Confluent's Q3 2025 Earnings: A Tipping Point for Cloud-Native Data Infrastructure?

Unit Economics: Margin Expansion and Cost Discipline

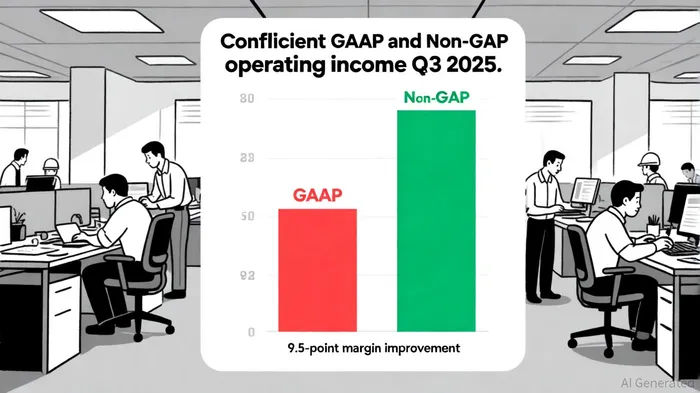

Confluent's Q3 2025 results revealed a marked improvement in operating margins, with non-GAAP operating income surging to $29.1 million, a $13.3 million increase year-over-year, according to Confluent's press release. This reflects a 9.5-point improvement in operating margin to -27.9% from -37.4% in Q3 2024, as shown in Confluent's investor slides. The company's free cash flow margin also rose to 8.2%, up from 3.9% in the prior quarter, per the investor slides, signaling tighter cost controls.

However, GAAP operating losses persist, narrowing to $83.3 million from $93.7 million in the same period last year, as noted in the press release. This discrepancy is largely attributable to non-cash expenses such as stock-based compensation, which totaled $106.8 million for the quarter (see the investor slides). While these charges are typical for high-growth tech firms, they highlight the challenges of forecasting GAAP profitability in a sector reliant on equity-based incentives.

Growth Sustainability: Cloud-First Strategy and Revenue Diversification

Confluent's cloud-first strategy is paying dividends, with ConfluentCFLT-- Cloud revenue reaching $161 million-a 24% year-over-year increase and 54% of total revenue, per the press release. This segment's growth outpaced the broader market, driven by enterprise demand for real-time data streaming solutions. The company also reported 1,487 customers with $100,000 or more in annual recurring revenue (ARR), a 10% year-over-year increase, according to the press release.

Yet, the path to sustained growth is not without hurdles. While total revenue grew 19% to $298.5 million (see the press release), the company's guidance for Q4 2025-$295.5–296.5 million in subscription revenue-suggests a moderation in growth momentum. This cautious outlook, coupled with a 3% shortfall in Q4 revenue expectations relative to analyst forecasts in an IndexBox analysis, raises concerns about macroeconomic headwinds and customer acquisition costs.

Enterprise Adoption: Stabilized Retention, Uncertain Churn

A critical metric for SaaS companies is the dollar-based net retention rate (DBNRR), which Confluent described as "stabilized" in Q3 2025, according to the press release. While the company did not disclose a specific percentage, the 24% year-over-year growth in Confluent Cloud revenue and 43% acceleration in remaining performance obligations suggest robust consumption growth (see the press release).

Enterprise churn, however, remains opaque. Confluent reported 1,487 enterprise customers with $100k+ ARR, up 48 from the previous quarter in a FinancialContent article, but the modest increase implies a slowdown in new customer acquisition. Without explicit churn data, investors are left to infer retention health from indirect indicators such as upsell success and geographic diversification. The company noted 58% of Q3 revenue came from international markets (per the investor slides), a positive sign for long-term scalability but one that also introduces currency and regulatory risks.

The Tipping Point: Balancing Optimism and Caution

Confluent's Q3 results present a mixed picture. On one hand, the company's cloud transition and margin expansion demonstrate operational maturity. On the other, the lack of transparency around churn and the cautious Q4 guidance hint at underlying fragility. For cloud-native data infrastructure to become a true tipping point, Confluent must prove it can sustain high-growth metrics while scaling enterprise adoption without sacrificing profitability.

The coming quarters will be pivotal. If the company can stabilize its DBNRR, reduce GAAP losses, and maintain cloud revenue growth above 20%, it may solidify its position as a leader in the data streaming space. Until then, investors should remain vigilant, balancing the promise of innovation with the realities of a competitive and capital-intensive market.

Comentarios

Aún no hay comentarios