Capitalization-Driven Market Performance in Q4 2025: Navigating Macroeconomic Tailwinds and Investor Behavior

The fourth quarter of 2025 has emerged as a pivotal period for capitalization-driven market performance, shaped by a complex interplay of macroeconomic tailwinds and shifting investor behavior. With inflation stubbornly above central bank targets, interest rates at restrictive levels, and global growth moderating, the relative performance of large-cap and small-cap equities has become a focal point for investors. Historical patterns and current market positioning suggest a nuanced outlook, where structural forces and cyclical dynamics collide.

Macroeconomic Tailwinds: A Mixed Bag for Market Caps

The Federal Reserve's September 2025 projections paint a landscape of moderate growth and persistent inflation, with core PCE inflation expected to remain at 3.1% in 2025 before gradually declining to 2.0% by 2028. Real GDP growth is projected at 1.6% for Q4 2025, a slowdown from earlier in the year, while unemployment is forecast to hover near 4.5% (the Fed's projections). These conditions mirror historical periods where large-cap stocks have outperformed small-cap counterparts. For instance, during the 2022–2023 rate-hiking cycle, large-cap firms with strong balance sheets and pricing power navigated higher borrowing costs more effectively, while small-cap stocks, often reliant on debt financing and more sensitive to demand shifts, lagged, as shown in a Meeder analysis.

Global headwinds further amplify this dynamic. EY's U.S. Economic Outlook notes that U.S. GDP growth is expected to decelerate to 1.8% in 2025, partly due to higher tariffs and reduced immigration-driven demand. Such macroeconomic fragility tends to favor large-cap companies, which typically have diversified revenue streams and greater operational flexibility. Energy and financial sectors, for example, are seen as "marketperform" in Q4 2025, supported by inflation-linked commodity prices and rising interest rates, according to a Schwab sector outlook. Conversely, small-cap sectors like industrials and consumer discretionary face steeper challenges, given their exposure to domestic demand and tighter credit conditions.

Investor Behavior: Shifting Alliances in a High-Yield Environment

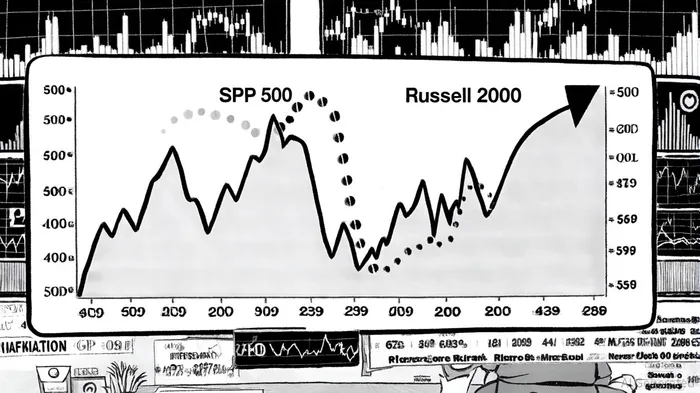

Investor behavior during tightening cycles has historically reinforced the dominance of large-cap stocks. As noted by EY's U.S. Economic Outlook, elevated interest rates weigh on business investment and consumer spending, creating a risk-averse environment where investors favor the perceived stability of large-cap equities. This trend is evident in Q4 2025 valuation metrics: the S&P 500 trades at a price-to-earnings (P/E) ratio of 27.32, classified as "overvalued" relative to its 10-year average, while the Russell 2000's P/E of 18.25, though also overvalued, reflects a narrower deviation (see major index PE ratios). Forward P/E ratios further highlight the gap, with the S&P 500 at 24.15 versus the Russell 2000's 29.97 (major index PE ratios).

However, historical cycles suggest a potential inflection point. Small-cap stocks have historically outperformed large-cap stocks during declining rate environments, and the current 12-year underperformance cycle-longer than the historical average of nine years-hints at a possible reversal, according to a CFA Institute analysis. Northern Trust's research underscores this, noting that small-cap valuations, while elevated, offer better value metrics (e.g., higher return on assets and lower price-to-book ratios) compared to the weakest segment of large-cap stocks. Additionally, a steepening yield curve-a scenario where long-term rates rise faster than short-term rates-could tilt capital flows toward small-cap equities, as seen in the 1980s and early 2000s (Meeder Investment).

Sector Rotations and Structural Shifts

Sector-specific dynamics further complicate the capitalization-driven narrative. Financials, for instance, benefit from higher interest rates through expanded net interest margins, while energy firms gain from inflation-adjusted commodity prices (Schwab sector outlook). In contrast, sectors like healthcare face downward pressure on earnings as elevated rates increase borrowing costs for capital-intensive firms (Schwab sector outlook). Cyclical sectors such as industrials may see decompression opportunities if economic growth stabilizes, while structural growth areas like AI and renewables remain insulated due to their earnings resilience (Schwab sector outlook).

Fund flows in Q4 2025 reflect a cautious posture. Large-cap equities, particularly U.S. growth stocks tied to AI-driven earnings, have attracted capital despite macroeconomic uncertainty, according to BlackRock investment directions. Meanwhile, small-cap stocks are seeing renewed interest as investors seek undervalued opportunities amid improved relative valuations and favorable interest rate dynamics (CFA Institute analysis). BlackRockBLK-- and Invesco note a broader rotation into non-U.S. equities and "risk-off" assets, signaling a diversification away from concentrated U.S. large-cap positions (BlackRock investment directions).

Conclusion: Balancing Cyclical and Structural Forces

The Q4 2025 market environment presents a delicate balance between cyclical headwinds and structural opportunities. While large-cap stocks remain favored in a high-rate, inflationary climate, historical patterns and valuation metrics suggest small-cap equities could stage a relative rebound. Investors must weigh macroeconomic risks-such as prolonged inflation or a sharper-than-expected slowdown-against structural tailwinds like AI-driven productivity gains and sector-specific resilience.

Comentarios

Aún no hay comentarios