Colombia's $500M Bond Issuance: Strategic Implications for Emerging Market Debt

The recent $500 million bond issuance by Colombia has sparked renewed interest in emerging market (EM) debt, offering a case study in balancing credit risk, liquidity demand, and yield appeal. As global investors navigate a shifting macroeconomic landscape—marked by moderating inflation and easing monetary policy—Colombia’s foray into the international bond market underscores both the opportunities and challenges inherent in EM sovereign debt.

Credit Quality: A Fragile Foundation

Colombia’s credit profile remains a mixed bag. While Fitch maintains a stable outlook with a "BB+" rating, Standard & Poor’s and Moody’sMCO-- have adopted negative outlooks, reflecting concerns over deteriorating fiscal accounts and a suspended fiscal rule. S&P’s downgrade to "BB" in June 2025 cited "weaker fiscal performance," with general government debt projected to rise to 63% of GDP by 2026 [3]. Moody’s "Baa2" rating similarly emphasizes the risks of failing to stabilize fiscal conditions, noting that Colombia’s debt burden is "elevated but manageable under current growth assumptions" [1].

The suspension of Colombia’s fiscal rule—a framework designed to align spending with revenue cycles—has exacerbated uncertainties. This policy gap, coupled with President Gustavo Petro’s expansion of fiscal spending, has led to a 70% decline in corporate bond sales through early July 2025, signaling investor caution [1]. For the $500 million bond, which carries a coupon rate of 6.18% and matures in 2032, the negative outlooks imply a heightened risk of further downgrades, potentially increasing borrowing costs in future issuances.

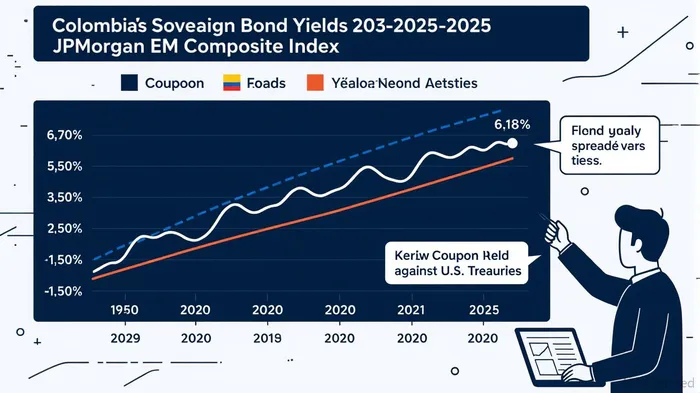

Liquidity and Yield Appeal: Navigating EM Trends

Despite these risks, Colombia’s bond issuance aligns with broader EM debt trends that favor large-denomination offerings. Bonds of $500 million or more have become increasingly common since the 2008 financial crisis, capturing 62% of new EM corporate debt post-2008 [1]. This trend is driven by the "size yield discount," where larger bonds—often included in benchmarks like the JPMorgan CEMBI Narrow Diversified Index—attract institutional investors seeking liquidity and diversification.

The 2025 Colombia bond, with its $500 million threshold, benefits from this dynamic. While specific subscription multiples for the issuance remain undisclosed, historical data offers context. Colombia’s inaugural green bond in 2021, for instance, was oversubscribed 4.6 times, securing a 7 basis point "greenium" [2]. Although the 2025 bond is not explicitly labeled as green, its 6.18% coupon—compared to the 8.5% and 7.375% rates on Colombia’s April 2025 sovereign bonds—suggests a strategic effort to balance cost and market appeal [3].

Yield comparisons further highlight its positioning. As of August 2025, the yield differential between EM dollar-denominated debt and U.S. Treasuries has narrowed to its smallest level in years, reflecting improved risk appetite [1]. Colombia’s 6.18% coupon, while higher than the 4.5% on its 2029 bonds, remains competitive against peers like Brazil’s 7.25% 2032 bonds and Mexico’s 6.8% 2030s [3]. This positions the issuance as a middle-tier option for investors seeking yield without excessive duration risk.

Strategic Implications: A Calculated Move

Colombia’s bond issuance reflects a dual strategy: managing liquidity needs while signaling fiscal discipline. Proceeds will partially fund the Sucuriu Project—a hydropower initiative—and repay existing debt, addressing both infrastructure gaps and refinancing pressures [2]. However, the negative credit outlooks cast doubt on the sustainability of this approach. If fiscal stabilization measures falter, the country could face a "downgrade spiral," where higher borrowing costs exacerbate debt dynamics [3].

For investors, the bond presents a nuanced proposition. The 6.18% yield offers a premium over U.S. Treasuries but comes with elevated credit risk compared to investment-grade EM peers like Indonesia or South Africa. Liquidity demand, meanwhile, hinges on the bond’s inclusion in key indices and Colombia’s ability to maintain investor confidence amid political and fiscal uncertainties.

Conclusion: A High-Yield Gamble?

Colombia’s $500 million bond issuance encapsulates the duality of EM debt in 2025: attractive yields amid fragile credit fundamentals. While the offering leverages favorable market conditions and liquidity incentives, its long-term success depends on Colombia’s fiscal trajectory. For risk-tolerant investors, the bond offers a compelling entry point—but one that demands close monitoring of policy developments and rating agency actions.

**Source:[1] Emerging markets debt investment views – August 2025 [https://www.schroders.com/en-be/be/professional/insights/emerging-markets-debt-investment-views---august-2025/][2] Bonds and Loans: Colombia issues inaugural green bond while UK gears up... [https://www.responsible-investor.com/bonds-and-loans-colombia-issues-inaugural-green-bond-while-uk-gears-up-for-second-green-gilt/][3] S&P, Moody's cut Colombia's debt rating over declining ..., [https://www.reuters.com/world/americas/sp-cuts-colombias-debt-rating-bb-over-declining-fiscal-results-2025-06-27/]

Comentarios

Aún no hay comentarios