Clearmind Medicine's $10 Million Convertible Note Offering: A Strategic Catalyst for Growth or a Double-Edged Sword for Investors?

In the high-stakes arena of psychedelic-derived therapeutics, Clearmind MedicineCMND-- (CMND) has unveiled a $10 million convertible note offering as a strategic lifeline to fuel its ambitions. This move, structured in tranches and contingent on regulatory milestones, reflects both the company's urgent need for liquidity and its calculated pursuit of growth. However, for investors, the offering raises critical questions about dilution, financial sustainability, and the alignment of capital with long-term value creation.

Strategic Flexibility or Financial Band-Aid?

The convertible note offering is designed to provide Clearmind with a staged capital infusion, allowing it to access funds as needed. At the first initial closing, the company secured $500,000 for notes valued at $555,556—a 10% discount—while a subsequent tranche of $1,750,000 is contingent on SEC registration effectiveness [1]. Quarterly tranches of up to $2.5 million could follow, totaling $7.5 million. This structure offers flexibility, enabling Clearmind to align capital deployment with clinical milestones, such as its multinational Phase I/IIa trial for CMND-100, a treatment for Alcohol Use Disorder (AUD) [2].

The terms, however, are far from benign. Notes are issued at 90% of face value, with a variable conversion price not below $0.20 per share—a threshold that could trigger significant dilution for existing shareholders. Additionally, the 4% annual interest rate (escalating to 14% upon default) and 18-month deferral of repayment before monthly installments begin add layers of financial risk [1]. For a company with a leverage ratio of 2.3 and no revenue, these terms underscore the precariousness of its balance sheet [3].

Clinical Progress vs. Liquidity Crisis

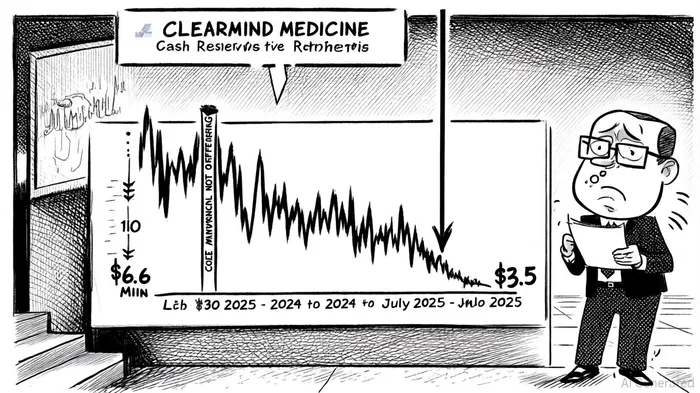

Clearmind's financial health paints a mixed picture. While R&D spending surged 83% to $1.6 million in Q3 2025, reflecting progress in its AUD pipeline, cash reserves have plummeted by 47% to $3.5 million, with operating cash outflows reaching $3.4 million over nine months [1]. This liquidity crunch has forced the company to rely on equity financing, inflating the share count by 26% to 5.4 million outstanding shares—a move that has eroded per-share value without establishing a sustainable capital base [1].

The convertible notes aim to alleviate this pressure, with proceeds earmarked for working capital, acquisitions, and general operations. Yet, the company's exposure to geopolitical instability—given its Israeli-based R&D operations—and its entanglement with related-party entities like SciSparcSPRC-- (which now accounts for $174,043 in receivables) raise governance concerns [1]. These factors could complicate capital allocation and investor confidence.

Investor Implications: Catalyst or Conundrum?

For investors, the offering represents a double-edged sword. On one hand, the capital could accelerate clinical trials for CMND-100, a drug that has already driven a 34% stock surge in July 2025 following trial initiation [2]. On the other, the dilutive nature of the notes and the company's lack of revenue create a high-stakes gamble. The conversion price of $0.20 per share, for instance, is well below the current market price (assuming a $0.50 share price), potentially triggering a 50% dilution of ownership for existing shareholders [1].

Moreover, the offering's success hinges on Clearmind's ability to meet regulatory and operational milestones. If the company fails to advance its pipeline or secure additional financing, the 14% default interest rate could exacerbate financial distress [1].

Conclusion: A Calculated Bet in a High-Risk Sector

Clearmind's convertible note offering is a strategic maneuver to bridge its liquidity gap and fund growth in a nascent but promising sector. However, the aggressive dilution, coupled with a lack of revenue and geopolitical risks, positions this move as a high-reward, high-risk proposition. Investors must weigh the potential for clinical breakthroughs against the company's financial fragility. For now, the offering buys time—but not necessarily a path to profitability.

Comentarios

Aún no hay comentarios