BTQ Technologies: A Quantum Leap or a Valuation Bubble?

The stock of BTQ TechnologiesBTQ-- (NASDAQ: BTQ) has surged to a market capitalization of $1.97 billion, despite generating just $653,726 in trailing 12-month revenue and reporting a net loss of $4.62 million during the same period, according to the StockAnalysis revenue breakdown. This disconnect between valuation and fundamentals raises urgent questions about overvaluation risks in a sector already grappling with speculative excess.

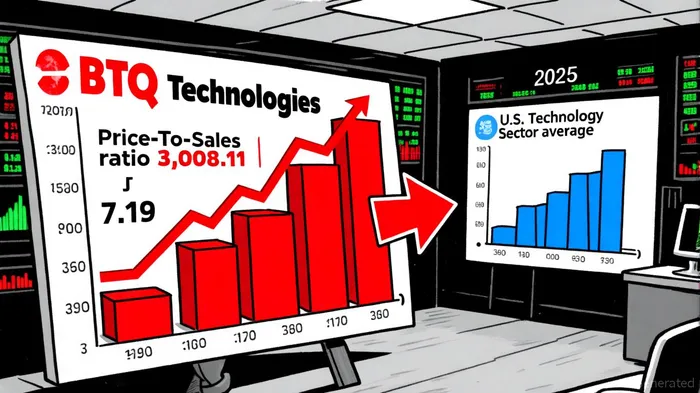

A Valuation Detached from Reality

BTQ's Price-to-Sales (P/S) ratio of 3,008.11 dwarfs the U.S. technology sector average of 7.19, per the technology sector valuation, while its Price-to-Book (P/B) ratio of 480.43 exceeds peer averages by over 75 times, according to StockAnalysis statistics. Morningstar estimates the stock trades at a 799% premium to its fair value, a metric that defies conventional logic. Such extremes are not unique to BTQ-Quantum Computing Inc. (QUBT), a direct competitor, trades at a P/S ratio of 9,663.94 according to MarketBeat's competitors page, reflecting a broader "quantum bubble" where valuations are decoupled from revenue or profitability.

The company's financials exacerbate these concerns. With a net cash position of $4.39 million and no debt, BTQ's balance sheet lacks the robustness to justify its $1.97 billion market cap. Worse, its return on equity (ROE) of -236.03% and return on assets (ROA) of -83.92%, per StockAnalysis statistics, underscore operational inefficiencies that could erode investor confidence if growth projections fail to materialize.

Strategic Alliances vs. Revenue Clarity

BTQ's business model hinges on partnerships with institutions like the University of Cambridge and QPerfect, as detailed in a PR Newswire release. While these collaborations enhance its credibility, they also obscure how the company monetizes its core offerings. For instance, PQScale, a post-quantum cryptography tool, and Keelung, a zero-knowledge proof toolkit, remain poorly defined in terms of pricing strategies or customer adoption rates, according to the FT profile.

The company's recent Nasdaq uplisting, announced in a PR Newswire release, and plans for a Quantum-Secure Custody Treasury and post-quantum hardware push detailed in a MarketChameleon article signal ambitions to scale, but these initiatives lack concrete revenue targets. Analysts project a 158.8% annual revenue growth rate through 2027, per Simply Wall St., yet such optimismOP-- is built on a base of just $0.666 million in FY 2024 revenue, according to MarketScreener. Even if these forecasts materialize, BTQBTQ-- would need to achieve $10 million in 2026 revenue to justify its current valuation-a 14,500% increase from FY 2024 levels.

Competitive Landscape and Feasibility

Quantum Computing Inc. (QUBT), BTQ's primary rival, operates in a similarly volatile space, with a beta of 4.09-309% more volatile than the S&P 500, according to MarketBeat. While QUBT's market cap ($4 billion) dwarfs BTQ's, its Q2 2025 revenue of $263K highlights the sector's collective struggle to translate innovation into earnings. BTQ's recent strategic hires, including former Radical Semiconductor executives, were announced in a PR Newswire release and may provide a temporary edge, but the absence of a clear path to profitability remains a critical vulnerability.

Strategic Alternatives for Risk Mitigation

To address overvaluation risks, BTQ must pivot from speculative growth to tangible monetization. Three alternatives merit consideration:

1. Diversification into adjacent markets: Expanding PQScale and Keelung into high-margin sectors like IoT or AI-enabled infrastructure could accelerate revenue diversification, as discussed in a guide on SaaS pricing models.

2. Strategic acquisitions: Acquiring smaller quantum startups with proven revenue models could fast-track commercialization, as seen in its QPerfect partnership announced earlier.

3. Regulatory alignment: Leveraging U.S. CNSA 2.0 and NIST standards, and pursuing government endorsement as outlined in a Qubit Report post, could secure government contracts and provide stable, long-term revenue streams.

Conclusion

BTQ Technologies occupies a precarious position at the intersection of cutting-edge quantum innovation and speculative overvaluation. While its partnerships and technological ambitions are commendable, the absence of clear revenue drivers and operational profitability poses significant risks. For investors, the key question is whether the company can bridge the chasm between its lofty valuation and its ability to deliver sustainable growth-a challenge that will define its long-term viability.

Comentarios

Aún no hay comentarios