ChoiceOne Financial Services' Q3 2025 Outperformance: A Deep Dive into Operational Efficiency and Market Resilience

Operational Efficiency: A Catalyst for Earnings Growth

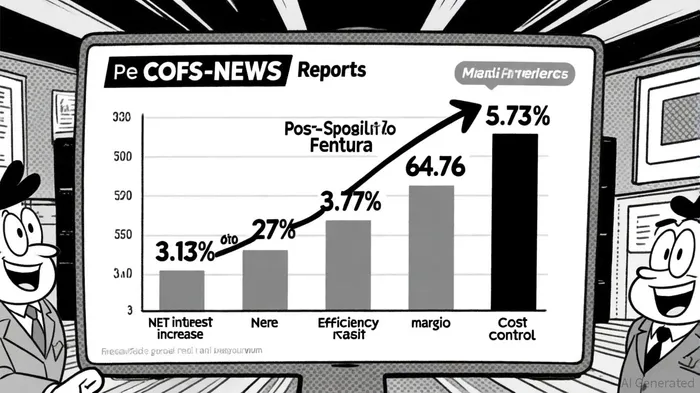

COFS' Q3 success is rooted in its ability to optimize cost structures and enhance revenue-generating activities. The company's GAAP net interest margin (NIM) expanded to 3.73% in Q3 2025, up from 3.17% in the same period of 2024, according to a ChoiceOne press release. This improvement reflects a combination of rate hikes and strategic asset management, particularly following the March 2025 merger with Fentura. The press release said the merger added $1.4 billion in core loans and $1.3 billion in deposits, amplifying the company's earning asset base.

Cost discipline further bolstered efficiency. The efficiency ratio-a key metric of operational effectiveness-dropped to 54.76%, according to a Panabee analysis. This decline was driven by economies of scale post-merger, despite one-time integration costs of $13.9 million, noted in a StockTitan report. Such cost management is critical in an environment where margin compression remains a risk for many financial institutions.

Market Resilience: Navigating Risks and Capitalizing on Opportunities

COFS' resilience is equally tied to its ability to adapt to macroeconomic headwinds. The company's asset quality remains robust, with annualized net loan charge-offs at 0.03% and nonperforming loans at 0.69% of total loans, as the ChoiceOne press release reports. These metrics suggest prudent risk management, a critical factor in maintaining investor confidence during periods of economic uncertainty.

However, challenges persist. The company's exposure to non-owner occupied Commercial Real Estate (CRE) loans-275.2% of total capital-poses a concentration risk, according to the Panabee analysis. Additionally, a shift in deposit mix, with higher-cost interest-bearing deposits replacing non-interest-bearing ones, could pressure net interest margins in a rate-cutting environment, as the Panabee analysis warns. The presence of $1.2 billion in uninsured deposits (33.2% of total deposits) further amplifies liquidity risks, the StockTitan report notes.

Strategic Outlook: Balancing Growth and Prudence

While COFS' Q3 results are commendable, the path forward requires careful navigation. The company's adjusted diluted earnings per share (EPS) reached $2.76 for the nine months ending September 30, 2025, demonstrating underlying profitability, the StockTitan report noted. However, the anticipated recognition of $51.1 million in interest income from purchased loans-$8.2 million of which is expected in 2026-suggests that future gains may be front-loaded, according to the StockTitan report. Investors must weigh these near-term tailwinds against structural vulnerabilities, such as CRE concentration and deposit mix dynamics.

Conclusion

ChoiceOne Financial Services' Q3 2025 outperformance is a testament to its operational agility and strategic foresight. By leveraging the Fentura merger to boost margins and manage costs, COFS has demonstrated a blueprint for resilience in a challenging market. Yet, the company's exposure to CRE and liquidity risks underscores the need for continued vigilance. For investors, the key will be monitoring how COFS balances growth ambitions with risk mitigation in the quarters ahead.

Comentarios

Aún no hay comentarios