Canadian Solar's Rally: A Glimmer of Hope or a Fleeting Flame in a Challenging Sector?

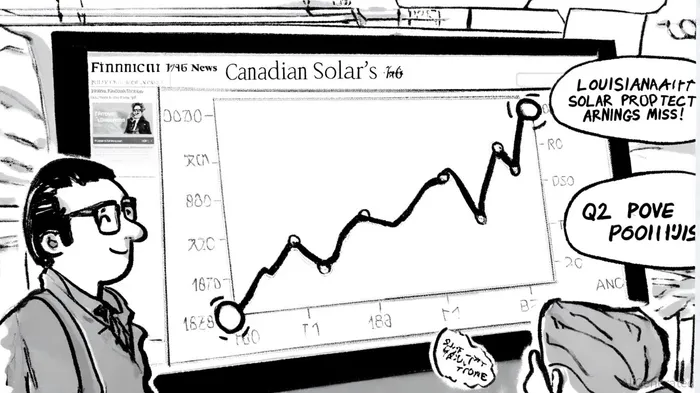

Canadian Solar Inc. (CSIQ) has experienced a notable stock rally in 2025, surging 14.65% in a single instance and gaining 15% year-to-date, according to a Benzinga price prediction. This momentum, however, raises a critical question: Is the optimism surrounding the stock sustainable amid a solar industry grappling with structural headwinds? To answer this, we must dissect the interplay between Canadian Solar's strategic initiatives and the broader challenges confronting the renewable energy sector.

Drivers of the Rally: Operational and Strategic Momentum

Canadian Solar's recent performance has been fueled by a combination of operational expansion and strategic diversification. The company's Recurrent Energy unit launched a 127 MW solar project in Louisiana, while its anti-hail solar panel technology in Australia and related developments were highlighted in a Timothy Sykes article. Meanwhile, e-STORAGE, its battery storage subsidiary, secured 420 MW / 2,122 MWh of agreements in Ontario and Chile, signaling a pivot toward energy storage-a sector poised for growth as grid stability becomes a priority.

Financially, the company reported a 14% increase in solar module shipments to 7.9 GW in Q2 2025, reflecting strong demand. However, management has warned of margin pressures due to rising supply chain costs, a challenge shared across the industry.

Structural Challenges: A Perfect Storm for the Solar Sector

The global solar industry is navigating a complex landscape of overcapacity, policy uncertainty, and technological shifts. In 2025, downstream manufacturing-particularly in China-has faced oversupply, with module production far outpacing demand, according to a PR Newswire report. This has led to depressed prices and financial strain for manufacturers, even as China's aggressive policy frameworks (e.g., 357.3 GW of 2024 installations) solidify its dominance.

In the U.S., the expiration of key solar tax credits (e.g., Section 25D for residential solar) by year-end 2025 poses a significant headwind, as detailed in the SEIA report. The One Big Beautiful Bill Act (OBBBA) further complicates matters by curtailing access to tax credits like 48E and 45Y after 2027. Meanwhile, federal permitting delays and trade barriers-such as anti-dumping duties on modules from Southeast Asia-add bureaucratic and economic hurdles, a point emphasized in a Wood Mackenzie analysis.

Technologically, the industry is shifting toward higher-efficiency solutions like TOPCon cells and hybrid systems integrating solar, storage, and smart grids. While Canadian Solar's e-STORAGE division aligns with this trend, its reliance on traditional solar modules may expose it to margin compression as competition intensifies.

Canadian Solar's Position: Strengths and Vulnerabilities

Canadian Solar's 80.2 GWh backlog provides a buffer of predictable revenue, offering short- to medium-term stability. Its international footprint-spanning projects in Louisiana, Australia, and Chile-also diversifies risk. However, the company's exposure to U.S. policy shifts and global supply chain volatility remains a concern. For instance, the U.S. solar tax credit expiration could dampen demand for its products in a key market.

The stock's recent volatility-surging on e-STORAGE deals but plunging 16% after a Q2 earnings miss-reflects investor skepticism. Analysts remain divided, with a consensus "Hold" rating and an average price target of $11.64 (a 22.86% downside from the $15.10 price as of October 2025). While Mizuho's recent "Outperform" rating with a $20 target hints at optimism, the broad range of price targets ($8–$15) underscores uncertainty.

The Canadian Context: A Mixed Outlook

Canada's solar sector is experiencing growth, driven by federal and provincial incentives like the Canada Greener Homes Loan program. However, regulatory complexities and provincial disputes over federal clean energy regulations (e.g., Alberta and Saskatchewan's constitutional challenges) create uncertainty. Canadian Solar's domestic projects, such as its Ontario battery storage agreements, position it to benefit from this growth, but logistical challenges in remote regions and competition from hydro and wind power could temper expansion.

Conclusion: A Calculated Bet Amid Uncertainty

Canadian Solar's rally is underpinned by tangible operational progress and strategic diversification into energy storage. However, the stock's long-term prospects hinge on its ability to navigate industry-wide challenges: mitigating margin pressures from supply chain costs, adapting to policy shifts, and competing in a market increasingly dominated by higher-efficiency technologies. While the 80.2 GWh backlog offers near-term stability, investors must weigh the risks of U.S. tax credit expiration and global overcapacity against the company's international expansion and innovation efforts.

For now, the stock appears to be a high-conviction play. Analysts' mixed forecasts and the broad range of price targets suggest that Canadian Solar's trajectory will depend heavily on macroeconomic developments and its execution in the coming quarters. As the solar sector evolves, Canadian Solar's ability to balance growth with resilience will determine whether its optimism is sustainable-or merely a fleeting spark.

Comentarios

Aún no hay comentarios