Cloud Computing and AI Drive IT Services Surge: Where to Invest Next?

The global IT and business services market hit a record $29.2 billion in Q2 2025, fueled by an AI-driven cloud boom and strategic mega-deals reshaping the industry. With cloud infrastructure spending surging 34% year-over-year and managed services carving out new opportunities in energy and manufacturing, investors should focus on firms positioned to capitalize on this structural shift.

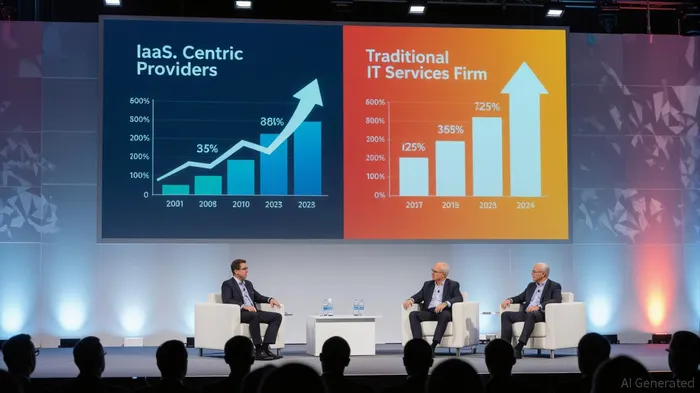

The Cloud Ascendancy: AI as the Catalyst

The report underscores a clear bifurcation in IT spending: enterprises are prioritizing cloud scalability for AI while scaling back discretionary projects. Cloud-based XaaS (everything-as-a-service) now accounts for 64% of the IT market, with IaaS alone reaching $14.5 billion—a 34% leap from 2024. This growth isn't just about storage or computing power; it's about enabling AI workloads that require real-time data processing, predictive analytics, and machine learning at scale.

The reveals why investors are flocking here: these platforms are the backbone of AI's infrastructure needs. Meanwhile, SaaS's 9% growth pales in comparison, as enterprises delay non-essential software upgrades until they solidify their cloud foundations.

Mega-Deals: Bigger Contracts, Fewer Risks

A strategic shift is underway. While the number of mega-deals (≥$100M) dipped slightly to eight in Q2, their combined value rose 13% year-over-year. Companies are favoring large, long-term agreements to lock in cost efficiencies and avoid vendor fragmentation. In the Americas, five mega-deals generated an 81% ACV surge, signaling a preference for consolidated partnerships over piecemeal spending.

This trend favors IT services giants like IBM and Accenture, which dominate the $500M+ deal space, but also creates openings for niche players. For instance, Cognizant's recent $1.2B deal with a European energy firm highlights how sector-specific expertise can command premium pricing.

Regional Split: Americas Lead, Europe Stumbles

The Americas are the clear growth engine:

- Managed services hit $5.9B (20% growth), with IT outsourcing (ITO) soaring 32%.

- Energy and manufacturing sectors saw over 60% growth in managed services, as companies automate supply chains and digitize operations.

Europe, however, faces headwinds:

- Managed services dipped 4% amid macroeconomic uncertainty, with BFSI contracting 8%.

- Yet, sovereign cloud initiatives in Germany and France (e.g., Gaia-X) point to long-term opportunities in data sovereignty, a theme to watch for 2026.

Sector Gold Mines: Energy, Manufacturing, and ER&D

The data reveals three high-potential sectors:

1. Energy and Manufacturing: Both saw double-digit growth in managed services as firms invest in predictive maintenance, IoT-enabled logistics, and AI-driven supply chain optimization.

2. Engineering, R&D (ER&D): Europe's 193% ER&D spending spike underscores demand for firms like Tech Mahindra or Capgemini, which specialize in digital innovation for industries.

3. Healthcare: A 33% growth rate in the Americas reflects tech investments in telemedicine platforms and patient data analytics.

Investment Playbook: Target Scalability and Sector Expertise

- Buy the Cloud Stack: Prioritize IaaS providers and hybrid cloud specialists.

- Mega-Deal Winners: Look for firms with a track record in large, multi-year contracts (e.g., DXC Technology's $2B+ deals in transportation).

- Sector Specialists: Firms like Lument Consulting (energy IT) or EPAM Systems (manufacturing AI) could outperform as sector-specific needs grow.

- Avoid Discretionary: BPO and legacy SaaS vendors face headwinds as cost-conscious buyers shift budgets to AI infrastructure.

Risk Factors to Monitor

- Geopolitical Clouds: Europe's sovereign cloud push could fragment the market, favoring local players over global giants.

- AI Overheating: A sudden slowdown in enterprise AI adoption could stall cloud spending—investors should monitor quarterly IT budgets closely.

Conclusion: Ride the Cloud, But Stay Sector-Specific

The IT services market is at an inflection pointIPCX--. While the broader sector's 17% annual growth is impressive, investors must distinguish between winners and laggards. Focus on firms that can deliver AI-ready cloud infrastructure and sector-specific managed services. Those lacking expertise in energy digitization or ER&D risk being left behind.

The data is clear: this isn't a temporary boom. With ISG上调ing its cloud growth forecast to 21% and mega-deals cementing long-term partnerships, the next 12–18 months will reward investors who bet on the right players in this AI-powered transformation.

Comentarios

Aún no hay comentarios