CarMax's Q3 2025 Earnings Miss: Navigating Market Shifts and Operational Challenges in the Used-Car Sector

CarMax's Q3 2025 earnings report revealed a complex interplay of resilience and vulnerability in the used-car market. While the company reported a 1% year-over-year increase in total net sales to $6.22 billion, according to a Yahoo analysis, it fell short of analyst expectations for retail revenue ($6.59 billion vs. $7.07 billion projected), per that same Yahoo analysis. This miss, coupled with a 3.9% decline in average selling prices, according to a Panabee report, underscores the challenges of navigating a market shaped by shifting consumer behavior, inventory dynamics, and pricing pressures.

Operational Sustainability: Profitability vs. Revenue Headwinds

Despite the revenue shortfall, CarMax's net income surged 53% to $125.4 million, driven by disciplined cost management and higher gross profit per unit, according to a backtest analysis. However, earnings per share (EPS) of $0.81 lagged behind the $1.05 forecast, signaling lingering operational inefficiencies noted in the Yahoo analysis. The company's 5.4% year-over-year increase in retail used vehicle unit sales identified by the backtest was offset by weak demand in Q2 2026, where comparable store sales dropped 6.3%, according to a LinkedIn analysis. Analysts attribute this to a demand pull-forward caused by earlier tariff speculation and a misalignment between pricing and market realities described in the Yahoo analysis.

CarMax's SG&A expenses, while reduced by 1.6% year-over-year in Q2 2026 as reported in the LinkedIn analysis, remain a critical focus. The company announced a $150 million cost-cutting plan over 18 months in that same LinkedIn article, reflecting its commitment to preserving margins amid shrinking profit pools. This contrasts with competitors like Penske Automotive, whose SG&A expenses rose 3.8% year-over-year, consuming 72% of gross profit in Q1 2025 per the LinkedIn analysis. Sonic Automotive, meanwhile, demonstrated tighter SG&A leverage in its EchoPark segment, with expenses declining by 110 basis points sequentially, as discussed in the Yahoo analysis.

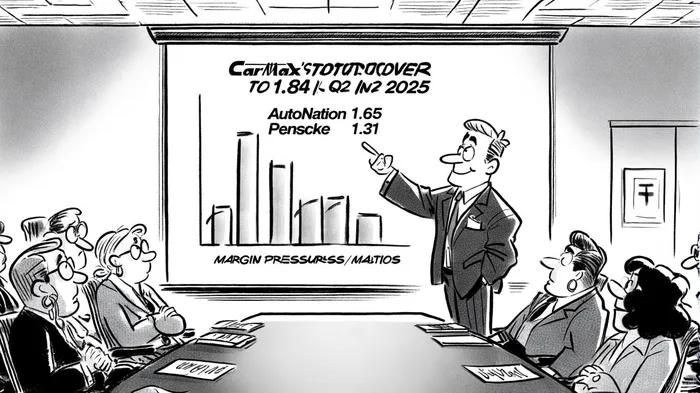

Competitive Positioning: Digital Disruption and Traditional Resilience

CarMax's dominance in the used-car market-selling twice as many vehicles as its nearest rival, according to the Yahoo analysis-is being tested by both digital disruptors and traditional dealerships. Online platforms like Carvana, with their AI-driven efficiency, and omnichannel competitors like AutoNation, which reported a 6% revenue growth in Q2 2025 per the Yahoo analysis, are reshaping consumer expectations. AutoNation's inventory turnover ratio of 1.65, according to Macrotrends, lags behind CarMax's 1.84 reported in the LinkedIn analysis, but its diversified portfolio of franchised dealerships provides a buffer against market volatility.

The broader used-car market, however, remains a double-edged sword. Inventory levels hit 2.21 million units in September 2025, according to a Cox Automotive report, the highest of the year, yet CarMax's Q2 2025 earnings miss triggered a 19–23% stock plunge reported by Panabee. High interest rates and affordability gaps between new and used vehicles discussed in the LinkedIn analysis have created a paradox: while demand persists, pricing power is eroding. CarMax's strategy to boost inventory of newer pre-owned cars, outlined in the LinkedIn analysis, and its "Wanna Drive" marketing campaign noted in the Yahoo analysis aim to capture this segment, but execution risks remain.

Long-Term Outlook: Balancing Innovation and Margin Pressure

CarMax's ability to sustain growth hinges on its capacity to harmonize digital innovation with operational efficiency. Its 2.79% net margin cited in the Yahoo analysis outperforms competitors' average of 24.94% revenue growth but lags in absolute terms. Sonic Automotive's EchoPark segment, with a 128% year-over-year adjusted EBITDA increase, illustrates the potential for niche differentiation in the used-car space as discussed in the Yahoo analysis.

For CarMaxKMX--, the path forward requires dynamic pricing adjustments, inventory optimization, and continued SG&A reductions highlighted in the Yahoo analysis. Analysts are probing management on credit expansion strategies and cost-cutting measures raised in the Yahoo piece, recognizing that CarMax's $18.95 billion FY2021 revenue base must adapt to a market where affordability and transparency are paramount.

Conclusion

CarMax's Q3 2025 earnings miss is a symptom of broader industry turbulence rather than a standalone failure. While its profitability metrics remain robust, the company must navigate a landscape where digital competitors and traditional rivals are both innovating and consolidating. For investors, the key question is whether CarMax's $150 million cost-cutting plan described in the LinkedIn analysis and omnichannel enhancements can offset margin pressures and sustain its leadership in a market projected to grow on the back of affordability gaps. The answer will depend on its agility in balancing inventory turnover, pricing discipline, and customer experience-a test that will define its long-term competitiveness.

Historical backtesting of KMX's earnings misses from 2022 to 2025, as documented in the backtest analysis, reveals a pattern of sustained downward pressure. A simple buy-and-hold strategy following these events would have yielded an average cumulative abnormal return (CAR) of -5.8% by day 30, with negative returns becoming statistically significant from day 4 onward. The win rate of 45% further underscores the negative skew associated with earnings misses, suggesting that investors historically faced a higher likelihood of losses in the month following such events.

Comentarios

Aún no hay comentarios