CleanCore's High-Risk, High-Reward Dogecoin Treasury Strategy: A Case Study in Crypto-Driven Rebranding

In the volatile world of small-cap stocks, few stories are as audacious—or as polarizing—as CleanCoreZONE-- Solutions' (NASDAQ: ZONE) 2025 pivot to a Dogecoin-centric business model. The company, which reported a 29% year-over-year revenue increase to $2.07 million in fiscal 2025[1], has simultaneously burned through $6.74 million in net losses and now faces a “going concern” warning from auditors[1]. Against this backdrop, CleanCore's decision to allocate $68 million of its treasury to DogecoinDOGE-- (DOGE)—with a stated goal of acquiring 1 billion tokens within 30 days—raises urgent questions about the viability of crypto-driven rebranding in a struggling firm.

The Financial Fragility Behind the Hype

CleanCore's core business remains a mixed bag. While U.S. revenue hit a record $1.1 million in Q4 2025[1], its G&A expenses ballooned by 187% year-over-year to $7.08 million[1], dwarfing revenue growth and underscoring operational inefficiencies. The company's audited financials for 2025 explicitly warn of “substantial doubt about its ability to continue as a going concern”[1], a red flag for investors. Compounding these issues, CleanCore reclassified $230,000 in Q3 revenue as intercompany sales post-acquisition of Sanzonate Europe Ltd., casting doubt on its financial reporting discipline[1].

Yet, rather than addressing these fundamentals, CleanCore has opted for a radical rebranding play. The company raised $175 million via a private placement involving institutional heavyweights like Pantera and FalconX[3], using the proceeds to fund its Dogecoin treasury. This move, while funded by external capital, does little to resolve its core financial challenges. For every dollar invested in Dogecoin, CleanCore's balance sheet remains burdened by liabilities that far exceed its tangible assets.

The Dogecoin Gamble: Strategic or Speculative?

CleanCore's Dogecoin strategy is framed as a “strategic reserve” initiative, positioning the meme coin as a “people's currency” with global utility[5]. The company's partnership with the Dogecoin Foundation and House of DogeDOGE--, led by CEO Marco Margiotta, adds a veneer of legitimacy[2]. However, the aggressive acquisition target—1 billion DOGE in 30 days—suggests a speculative bet on price appreciation rather than a measured approach to treasury diversification.

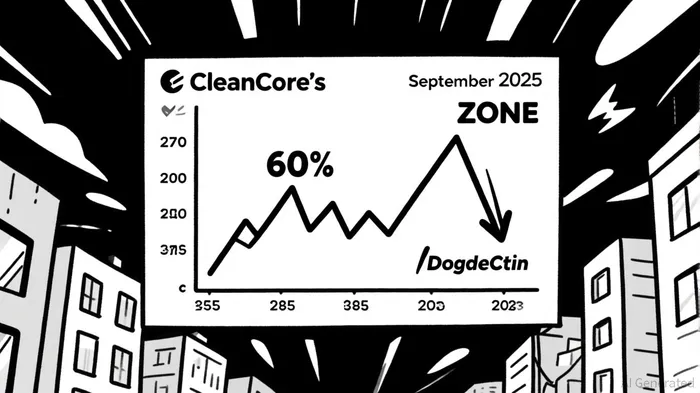

Data from CoinMarketCap highlights the risks: Dogecoin's price volatility in 2025 has been extreme, with a 30-day range of 120% as of September 2025[3]. CleanCore's treasury is exposed to this volatility, and a 50% drop in DOGE's value would erase nearly half of its $68 million investment. Worse, the company's stock price plummeted 60% following the announcement[4], indicating investor skepticism about the move's prudence.

The Broader Crypto Rebranding Trend

CleanCore is not alone in leveraging crypto for rebranding. As noted in a report by CTOL Digital, 2025 has seen a surge in corporate Dogecoin treasuries, driven by institutional interest and pending SEC ETF approvals[5]. However, CleanCore's approach diverges sharply from peers like MicroStrategy, which uses BitcoinBTC-- as a long-term hedge against inflation. Instead, CleanCore's strategy appears to prioritize hype over hedging, betting on Dogecoin's cultural cachet to attract retail investors and media attention[2].

This raises a critical question: Is CleanCore's rebranding a genuine attempt to innovate, or a desperate bid to distract from its deteriorating fundamentals? The appointment of Elon Musk's attorney, Alex Spiro, as chairman[6], and the involvement of House of Doge's Margiotta[2], suggest a calculated effort to align with high-profile crypto advocates. Yet, as Bloomberg's analysis of similar rebranding plays notes, such moves often lack substance and fail to address underlying operational weaknesses.

Risk vs. Reward: A Calculus for Investors

For investors, CleanCore's Dogecoin treasury presents a binary outcome. If Dogecoin's price surges—driven by ETF approvals or broader adoption—the company's treasury could become a valuable asset, potentially offsetting its losses. Conversely, a market downturn or regulatory crackdown could deepen its financial crisis.

A visual comparison of CleanCore's stock performance and Dogecoin's price trajectory (see chart query below) would illustrate this duality. Meanwhile, the company's reliance on private placement funding—rather than organic revenue growth—highlights its precarious liquidity position.

Conclusion: A Hail Mary or a Strategic Pivot?

CleanCore's Dogecoin treasury strategy is a high-stakes gamble. While the company's institutional backing and aggressive acquisition goals signal confidence, its financial instability and lack of a clear path to profitability make this rebranding a speculative bet. For now, the strategy appears to prioritize short-term market buzz over long-term operational health—a recipe for disaster in a sector where fundamentals ultimately prevail.

Investors should monitor two key metrics: (1) Dogecoin's price action and (2) CleanCore's ability to stabilize its core business. Until then, this rebranding remains a cautionary tale of how crypto can amplify both the potential and the peril of small-cap speculation.

Comentarios

Aún no hay comentarios