Churchill Downs CHDN 2025Q2 Earnings Preview Downside Risk Amid Lower EPS Forecasts

Generado por agente de IAAinvestweb

domingo, 20 de julio de 2025, 9:12 pm ET1 min de lectura

CHDN--

Forward-Looking Analysis

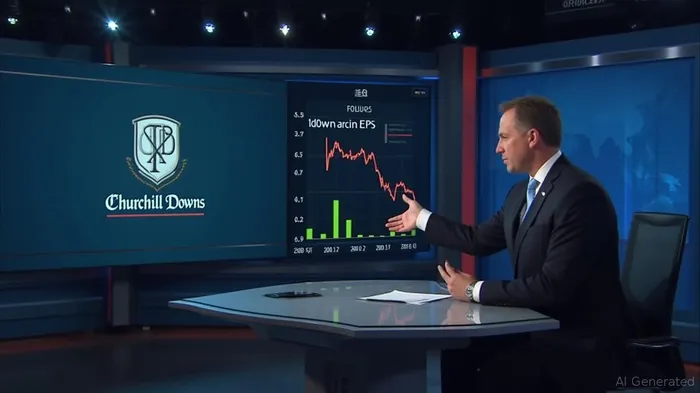

Analysts have adjusted expectations for Churchill Downs' Q2 2025 earnings, reflecting a significant reduction in EPS forecasts over the past year. The EPS is expected to drop from $1.40 to $1.12, marking a 19.9% decrease. Despite previous forecasts predicting revenues of $2.95 billion and EPS of $6.50 for 2025, recent results have prompted a slight dip in overall sentiment, with revised forecasts projecting revenues of $2.92 billion and EPS of $6.26. Analysts have also lowered the consensus price target by 7% to $138, indicating a lack of confidence in the stock's performance amid lower earnings expectations. While revenue growth is anticipated at a modest 4.9%, it is expected to lag behind the industry's projected growth rate of 9.8%. This decline in sentiment suggests potential downside risks, despite stable revenue estimates.

Historical Performance Review

In the first quarter of 2025, Churchill DownsCHDN-- reported revenue of $642.60 million and net income of $77.20 million, translating to an EPS of $1.02. The gross profit for this period stood at $189.50 million, reflecting a steady financial performance. While the EPS fell short of market expectations, the company managed to align with analyst predictions, maintaining its operational stability.

Additional News

Recently, Churchill Downs IncorporatedCHDN-- (NASDAQ:CHDN) has seen its stock price decline by 13% to $88.35 following its quarterly report. Despite meeting analyst predictions with revenues of $643 million and statutory earnings per share of $1.02, there has been a notable shift in investor sentiment. Analysts have updated their earnings models due to these results, indicating a potential reassessment of the company's future prospects. While the business appears to be executing in line with its plans, the consensus price target has fallen, reflecting the analysts' caution in their valuation of Churchill Downs.

Summary & Outlook

Churchill Downs faces a challenging outlook with downgraded earnings per share estimates and a reduced consensus price target, indicating bearish sentiment. Although the company maintains stable revenue estimates, it is expected to grow slower than industry peers, posing a risk to its long-term growth trajectory. With the stock experiencing a significant decline, investors should be cautious amid lower forecast earnings. The company's future prospects remain uncertain as analysts continue to reassess its valuation in the face of these challenges.

Analysts have adjusted expectations for Churchill Downs' Q2 2025 earnings, reflecting a significant reduction in EPS forecasts over the past year. The EPS is expected to drop from $1.40 to $1.12, marking a 19.9% decrease. Despite previous forecasts predicting revenues of $2.95 billion and EPS of $6.50 for 2025, recent results have prompted a slight dip in overall sentiment, with revised forecasts projecting revenues of $2.92 billion and EPS of $6.26. Analysts have also lowered the consensus price target by 7% to $138, indicating a lack of confidence in the stock's performance amid lower earnings expectations. While revenue growth is anticipated at a modest 4.9%, it is expected to lag behind the industry's projected growth rate of 9.8%. This decline in sentiment suggests potential downside risks, despite stable revenue estimates.

Historical Performance Review

In the first quarter of 2025, Churchill DownsCHDN-- reported revenue of $642.60 million and net income of $77.20 million, translating to an EPS of $1.02. The gross profit for this period stood at $189.50 million, reflecting a steady financial performance. While the EPS fell short of market expectations, the company managed to align with analyst predictions, maintaining its operational stability.

Additional News

Recently, Churchill Downs IncorporatedCHDN-- (NASDAQ:CHDN) has seen its stock price decline by 13% to $88.35 following its quarterly report. Despite meeting analyst predictions with revenues of $643 million and statutory earnings per share of $1.02, there has been a notable shift in investor sentiment. Analysts have updated their earnings models due to these results, indicating a potential reassessment of the company's future prospects. While the business appears to be executing in line with its plans, the consensus price target has fallen, reflecting the analysts' caution in their valuation of Churchill Downs.

Summary & Outlook

Churchill Downs faces a challenging outlook with downgraded earnings per share estimates and a reduced consensus price target, indicating bearish sentiment. Although the company maintains stable revenue estimates, it is expected to grow slower than industry peers, posing a risk to its long-term growth trajectory. With the stock experiencing a significant decline, investors should be cautious amid lower forecast earnings. The company's future prospects remain uncertain as analysts continue to reassess its valuation in the face of these challenges.

Divulgación editorial y transparencia de la IA: Ainvest News utiliza tecnología avanzada de Modelos de Lenguaje Largo (LLM) para sintetizar y analizar datos de mercado en tiempo real. Para garantizar los más altos estándares de integridad, cada artículo se somete a un riguroso proceso de verificación con participación humana.

Mientras la IA asiste en el procesamiento de datos y la redacción inicial, un miembro editorial profesional de Ainvest revisa, verifica y aprueba de forma independiente todo el contenido para garantizar su precisión y cumplimiento con los estándares editoriales de Ainvest Fintech Inc. Esta supervisión humana está diseñada para mitigar las alucinaciones de la IA y garantizar el contexto financiero.

Advertencia sobre inversiones: Este contenido se proporciona únicamente con fines informativos y no constituye asesoramiento profesional de inversión, legal o financiero. Los mercados conllevan riesgos inherentes. Se recomienda a los usuarios que realicen una investigación independiente o consulten a un asesor financiero certificado antes de tomar cualquier decisión. Ainvest Fintech Inc. se exime de toda responsabilidad por las acciones tomadas con base en esta información. ¿Encontró un error? Reportar un problema

Comentarios

Aún no hay comentarios