COPT Defense Properties: Strategic Resilience in a Volatile Political Climate

COPT Defense Properties: Strategic Resilience in a Volatile Political Climate

In an era of heightened political polarization and fiscal uncertainty, COPT DefenseCDP-- Properties (CDP) stands out as a rare example of a real estate investment trust (REIT) that has engineered its business model to thrive amid government instability. As the U.S. faces recurring threats of shutdowns-most recently in October 2025-investors are scrutinizing how companies in the defense and government services sectors can navigate such disruptions. For CDP, a REIT focused on mission-critical facilities near defense installations, the risks are not just mitigated but transformed into strategic advantages.

A Niche Built for Resilience

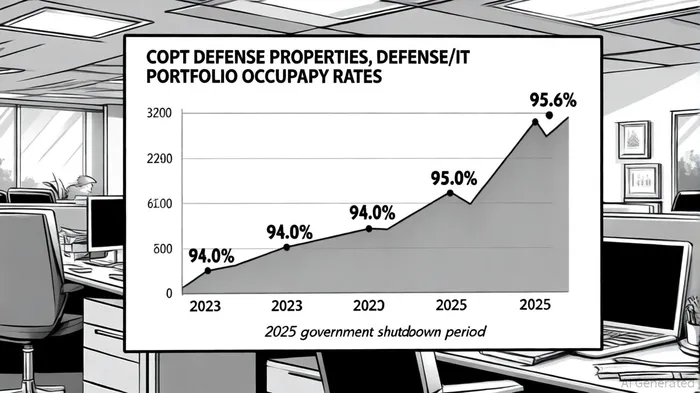

COPT Defense Properties has carved out a unique position in the real estate market by specializing in high-security properties near U.S. defense hubs, including the Pentagon and Fort Meade. As of June 30, 2025, its Defense/IT portfolio was 95.6% occupied and 96.8% leased, with tenants including government agencies and defense contractors locked into long-term leases averaging eight years, according to COPT's Q2 2025 results. This stability is further reinforced by contractual cash rent increases and a development pipeline where 89% of projects are pre-leased, reducing exposure to market volatility, per Fitch's affirmation.

The company's 2025 guidance underscores this resilience: it anticipates diluted earnings per share (EPS) of $1.27–$1.35 and funds from operations (FFO) per share of $2.62–$2.70, driven by lease commencements and development completions, according to COPT's 2025 guidance. Even as interest rates remain elevated, COPT's focus on cash-flow-generating assets-97% of its debt is fixed-rate-positions it to outperform peers in a high-interest environment, as noted in its Q2 results.

Mitigating Shutdown Risks Through Structure

Government shutdowns typically disrupt federal operations, but COPT's business model is designed to insulate it from such shocks. Its tenants, which include defense contractors and agencies with statutorily funded obligations, are less likely to face immediate furloughs or operational halts. For instance, during the October 2025 shutdown, defense manufacturers under COPT's portfolio saw minimal declines (average -0.01%), while government services contractors even posted gains (+2.28%), according to a 2025 shutdown analysis.

This resilience is further bolstered by COPT's proactive risk management. The company has accelerated the disposition of non-core regional offices to concentrate its portfolio on high-growth defense/IT assets, as noted by Fitch. Additionally, its tenant retention rates-90% in Q2 2025 and 82% year-to-date-highlight the stickiness of its client base, per COPT's Q2 2025 results. Fitch Ratings has affirmed COPT's investment-grade status, citing its "superior tenant credit quality and long-term lease structures" as key differentiators (Fitch).

Historical Precedent and Sector Dynamics

While COPT's specific historical performance during past shutdowns is not fully documented, broader trends in defense REITs suggest a pattern of resilience. A 2025 EPU study on Economic Policy Uncertainty (EPU) and sector-specific REITs found that industrial and infrastructure-focused REITs act as "net receivers of shocks," meaning they absorb market stress better than others. Defense REITs, with their alignment to national security priorities, fit this profile. For example, during the 2013 and 2019 shutdowns, defense manufacturers saw average declines of just -0.01%, compared to broader market losses, as highlighted in the 2025 shutdown analysis.

COPT's strategic expansion into new defense markets-such as Colorado Springs and San Antonio-also diversifies its geographic risk. While 65% of its net operating income (NOI) currently comes from the Baltimore-Washington corridor, the company aims to reduce this concentration through a $300 million acquisition pipeline by Q4 2025, according to its 2025 guidance. This proactive diversification, combined with a net debt-to-EBITDA ratio of 5.9x, signals a disciplined approach to growth, per COPT's Q2 2025 results.

Strategic Opportunities in a High-Defense Era

The U.S. defense budget, now exceeding $800 billion, creates a tailwind for COPT's mission-critical facilities. With 600,000 square feet of new developments slated for 2025-75% pre-leased-the company is capitalizing on modernization needs for cyber defense, intelligence, and missile systems, as detailed in its Q2 results. Analysts at Citi note that COPT's "pure-play defense/IT landlord" strategy positions it to benefit from long-term secular trends, including increased federal spending on secure infrastructure, a point echoed by Fitch.

However, challenges remain. COPT's small market cap ($1.2B) and geographic concentration require careful monitoring. Yet, its focus on self-funding developments and maintaining a strong balance sheet-97% fixed-rate debt-mitigates liquidity risks, as reported in the Q2 results.

Conclusion: A Hedge Against Uncertainty

COPT Defense Properties exemplifies how strategic specialization can turn systemic risks into competitive advantages. By anchoring its portfolio to long-term defense contracts, prioritizing tenant stability, and expanding into new markets, the company has insulated itself from the volatility that plagues broader REIT sectors. For investors seeking exposure to a sector that thrives amid political uncertainty, COPTCDP-- offers a compelling case: a business model built not just to survive shutdowns, but to outperform in them.

Comentarios

Aún no hay comentarios