ChargePoint: Is the EV Charging Giant a Value Trap?

The EV charging industry is at a crossroads. As automakers and governments push for electrification, companies like ChargePointCHPT-- face a paradox: improving unit economics amid structural headwinds that threaten long-term viability. With a 20% year-over-year surge in subscription revenue and gross margins climbing from 6% to 24% in fiscal 2025, ChargePoint appears to be turning a corner according to ChargePoint's fiscal 2025 results. Yet, its networked charging systems revenue plummeted 35% in the same period, and the company still posted a $57.1 million net loss in Q1 2026, as shown in the Q1 2026 results. Is this a classic value trap-a stock that looks cheap but hides insurmountable challenges-or a resilient player navigating a turbulent market?

Structural Headwinds: Beyond the Numbers

ChargePoint's financials reflect a broader industry crisis. Public charging stations in the U.S. have an average reliability score of just 78%, with one in five units nonfunctional, according to a Harvard study. For a company reliant on hardware deployment, this spells trouble. Networked charging systems revenue dropped 20% in Q1 2026 to $52.1 million per the Q1 2026 results, a trend mirrored across the sector as demand shifts from upfront hardware sales to recurring subscriptions. While this transition has boosted ChargePoint's gross margins to 31% (non-GAAP) in Q2 2026, the shift also underscores a harsh reality: the economics of hardware-driven growth are collapsing.

The company's liquidity-$194.5 million in cash as of Q2 2026 per the fiscal 2025 filing-provides a buffer, but its $225 million in cash at the end of fiscal 2025 has eroded by 13% in just six months. Worse, ChargePoint's debt structure offers no immediate relief, with maturities not due until 2028. This creates a false sense of security. As Bloomberg notes, "The EV charging industry is reaching a crossroads, with rising competition and declining profitability forcing operators to rethink their models." ChargePoint's path to positive EBITDA by 2026 hinges on sustaining margin gains while scaling subscriptions-a tightrope walk in a market where 95% of users prioritize ease of use over price, according to EverCharge's 2025 report.

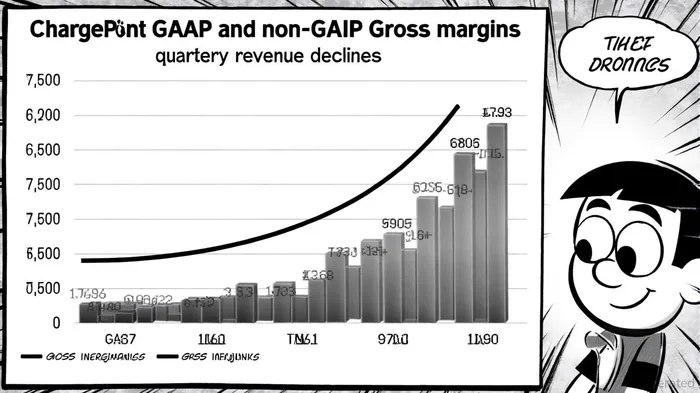

Margin Compression: A Double-Edged Sword

ChargePoint's shift to subscription revenue has been a lifeline. Subscription income grew 14% in Q1 2026 to $38.0 million (per the Q1 2026 results), contributing to non-GAAP gross margins of 31%-a 7 percentage point improvement from the prior year (per the fiscal 2025 filing). However, this progress is offset by persistent net losses. In Q1 2026, the company burned $57.1 million in GAAP net losses (per the Q1 2026 results), down from $282.9 million in fiscal 2025 (per the fiscal 2025 filing), but still unsustainable for long-term value creation.

The root cause lies in structural inefficiencies. ChargePoint's cost rationalization-GAAP operating expenses fell 26% in fiscal 2025 per the fiscal 2025 filing-has been offset by declining hardware sales. Networked charging systems revenue, once a cornerstone of growth, now accounts for just 53% of total revenue in Q1 2026 (per the Q1 2026 results), down from 56% in fiscal 2025. This shift reflects a broader industry trend: automakers and utilities are increasingly handling infrastructure deployment, leaving third-party operators like ChargePoint to compete on thin-margin services, as noted by Bloomberg.

Strategic Initiatives: Can Innovation Offset Decline?

ChargePoint's recent partnerships and product launches offer hope. A collaboration with Eaton Corporation to integrate power management solutions (reported in the Q1 2026 results) and the launch of its modular Express DC fast charging architecture (outlined in the fiscal 2025 filing) aim to reduce operational costs and attract fleet operators. These moves align with industry demands for scalable, cost-effective solutions. However, execution risks remain. The company's legal challenges-lawsuits involving former executives, according to a StockInvest digest-could divert resources from innovation, while its 15% workforce reduction in sales and marketing (per the Q1 2026 results) may weaken customer acquisition.

Moreover, the EV charging market's projected expansion to 35 million charge points by 2030 is contingent on solving "charging deserts" and pricing transparency issues, as highlighted in the Harvard study and the EverCharge report. ChargePoint's focus on urban and affluent areas noted in the EverCharge analysis risks exacerbating equity gaps, potentially alienating regulators and policymakers who prioritize inclusive infrastructure.

Conclusion: A Value Trap or a Turnaround Story?

ChargePoint's financial improvements are undeniable, but they mask deeper structural flaws. The company's reliance on subscription revenue, while margin-boosting, cannot offset the collapse of its hardware business. With revenue declining 9% year-over-year in Q1 2026 (per the Q1 2026 results) and net losses persisting, investors must ask: Is this a temporary setback, or a symptom of a dying business model?

The answer lies in ChargePoint's ability to execute its strategic initiatives. If the Express DC architecture and Eaton partnership drive meaningful cost savings and market share gains, the company could yet achieve its EBITDA-positive target. However, given the industry's reliability issues, pricing chaos, and uneven access documented in the Harvard study, the odds remain stacked against it. For now, ChargePoint appears to be a cautionary tale: a company with promising metrics but a business model in existential flux.

Comentarios

Aún no hay comentarios