Chinese Regional Banking Sector Resilience: Navigating Profitability Challenges and Earnings Momentum

The Chinese regional banking sector has entered a period of prolonged stress, marked by declining profitability metrics, sluggish loan growth, and systemic risks from the property market downturn. While state-owned commercial banks have historically dominated the landscape, regional institutions-often more exposed to local economic fluctuations-are now facing a critical test of resilience. This analysis examines the sector's profitability trends, policy interventions, and contrasting performances to assess its long-term viability for investors.

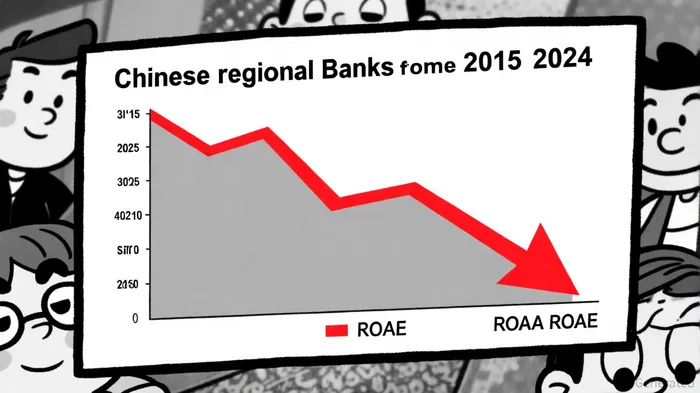

Profitability Metrics: A Decade of Decline

Chinese regional banks have seen their profitability metrics plummet to decade lows, driven by a confluence of macroeconomic headwinds. Return on average assets (ROAA) for Chinese banks dropped to 0.71% in 2024, down from 1.07% in 2015, while return on equity (ROAE) fell to 8.71% from 14.99% in the same period, according to an S&P Global analysis. Net interest margins (NIM), a critical indicator of banking sector health, have also contracted sharply, reaching 1.46% in 2024-a 42% decline from 2015 levels. These trends underscore a sector grappling with low-interest-rate environments, weak credit demand, and rising nonperforming loans, particularly in the property and retail sectors, according to an S&P Global report.

The property market crisis has further exacerbated these challenges. With nonperforming assets in the sector projected to hover between 5.5% and 5.9% over the next two years, regional banks-often more reliant on local real estate financing-face heightened credit risk. Deloitte's 2024 analysis highlights that even listed banks are struggling to balance asset quality with capital adequacy, as regulatory pressures mount.

Policy Interventions: A Mixed Bag of Relief

The People's Bank of China (PBOC) has deployed aggressive measures to stabilize the sector, including cutting benchmark lending rates to record lows and implementing a 12 trillion yuan debt swap package to ease local government debt burdens. In October 2024, authorities also allowed homeowners to renegotiate mortgage terms, aiming to reduce default risks and stimulate credit demand. These interventions have provided temporary relief, but their long-term efficacy remains uncertain.

For instance, while capital injections of 1 trillion yuan into the six largest state-owned banks have bolstered their balance sheets, regional institutions-often excluded from such largesse-continue to face liquidity constraints. The PBOC's rate cuts, meanwhile, have compressed NIMs further, squeezing margins at a time when loan growth is already slowing. In Q3 2024, aggregate NIMs for Chinese commercial banks fell to 1.53%, a 20 basis point drop year-over-year.

Contrasting Performances: Governance and Innovation as Lifelines

Amid the broader sector's struggles, some regional banks have demonstrated resilience through governance reforms and technological integration. For example, Bank of Marin Bancorp (BMRC), a U.S. regional bank with operations in China, reported a 65% year-over-year increase in net income during Q3 2025, showcasing the potential for innovation-driven profitability, according to BMRC's Q3 results. While BMRC is not a Chinese bank, its success highlights the importance of digital transformation and AI-driven risk management-strategies Deloitte has emphasized as critical for Chinese regional banks.

Non-state shareholders in Chinese state-owned enterprises (SOEs) also offer a glimmer of hope. Research indicates that non-state governance improves earnings quality in SOEs, particularly in regions with weak marketization, according to a ScienceDirect study. This suggests that private sector involvement in regional banks could enhance transparency and operational efficiency, mitigating some of the sector's systemic risks.

Outlook and Investment Considerations

The path forward for Chinese regional banks remains fraught with uncertainty. While policy interventions may stabilize the sector in the short term, structural challenges-including property market woes and geopolitical tensions-will likely persist. Investors should monitor key metrics such as NIMs, nonperforming loan ratios, and capital adequacy ratios for early signs of recovery.

For those willing to take a long-term view, opportunities may emerge in banks that prioritize digital transformation and governance reforms. However, given the sector's exposure to macroeconomic volatility, a cautious approach is warranted. As one analyst noted, "The Chinese regional banking sector is at a crossroads-resilience will depend on how effectively banks can adapt to a new normal of slower growth and tighter credit conditions."

Comentarios

Aún no hay comentarios