CION's 2026 Playbook: Capturing Deal Flow While Managing Rising Risks

CION Investment Corp. CION enters 2026 with a clearer set of catalysts and constraints than it had during last year’s choppy credit backdrop. The setup is shifting as merger-and-acquisition confidence improves and macro visibility stabilizes after earlier tariff-related uncertainty.

At the same time, credit risks have risen as non-accruals moved higher in 2025, and private-credit competition has intensified. The next phase for the stock likely depends on how quickly origination rebounds and how much return potential survives tighter pricing.

CION Trend: Why Origination Could Rebound

CION’s origination outlook is tied to a more constructive transaction environment. With market sentiment recovering and merger-and-acquisition activity accelerating, the addressable opportunity set for direct lending has started to expand again. Better macro clarity after tariff-related uncertainty is also helping deal discussions move from “wait and see” to execution.

That backdrop matters because CIONCION-- is positioned to participate quickly. As of Dec. 31, 2025, the company held a well-diversified $1.70 billion portfolio across 89 companies and 22 industries, with a heavy tilt to first-lien senior secured exposure. This structure can support steady earnings while still allowing the portfolio to rotate into new opportunities as volume returns.

The most direct indicator to watch is new commitments. CION InvestmentCION-- generated $255 million of new investment commitments in 2025, and expectations call for continued improvement as lending conditions and deal activity strengthen.

The portfolio’s defensive mix also informs the outlook. As of Dec. 31, 2025, first-lien investments represented 80.8% of the portfolio at fair value, and about 98% of the portfolio was risk rated 3 or better. That base can help CION Investment pursue new commitments without needing to stretch as far down the credit spectrum to maintain activity.

CION: Monthly Payout Shift and Investor Demand

CION Investment is also adjusting how it tells its income story. The company maintained a base distribution of 36 cents per share in the fourth quarter of 2025, and it plans to shift to monthly payments in early 2026. That change can make the cash-flow profile feel more consistent for income-focused investors and may influence how the stock is compared with other yield vehicles.

The capital distribution narrative is supported by balance sheet flexibility. CION ended 2025 with $124 million in cash and short-term investments and another $100 million available under financing arrangements. Available capacity matters because it can help the company manage distributions while continuing to fund selective originations.

CION’s peers Ares Capital ARCC and Main Street Capital MAIN also pays regular dividend. Ares Capital currently pays a dividend of 48 cents per share with a payout ratio of 96% Main Street Capital currently pays a dividend of 26 cents per share with a payout ratio of 75%.

CION Investment: What to Watch Ahead

CION’s scale is also bounded by funding and regulatory realities. To comply with regulatory requirements, the company invests primarily in U.S.-based companies, with more limited foreign exposure. In a challenging macro environment, persistent regulatory constraints may raise funding costs and reduce access to capital markets, limiting how quickly the portfolio can expand. Even with improving deal flow, CION still faces a tougher pricing environment. The private credit market remains intensely competitive, with tighter spreads, elevated leverage and looser lender protections.

Liquidity and balance-sheet structure provide some cushion, but they do not remove the constraint. As of Dec. 31, 2025, CION’s liabilities were largely unsecured, and its debt mix was about 65% unsecured and 35% senior secured, supporting flexibility. Leverage stood at 1.44X net debt-to-equity, reinforcing a disciplined posture as funding costs and capital access remain central to the growth equation.

From an investor standpoint, the near-term setup remains mixed. CION currently carries a Zacks Rank #5 (Strong Sell), reflecting the balance between improving origination drivers and the headwinds of credit risk, competition, and potential constraints on scaling.

CION Investment’s Zacks Rank & Price Performance

CION carries a Zacks Rank #5 (Strong Sell), which aligns with a measured stance into 2026.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

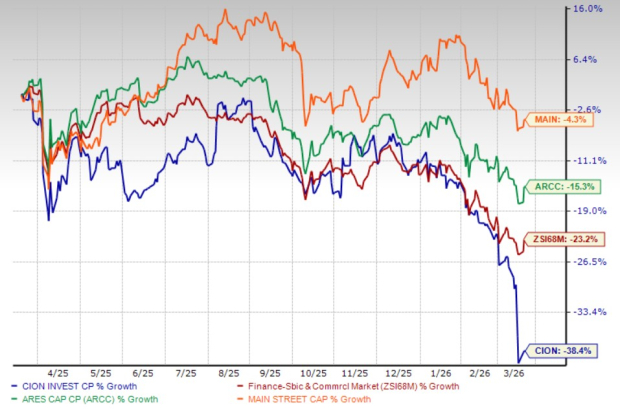

The stock has also lagged in the past year, with shares down 38.4% compared with the industry’s decline of 23.2%. Its peers, ARCC and MAIN shares fell 15.3% and 4.3%, respectively, over the same time frame.

Price Performance

Image Source: Zacks Investment Research

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ares Capital Corporation (ARCC): Free Stock Analysis Report

Main Street Capital Corporation (MAIN): Free Stock Analysis Report

CION Investment Corporation (CION): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios