FSFG shareholder approval, no such vote has been held as of Q3 2025 [1]. This delay, coupled with the absence of a formal bidding process, could be perceived as a lack of transparency. Shareholders may reasonably ask whether the 0.85 exchange ratio fully captures FSFG's strategic value, particularly given the combined entity's projected $21 billion in assets and 11% earnings-per-share accretion by 2027 [1].

Post-Merger Synergies: Long-Term Value or Short-Term Compromise?

Proponents of the deal highlight long-term benefits, including cost synergies and expanded market reach. The combined entity, operating as First MerchantsFRME-- Bank, will control 127 branches across Indiana, Michigan, and Ohio, creating operational efficiencies expected to yield a 3.0-year tangible book value earnback period [1]. For FSFG's retail shareholders, this could translate into enhanced stability and access to a larger capital base.

However, these benefits are contingent on successful integration, which carries risks such as cultural clashes and integration costs. The merger's anticipated closure in Q1 2026 [1] leaves little room for error, and any delays could erode confidence in the deal's value proposition.

Conclusion: A Fair but Imperfect Deal

The merger offers a compelling premium and aligns with FSFG's strong financial performance, suggesting fair value for shareholders. Yet the restrictive no-shop clause and lack of competitive bidding introduce governance risks that could undermine long-term fairness. While the 21.4% premium and projected synergies justify the transaction on paper, shareholders should remain vigilant about the board's fiduciary duties and the integration process.

In the end, the deal appears to strike a balance between immediate value and strategic growth—but not without caveats. As the Ademi Firm's investigation unfolds, all eyes will be on whether FSFG's board can defend its decision as both prudent and equitable.

Comentarios

Aún no hay comentarios