U.S.-Colombia Diplomatic Tensions and Market Implications

The escalating diplomatic tensions between the United States and Colombia in 2025 have underscored the fragility of economic partnerships in emerging markets, particularly when political instability intersects with trade and investment dynamics. President Gustavo Petro's allegations of U.S. involvement in a coup plot—based on leaked audio recordings involving former Colombian officials—triggered a cascade of retaliatory measures, including the recall of ambassadors, U.S. tariffs on Colombian imports, and threats of sanctions[1]. These developments have not only strained bilateral relations but also exposed Colombia's vulnerability to external shocks, raising critical questions about the investment risks tied to political instability in emerging economies.

The Economic Fallout: Tariffs, Trade, and FDI

Colombia's economy, heavily reliant on U.S. trade, has borne the brunt of the diplomatic crisis. In January 2025, the Trump administration imposed a 25% tariff on Colombian imports after Petro refused to allow U.S. deportation flights to land, citing inhumane treatment of repatriated citizens[3]. This move, coupled with a 12-hour suspension of consular services and a 25% emergency tariff, sent shockwaves through key export sectors. Coffee, which accounts for 20% of U.S. imports in the category, and cut flowers—nearly 60% of which are sold to South Florida—faced immediate price pressures and supply chain disruptions[4].

Foreign direct investment (FDI) has also contracted. By the end of 2024, FDI inflows had shrunk by 18.32% compared to 2023, with U.S. investments alone declining by 15% in the first half of 2025[5]. Petro's “Total Peace” policy, which prioritizes dialogue with armed groups over counter-narcotics enforcement, has further eroded investor confidence. Coca cultivation in Colombia surged to record levels in 2023, prompting U.S. lawmakers like Marco Rubio to accuse Petro of enabling drug trafficking and advocate for visa restrictions on Colombian officials[5].

Political Instability and Emerging Market Vulnerabilities

Colombia's case mirrors broader trends in emerging markets, where political instability often deters FDI and exacerbates currency volatility. Studies show that unpredictable governance, regulatory ambiguity, and security risks create an environment where foreign investors demand higher returns to offset perceived risks[6]. For instance, Brazil's FDI inflows fluctuated between $62.44 billion and $74.61 billion from 2022 to 2025 amid political crises and economic reforms[7]. Similarly, Nigeria and India have seen FDI volatility linked to corruption scandals and ethnic tensions[2].

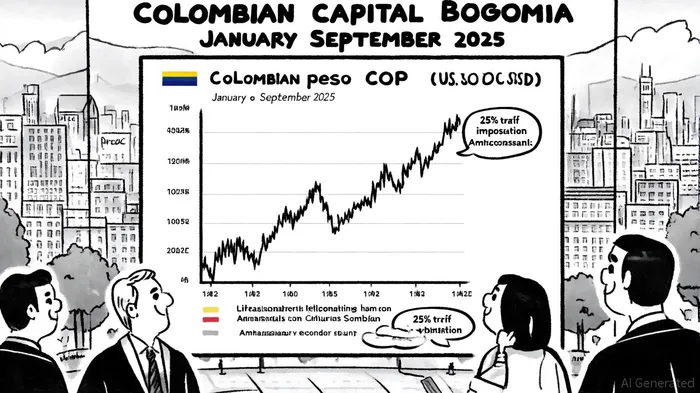

The U.S. monetary policy spillovers further compound these risks. Tightening cycles, such as those in 2022–2023, have historically triggered capital outflows from emerging markets, amplifying currency depreciation pressures[8]. Colombia's peso, for example, depreciated to 4,458.58 COP per USD in April 2025—the highest rate of the year—before partially recovering as diplomatic tensions eased[9]. Such volatility complicates hedging strategies for foreign investors and erodes returns.

Credit Ratings and Fiscal Risks

Fitch Ratings' recent downgrade of Colombia's credit outlook to “negative” highlights the fiscal risks stemming from the crisis. The central government's 2024 fiscal deficit reached 6.7% of GDP, with public debt climbing to 58% of GDP—projected to hit 62% by 2026[10]. These figures, coupled with Petro's renegotiation of trade agreements and restrictions on international arbitration, have raised concerns about long-term fiscal sustainability. Moody's has similarly warned that geopolitical tensions and U.S. trade policies could exacerbate Colombia's financial vulnerabilities[11].

Investor Implications and Strategic Considerations

For investors, the U.S.-Colombia crisis underscores the need for diversified portfolios and hedging mechanisms. Currency-hedged ETFs and forward contracts can mitigate exposure to peso volatility, while sector-specific analysis is critical. Colombia's energy transition and tech sectors remain attractive, but regulatory clarity and security improvements are prerequisites for sustained FDI inflows[5].

Historical precedents, such as Thailand's ability to attract FDI despite democratic deficits, suggest that strategic infrastructure and economic pragmatism can offset political risks[6]. However, Colombia's reliance on U.S. trade and its current fiscal trajectory present unique challenges.

Conclusion

The U.S.-Colombia diplomatic tensions of 2025 serve as a cautionary tale for emerging markets navigating political instability. While Colombia's strategic location and growing tech ecosystem offer long-term potential, the immediate risks—tariff-driven trade disruptions, FDI contractions, and credit downgrades—demand careful risk management. Investors must weigh short-term volatility against structural reforms and diversification efforts, recognizing that political stability remains a cornerstone of sustainable economic growth in emerging markets.

Comentarios

Aún no hay comentarios