Core Natural Resources: Strategic Upgrades and Undervalued Growth in the Energy Transition

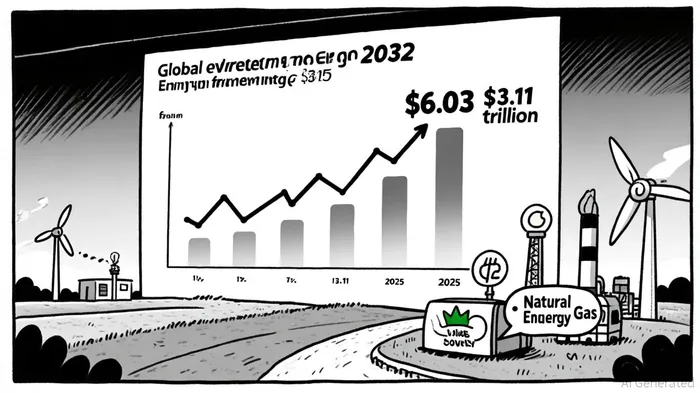

The energy transition is no longer a distant vision-it is a $3.11 trillion reality in 2025, growing at a 9.9% CAGR toward $6.03 trillion by 2032, according to Grand View Research. In this rapidly evolving landscape, Core NaturalCNR-- Resources (CNR) stands at a unique inflection point. While the company reported a $36.6 million net loss in Q2 2025, its $144.3 million adjusted EBITDA and $1.1 billion in revenue demonstrate resilience amid sector-wide volatility, as detailed in CNR's Q2 results. This article argues that CNR's strategic upgrades, undervalued assets, and alignment with transitional energy needs position it as a compelling long-term investment.

Strategic Upgrades: Synergies and Infrastructure

Core's recent announcement to increase annual synergy generation to $150–170 million underscores its commitment to operational efficiency, a point highlighted in CNR's Q2 results. This aligns with broader industry trends: 74% of investors are allocating $100 million+ to energy transition projects, with 64% prioritizing infrastructure upgrades, according to the KPMG outlook. CNR's focus on midstream infrastructure-such as LNG export facilities and AI-powered grid solutions-directly addresses the $2.2 trillion clean technology investment surge in 2025, per IMAcorp Q3 2025. For example, U.S. natural gas demand is projected to reach 151.4 trillion cubic feet by 2025, driven by grid reliability needs and AI-driven data centers, according to a PwC analysis. Core's strategic acquisitions of natural gas-fired power plants and battery storage systems further solidify its role in this transition.

Despite the Q2 2025 earnings report, historical data reveals limited predictive value for short-term trading around CNR's earnings releases. A backtest of CNR's performance from 2022 to 2025 shows that average excess returns versus the benchmark are small and statistically insignificant across a 30-day post-event window. For instance, the one-day post-earnings drift is mildly negative (-2.69%), and cumulative excess performance remains negative even by day 10. With only three earnings events in the sample, these results suggest no repeatable trading edge around CNR's earnings dates. This underscores the importance of focusing on long-term fundamentals rather than short-term volatility when evaluating CNR's strategic value.

Natural Gas: The Overlooked Bridge Fuel

While renewables dominate headlines, natural gas remains a critical transitional asset. According to a KPMG survey, 75% of investors continue to engage in fossil fuel projects, particularly natural gas, to ensure energy security. Core's $87.1 million in shareholder returns during Q2 2025, coupled with its exposure to LNG export capacity, highlights its ability to capitalize on this demand, as reported in CNR's Q2 results. With global crude oil production hitting 13.5 million barrels per day in 2025 and LNG supporting 37–74% of future electricity generation (per PwC), Core's diversified portfolio is uniquely positioned to benefit from both transitional and long-term energy needs.

Undervalued Potential: Balancing Risks and Rewards

Despite its strengths, Core faces headwinds, including regulatory uncertainty and intermittency challenges in renewables, as noted by Grand View Research. However, 94% of investors are forming partnerships to mitigate such risks, a strategy highlighted in the KPMG outlook, which Core has embraced through collaborations on grid modernization and decarbonization projects. At a time when 72% of investors report accelerating energy transition investments (IMAcorp Q3 2025), Core's $0.70 per share loss in Q2 2025 appears to be a short-term blip rather than a structural issue. Its $1.1 billion revenue and $144.3 million adjusted EBITDA suggest a company with strong cash flow generation, even as it navigates the transition.

Conclusion: A Strategic Bet on the Transition

Core Natural Resources is not a pure-play renewable energy stock, nor is it a traditional fossil fuel company. Instead, it embodies the hybrid model that the energy transition demands. By leveraging its natural gas infrastructure, pursuing strategic synergies, and aligning with $3.3 trillion in global energy investments noted by PwC, Core is well-positioned to thrive in a world where energy security and decarbonization coexist. For investors seeking undervalued growth in the energy transition, CNRCNR-- offers a compelling case: a company upgrading its assets, navigating regulatory and geopolitical risks, and capitalizing on the $1.1 trillion fossil fuel investment still required in 2025, as discussed in IMAcorp Q3 2025.

Comentarios

Aún no hay comentarios