Campbell Soup's $0.39 Dividend: A High-Yield Paradox in a Debt-Laden Landscape

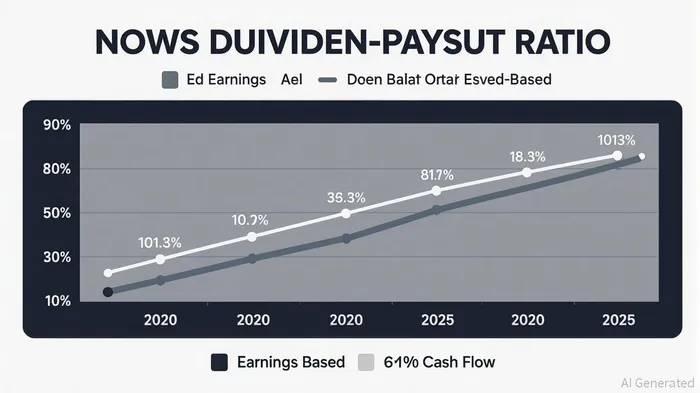

The Campbell Soup Company's $0.39 quarterly dividend, yielding 4.8% as of July 2025, appears enticing for income-focused investors. Yet, beneath the surface lies a paradox: the company's payout ratio based on net income is a staggering 101.3%[1], while its operating cash flow (OFCF) payout ratio stands at a more sustainable 61%[2]. This dichotomy underscores the fragility of the dividend's long-term viability, even as management insists on its durability.

Earnings Volatility and Cash Flow Constraints

Campbell's earnings per share (EPS) have swung wildly in recent years. In 2024, EPS fell to $1.89, a 33.7% drop from 2023's $2.85[3]. Free cash flow (FCF) has mirrored this instability, declining 13.6% to $668 million in 2024[4]. While the company's OFCF supports the current dividend, its reliance on non-cash adjustments—such as impairment charges—skews the earnings-based payout ratio. As stated by Panabee in its analysis, “The 177% earnings payout ratio is largely a function of accounting anomalies, not operational cash burn”[5].

Debt as a Double-Edged Sword

Campbell's debt load remains a critical risk. Total debt surged to $6.86 billion in 2025, a 9.1% decline from its 2024 peak of $7.18 billion[6], but still a 70% increase since 2020. The company's net debt-to-EBITDA ratio of 3.0[7] suggests progress toward its deleveraging goals, yet interest expenses have spiked 58% to $260 million for the nine months ending April 2025[8]. With a cash-to-debt ratio of 0.02[9], Campbell'sCPB-- liquidity cushion is thin, raising questions about its ability to service debt while maintaining dividend payments.

Management's Strategic Gambit

At its 2025 investor day, Campbell outlined an aggressive growth framework: 2–3% organic sales growth, 4–6% adjusted EBIT growth, and 7–9% adjusted EPS growth through 2028[10]. These targets hinge on a $250 million cost-cutting program and $215 million in capital expenditures[11]. While management cites a 61% OFCF payout ratio as evidence of dividend safety[12], the company's reliance on debt refinancing and asset sales to fund its strategy introduces uncertainty. As noted by Monexa, “The dividend's sustainability will depend on Campbell's ability to generate consistent cash flow amid a high-debt environment”[13].

The Shareholder Value Equation

Campbell's recent $2.5 billion Q3 sales increase[14] and Sovos Brands acquisition[15] signal confidence in its portfolio. However, the Snacks segment's slower-than-expected recovery[16] and elevated interest costs[17] could strain margins. For long-term shareholder value, the company must balance dividend commitments with reinvestment in growth. Its $1.85 billion unused credit facility[18] offers some flexibility, but without meaningful earnings growth or debt reduction, the 4.8% yield may prove a fleeting attraction.

Conclusion

Campbell's $0.39 dividend is a double-edged sword. While its cash flow supports the payout, the company's earnings volatility, debt burden, and reliance on non-cash adjustments create a precarious foundation. For investors, the key question is whether Campbell can execute its cost-cutting and growth initiatives without compromising its dividend. Until earnings and cash flow align more closely, the 4.8% yield remains a high-risk proposition.

Comentarios

Aún no hay comentarios