CEL-SCI's $5.7M Stock Offering: A Lifeline for Multikine or a Signal of Strained Viability?

CEL-SCI Corporation's recent $5.7 million stock offering has reignited investor interest in its lead asset, Multikine—a neoadjuvant immunotherapy for head and neck cancer. But beneath the surface of this high-stakes clinical play lies a pressing question: Can the offering stave off liquidity pressures long enough for Multikine to secure FDA approval, or is it a stopgap measure in a race against time?

Strategic Urgency: Cash Burn and the Multikine Pivot

CEL-SCI's survival hinges on its ability to fund the confirmatory Registration Study for Multikine, which targets 212 patients and could determine the therapy's regulatory fate. The company's recent offerings—$5.7 million at $3.82/share and a prior $5 million offering at $2.50/share—are explicitly tied to advancing this trial. However, the urgency stems from its dire cash position:

As of Q1 2025, CEL-SCICVM-- reported just $1.93 million in cash, with net losses widening to $7.1 million in Q1 and $6.6 million in Q2. Even with the $5.7 million infusion, the burn rate suggests runway of only 6–8 months—assuming no further dilution. The current ratio of 0.55 (liabilities > liquid assets) and negative EBITDA of -$23.94 million over 12 months underscore the fragility of its financial footing.

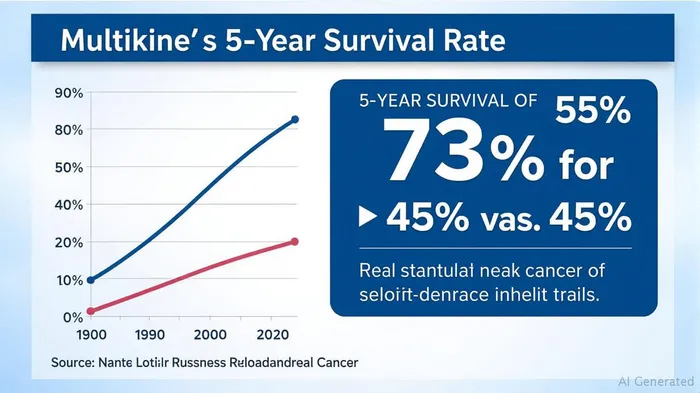

The stakes are existential. Multikine's prior trial showed a 73% 5-year survival rate versus 45% for standard care—a breakthrough that earned FDA Orphan Drug designation. Yet without FDA approval, CEL-SCI's pipeline remains theoretical. The company's Saudi partnership—seeking Breakthrough Medicine Designation from the SFDA—could fast-track Multikine's availability in the kingdom within months, but U.S. approval remains the ultimate prize.

FDA Approval Path: Hurdles and Catalysts

Multikine's path to FDA approval is fraught with risks but offers outsized rewards. The confirmatory trial's success hinges on replicating prior results in a population with low PD-L1 expression, a subset where standard therapies often fail. Positive data could catalyze a valuation jump, but failure would likely crater the stock.

The FDA's stance on immunotherapies for head and neck cancer is a wildcard. Keytruda (pembrolizumab) and other checkpoint inhibitors have reshaped standards of care, but Multikine's mechanism—a mix of cytokines to boost T-cell activity—could carve a niche. Regulatory clarity is critical: the FDA's guidance on trial design, endpoints, or accelerated approval pathways could make or break the timeline.

CEL-SCI's Saudi pivot adds another layer. If Multikine secures SFDA approval, Saudi Vision 2030 healthcare goals could fast-track commercialization, generating early revenue and bolstering credibility with U.S. regulators. However, this does not substitute for FDA approval, which remains the linchpin of long-term value.

Investment Considerations: High Risk, High Reward

Investors face a binary bet: Multikine's success versus the company's liquidity collapse. Key metrics to monitor include:

- Clinical Milestones: Confirmatory trial enrollment pace and interim data (if released).

- Cash Position: Post-offering liquidity ($5.7M + prior $5M) versus quarterly burn.

- Partnerships: Progress with Saudi entities and potential U.S. collaborations.

The stock's current price near $3.82 reflects this duality. Bulls see a $20+ potential if Multikine wins FDA approval, while bears note that CEL-SCI has burned through $11.7M in the first half of 2025 alone. The dilution from recent offerings—issuing 1.5 million shares at $3.82 and 2 million at $2.50—adds to the risk, especially if the stock sinks further.

Conclusion: A High-Stakes Gamble

CEL-SCI's $5.7M offering buys time, but not certainty. The company is betting its future on Multikine's trial success and Saudi partnerships, while navigating a liquidity crunch. For investors, this is a “all-in” proposition: the upside is transformative, but the downside is terminal.

Investment Advice:

- Aggressive investors: Consider a small position with a tight stop-loss, targeting catalysts like trial data or Saudi approval.

- Conservative investors: Avoid. The risk of cash exhaustion before pivotal milestones is too high.

The next 12–18 months will determine whether Multikine becomes a therapeutic breakthrough—or whether CEL-SCI's story ends in the annals of biotech cautionary tales.

This analysis is for informational purposes only. Investors should conduct their own research and consult a financial advisor before making decisions.

Comentarios

Aún no hay comentarios