Cannabis Operator GTBIF Stock Down 17% YTD: Should You Buy the Dip?

Shares of Green Thumb Industries GTBIF, one of the largest cannabis operators by market capitalization, have been declining over the past few years.

This pullback reflects regulatory hurdles and increasing competition in the United States cannabis market, rather than company-specific issues. Although sector sentiment briefly improved following President Trump’s push toward federal marijuana rescheduling, that move alone is unlikely to materially change the operating environment. Broader reforms, such as the SAFE Banking Act, are still required to ease capital access and reduce industry-wide financial constraints.

Let’s delve into the company’s fundamentals to better assess the stock following the decline.

Cannabis Sales Drive GTBIF's Top-line Growth

Green Thumb continues to deliver steady top-line growth, supported by resilient cannabis demand across its core U.S. markets and a well-established retail footprint. The company has benefited from strong performance in its consumer-packaged goods (CPG) portfolio, along with consistent traffic across its company-owned stores.

For full-year 2025, Green Thumb reported revenues of roughly $1.2 billion, reflecting growth of 3.4% year over year, driven primarily by retail cannabis sales and contributions from newer adult-use markets such as Minnesota. Growth was further supported by continued expansion in key markets like Florida and New York, as well as sustained demand across its branded product portfolio. During the year, the company also expanded its retail footprint by 12 locations, bringing its total store count to 113 nationwide.

While pricing pressure persists across mature markets, Green Thumb has been able to partially offset these headwinds through volume growth and a favorable product mix. Notably, the company generated $295 million in operating cash flow for the year, up roughly $100 million year over year, highlighting the strength of its operating model despite a competitive environment.

This combination of retail strength, brand leadership and disciplined execution has enabled Green Thumb to sustain stable revenue growth, positioning it favorably relative to peers even amid broader industry challenges.

Looking ahead, we expect Green Thumb to remain under pressure from persistent pricing compression in maturing markets. While the company continues to prioritize cash flow and prudent cost management, margin expansion could remain elusive without a rebound in retail pricing dynamics. Management expects first-quarter 2026 revenues to be sequentially down mid-single digits.

Stiff Competition and Limited International Exposure Weigh on GTBIF

Green Thumb operates in an increasingly competitive U.S. cannabis market, where pricing pressure and aggressive expansion strategies from peers continue to intensify. The company faces competition from players such as Cresco Labs CRLBF and Tilray Brands TLRY, both of which are actively positioning themselves for long-term growth through strategic market expansion and diversification.

A key differentiator is international exposure. Cresco Labs, historically focused on the U.S. market like Green Thumb, recently announced its entry into the German medical cannabis market, signaling a shift toward global expansion. This move could provide CRLBF with access to new growth avenues beyond the increasingly saturated U.S. landscape.

Tilray Brands, meanwhile, already has an established presence in international markets, particularly in Europe and Canada, giving it a broader geographic footprint and potential upside from global cannabis legalization trends.

In contrast, Green Thumb remains fully reliant on the U.S. market. While this focus allows it to capitalize on growth in limited-license states, it also leaves the company more exposed to domestic regulatory uncertainty and pricing pressures in maturing markets.

GTBIF Stock Performance and Estimates

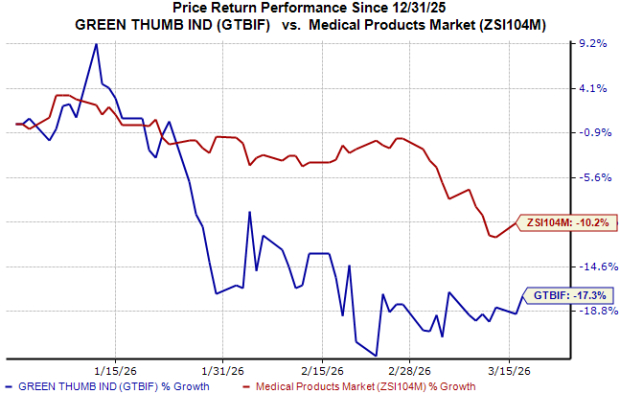

Shares of Green Thumb have underperformed the industry year to date, as shown in the chart below.

Image Source: Zacks Investment Research

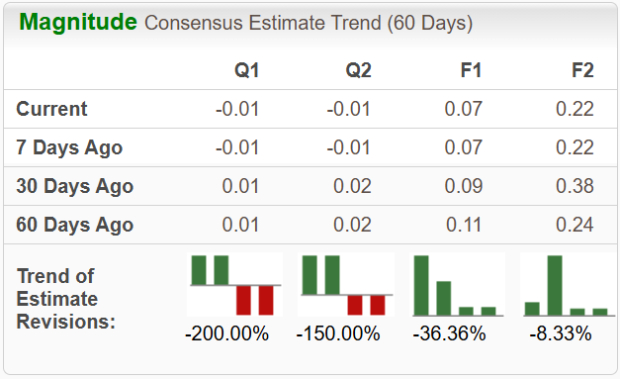

EPS estimates for 2026 and 2027 have moved south over the past 30 days.

Image Source: Zacks Investment Research

How to Play GTBIF Stock Now?

While marijuana rescheduling has improved sector sentiment, it is unlikely to materially change the near-term outlook, as broader reforms around banking and interstate commerce remain uncertain.

Green Thumb continues to generate steady revenue growth and strong cash flow, but persistent pricing pressure and its exclusive reliance on the U.S. market remain key overhangs. Declining EPS estimates for 2026 and 2027 reflect a cautious analyst outlook, signaling limited near-term earnings visibility.

Given this backdrop, existing investors may consider holding the stock, while new investors may prefer to wait for clearer signs of pricing stabilization or regulatory progress. GTBIF currently carries a Zacks Rank #3 (Hold), indicating a balanced risk-reward profile.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tilray Brands, Inc. (TLRY): Free Stock Analysis Report

Green Thumb Industries Inc. (GTBIF): Free Stock Analysis Report

Cresco Labs Inc. (CRLBF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios