Concentrix's Earnings Miss: A Warning Sign or a Strategic Pivot in the AI-Driven BPO Landscape?

Concentrix Corporation (NASDAQ: CNXC) recently reported its Q2 2025 earnings, delivering a mixed performance that has sparked debate among investors. While revenue grew by 1.5% year-on-year to $2.417 billion, surpassing estimates[1], the company's earnings per share (EPS) fell short of expectations, and operating margins contracted. This raises critical questions: Is this a temporary setback tied to strategic investments, or does it signal a broader stall in Concentrix's long-term growth story?

The Earnings Miss and Margin Compression

Concentrix's Q2 results revealed a 1.3% decline in operating income to $148.3 million and a 5.4% drop in non-GAAP operating income to $303.7 million[1]. The CEO attributed these declines to mid-quarter program pauses and increased investments in AI-driven initiatives, which are expected to yield returns by year-end[1]. However, the EPS miss—falling $0.06 below the $2.76 consensus—highlighted immediate profitability challenges[1].

Historical context from past earnings misses offers caution. Between 2022 and now, CNXCCNXC-- experienced seven earnings misses, with an average cumulative return of –6.6% over 30 trading days post-event, outperforming the benchmark (NASDAQ) by –3.3% but lacking statistical significance[1]. Short-term reactions were mixed, but negative drift emerged after the first week, with win rates declining sharply beyond day 7[1]. This suggests that while earnings misses may not immediately trigger panic, they often foreshadow prolonged underperformance.

Margin compression is not unique to ConcentrixCNXC--. The broader BPO industry is grappling with the dual forces of AI adoption and cost pressures. According to a 2025 industry report, AI integration has reduced operational costs by 25-40% but required upfront investments that temporarily squeeze margins[2]. For example, chatbots now handle 70-80% of routine customer interactions, cutting staffing needs but increasing R&D and technology expenditures[3]. This suggests that Concentrix's margin pressures may be industry-wide, though its execution of AI investments will determine its ability to outperform peers.

Strategic Investments and AI-Driven Growth

Concentrix's CEO, Chris Caldwell, emphasized the company's “momentum from AI investments,” including its iX Product Suite, which aims to deliver hyper-personalized customer experiences[1]. The company has also prioritized AI-powered data annotation and cybersecurity services, positioning itself in higher-margin segments of the BPO market[4]. These moves align with industry trends: specialized BPO services now achieve EBITDA margins of 30-45%, compared to 15-20% for basic customer service operations[2].

However, the path to margin expansion is not without risks. The BPO sector's average debt-to-equity ratio in Q2 2025 was 1.44[5], while Concentrix's ratio stood at 1.14[1]. Though lower leverage is generally favorable, the company's interest coverage ratio—maintained at 3.00 to 1.00—suggests it can service debt without immediate distress[1]. The key question is whether its AI investments will generate sufficient returns to justify the current margin compression.

Industry-Wide Pressures vs. Company-Specific Challenges

To assess whether Concentrix's struggles are isolated, consider its peers. Accenture, for instance, reported Q3 2025 revenues of $17.7 billion with an operating margin of 16.8%[6], demonstrating that large-scale BPO firms can maintain profitability through cost discipline. Meanwhile, smaller competitors like Teleperformance face margin erosion due to labor arbitrage models becoming obsolete[4].

Concentrix's revised full-year guidance—raising revenue projections to $9.72B-$9.815B—reflects confidence in its AI-driven strategy[1]. Yet, the company's adjusted free cash flow guidance of $625M-$650M for 2025 remains unchanged despite increased capital expenditures[1]. This implies that management expects AI investments to eventually offset margin pressures, but the timeline for this remains uncertain.

Is This a Buying Opportunity?

For investors, the critical variables are execution risk and market positioning. Concentrix's focus on AI-powered, high-value services aligns with long-term industry trends[2], and its debt profile is healthier than the sector average[5]. However, the company's ability to convert AI investments into tangible revenue growth will determine its success.

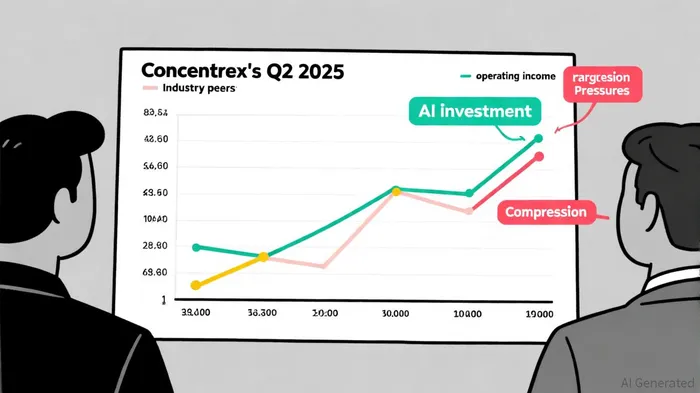

A visual comparison of Concentrix's Q2 performance against peers reveals a nuanced picture. While its revenue growth lagged behind Accenture's 8% YoY increase[6], its non-GAAP operating income of $303.7 million was competitive with firms like Teleperformance[4]. This suggests that Concentrix's challenges are more strategic than existential.

Conclusion

Concentrix's earnings miss and margin compression are symptomatic of the broader BPO industry's transition to AI-driven models. While the company's strategic investments in high-margin services are promising, the near-term risks of execution delays and capital intensity cannot be ignored. For now, the revised guidance and shareholder return commitments (e.g., $240M in buybacks[1]) suggest management remains confident in its long-term vision. Investors should monitor Q3 results for signs of margin stabilization and AI-driven revenue acceleration before making a final call.

Comentarios

Aún no hay comentarios