Can Circle's Interest Rate Dependence Sustain Long-Term Growth?

Circle Internet Group’s CRCL long-term growth is fundamentally tied to interest rates, making its revenue model highly macro-sensitive. The company’s business is largely driven by reserve income generated from USDC holdings, which accounted for the vast majority of its $770 million fourth-quarter 2025 revenues, with reserve income alone contributing $733 million. This highlights how closely Circle’s earnings are linked to prevailing interest rates, as higher yields on reserve assets directly boost revenues.

However, this dependence also introduces structural earnings risk. The reserve return rate declined year over year, partially offsetting the benefits of strong USDC circulation growth, which rose 72% to $75.3 billion in the reported quarter. Even with rising adoption and transaction volumes, lower interest rates can compress earnings, making revenue growth less predictable. This dynamic underscores that Circle’s model behaves more like a rate-sensitive financial platform than a traditional finance business.

To sustain long-term growth, the company is actively diversifying beyond interest income through products like CircleCRCL-- Payments Network, StableFX and its Arc blockchain infrastructure. While these initiatives are gaining traction, non-interest revenues remain relatively small compared to reserve income, indicating that diversification is still in its early stages.

CRCL’s long-term growth will depend on balancing three key levers: sustained USDC adoption, a stable or favorable interest rate environment and a faster shift toward fee-based revenue streams. The Zacks Consensus Estimate projects revenue growth of 14.5% in 2026 and 32.7% in 2027, suggesting that growth remains achievable — but ultimately conditional on macro support and successful business diversification.

CRCL Navigates a Rate-Driven Growth Challenge

PayPal Holdings PYPL competes with CRCL’s rate-driven model using transaction-based growth. It leverages its global payments network, merchant relationships and consumer engagement to drive payment volume instead of reserve yields. PYPL’s investments in checkout, BNPL and Venmo, along with crypto and wallet interoperability, support stablecoin usage in commerce. Unlike Circle’s yield focus, PYPL monetizes payment flows, making the company less sensitive to interest rate changes and better positioned as CRCL navigates a rate-driven growth challenge.

Coinbase Global COIN counters Circle’s rate-driven model with a diversified, platform-centric ecosystem. The company benefits from USDC revenue sharing but focuses on stablecoin utility in payments, trading and onchain applications. COIN’s “Everything Exchange” and strong institutional scale enhance monetization beyond reserve income. With diversified revenue streams like subscription and services, it is less sensitive to rate cycles, positioning COIN strongly as CRCL navigates a rate-driven growth challenge.

CRCL’s Share Price Performance, Valuation & Estimates

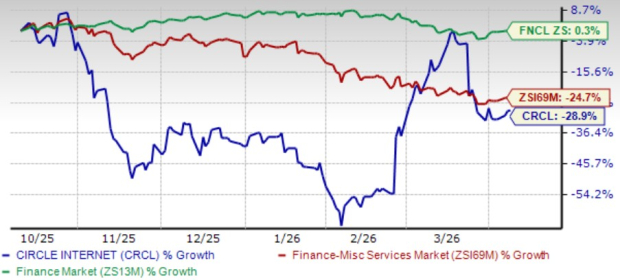

In the trailing six-month period, Circle stock has declined 28.9%, underperforming the broader Zacks Finance sector’s return of 0.3% and the Zacks Financial - Miscellaneous Services industry’s fall of 24.7%.

CRCL’s Price Performance

Image Source: Zacks Investment Research

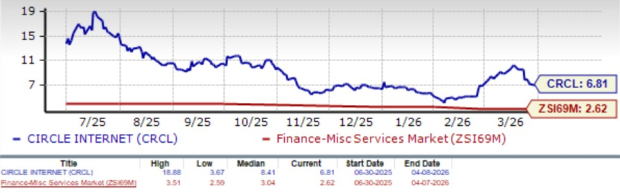

From a valuation standpoint, CRCL appears overvalued, trading at a forward 12-month price-to-sales ratio of 6.81, higher than the industry's average of 2.62. The company carries a Value Score of F.

CRCL’s Valuation

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for 2026 earnings is currently pegged at 85 cents per share, unchanged over the past 30 days. This represents a sharp year-over-year improvement from a loss of 44 cents.

Image Source: Zacks Investment Research

Circle stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

PayPal Holdings, Inc. (PYPL): Free Stock Analysis Report

Coinbase Global, Inc. (COIN): Free Stock Analysis Report

Circle Internet Group, Inc. (CRCL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios