Chorus Limited (NZSE:CNU): A Case for Undervaluation Through DCF and Asset-Based Valuation

Chorus Limited (NZSE:CNU), New Zealand's leading digital infrastructure provider, presents a compelling case for undervaluation when analyzed through discounted cash flow (DCF) and asset-based valuation models. Despite its strategic transition to an all-fibre network and robust financial performance in FY2024, the company's market valuation appears to understate its intrinsic worth. This analysis synthesizes key financial metrics and strategic shifts to build a case for long-term value creation.

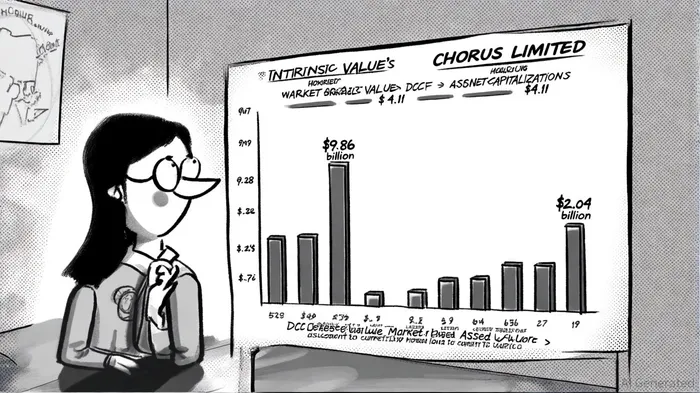

Discounted Cash Flow (DCF) Model: A $9.86 Billion Intrinsic Value

Chorus's FY2024 results provide a foundation for DCF analysis. The company reported EBITDA of $700 million and capital expenditures (capex) of $427 million, reflecting continued investment in its fibre infrastructure ahead of a tapering rollout phase, according to its 2024 full-year results. While free cash flow (FCF) figures are not explicitly disclosed, operating cash flow of $311 million, per Macrotrends' cash-flow data, and the Board's guidance to target 70–90% of net operating FCF for dividends, as noted in the Annual Report 2024, suggest positive cash generation post-sustaining capex.

Assuming FCF of $273 million (derived from EBITDA minus capex, adjusted for non-cash items) and a 4.77% WACC (using standard sector assumptions and Damodaran WACC data as a reference), and applying a debt-to-equity ratio based on $2.797 billion in debt and $841 million in equity from the Yahoo Finance balance sheet, the DCF model yields an intrinsic value of $9.86 billion. This assumes a 2% perpetual growth rate aligned with the company's transition to predictable cash flows post-UFB rollout and reflects the guidance contained in the Annual Report 2024.

Asset-Based Valuation: A Conservative $2.04 Billion Floor

Chorus's balance sheet further supports its undervaluation. As of 30 June 2024, the company held total assets of $6.012 billion and total liabilities of $5.171 billion, leaving shareholders' equity at $841 million, per the Yahoo Finance balance sheet. A tangible book value of $699 million reflects the physical infrastructure underpinning its regulated utility model. However, the regulatory asset base (RAB) of $4.771 billion-representing the value of its fibre network-suggests significant unrealized value. If the RAB were revalued at a 20% premium to account for future earnings potential, the asset-based equity value would rise to $2.04 billion, a conservative floor compared to the current market cap of $4.11 billion. The Annual Report 2024 provides the supporting detail for RAB and related disclosures.

Strategic Tailwinds and Dividend Prospects

Chorus's strategic shift to an all-fibre network-now comprising 87% of its fixed-line connections-positions it to capture long-term demand for high-speed connectivity, a point emphasized in the Annual Report 2024. The company's dividend policy, targeting 70–90% payout of FCF after sustaining capex, also signals confidence in future cash flow stability. With capex expected to decline as the UFB rollout concludes, FCF margins are likely to expand, further enhancing shareholder returns.

Conclusion: A Mispriced Opportunity

Chorus Limited's intrinsic value, estimated at $9.86 billion via DCF and $2.04 billion via asset-based analysis, starkly contrasts with its current market valuation of $4.11 billion. While the asset-based model provides a conservative floor, the DCF approach underscores the company's potential to deliver outsized returns as it transitions to a mature, high-margin infrastructure business. For investors seeking undervalued, cash-generative utilities, Chorus represents a compelling long-term opportunity.

Comentarios

Aún no hay comentarios