BrightSpring Health's Post-IPO Surge: A Deep Dive into Long-Term Growth Amid Earnings Momentum

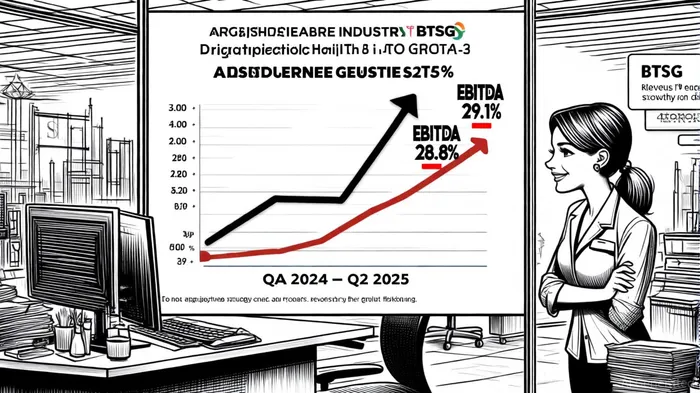

BrightSpring Health Services (NASDAQ:BTSG) has emerged as a standout performer in the post-IPO landscape, with its Q2 2025 results underscoring a compelling mix of top-line growth and operational discipline. The company reported a 29.1% year-over-year revenue increase to $3.1 billion, driven by robust contributions from its Pharmacy Solutions and Provider Services segments[2]. This performance has drawn elevated analyst expectations, with Deutsche BankDB-- and Bank of AmericaBAC-- raising their price targets to $30 and $31, respectively[1]. Yet, as investors weigh the stock's potential, a nuanced analysis of its financial trajectory, competitive positioning, and macroeconomic tailwinds is essential to assess its long-term viability.

Financial Momentum and Strategic Divestiture

BrightSpring's Q2 2025 results reflect a strategic pivot toward high-growth areas. The Pharmacy Solutions segment, which accounts for a significant portion of revenue, grew 32% year-over-year to $2.79 billion, fueled by strong demand for infusion and specialty pharmacy services. Meanwhile, the Provider Services segment expanded by 10.5%, reaching $358 million in revenue[2]. Despite these gains, net income remained flat at $8.5 million, a reflection of persistent cost pressures[2]. However, Adjusted EBITDA surged 28.8% to $142.5 million, signaling improved operational efficiency[2].

A critical catalyst for long-term growth is the company's planned divestiture of its Community Living business for $835 million, expected to close in late 2025[2]. This move is designed to streamline operations and refocus resources on the higher-margin Senior and Specialty populations. The transaction is projected to reduce the company's leverage ratio from 4.16x to 3.64x by mid-2025[2], enhancing financial flexibility and aligning with a broader industry trend of consolidation in healthcare services861198--.

Segment-Level Dynamics: Opportunities and Risks

The Pharmacy Solutions segment, while a growth engine, faces margin compression due to a strategic shift toward lower-margin specialty drugs and rising fulfillment costs[2]. Gross profit margins contracted slightly to 8.4% in Q2 2025[2], a challenge exacerbated by industry-wide pressures such as drug price transparency reforms and the adoption of biosimilars[1]. However, the segment's ability to generate 32% EBITDA growth suggests that operational efficiencies and scale are offsetting these headwinds.

In contrast, the Provider Services segment is navigating a more favorable environment. Home and community-based care demand is surging, driven by demographic shifts and policy tailwinds like the Inflation Reduction Act (IRA)[1]. BrightSpring's 11% year-over-year revenue growth in this segment[1] aligns with broader market trends, though its reliance on Medicaid reimbursement (10% of revenue[1]) introduces vulnerability to potential policy changes. Competitors like Option CareOPCH-- Health and Amedisys are also expanding in this space, with Amedisys recently announcing a merger with UnitedHealth Group[1], underscoring the competitive intensity.

Macroeconomic and Market Context

BrightSpring's trajectory must be viewed against a backdrop of U.S. trade policy uncertainty and global economic shifts. While Q2 2025 GDP growth exceeded 2%, the Federal Reserve's 4.5% policy rate[1] and the resurgence of growth-oriented sectors like technology have provided a tailwind for healthcare stocks. However, the U.S. dollar's decline against other currencies has reduced foreign investor returns[1], a factor that could influence capital flows into the sector.

The broader M&A landscape also favors BrightSpringBTSG--. With 2025 seeing heightened activity in healthcare and energy sectors[3], the company's strategic divestiture and focus on core segments position it to capitalize on consolidation opportunities. Analysts at Morgan StanleyMS-- note that a more favorable regulatory environment and increased financial sponsor activity are likely to drive cross-border deals in 2025[4], a trend that could benefit BrightSpring's growth ambitions.

Investment Thesis and Analyst Outlook

Despite near-term margin pressures, BrightSpring's financial discipline and strategic clarity have earned strong analyst backing. The company raised its 2025 guidance, projecting revenue growth of 15.2–20.1% and Adjusted EBITDA growth of 18.4–21.7%[2]. Deutsche Bank's price target increase to $30 reflects confidence in the company's ability to execute its divestiture and leverage its pharmacy and provider solutions expertise[1].

However, risks remain. The pharmacy sector's exposure to drug pricing reforms and supply chain vulnerabilities[1] could dampen margins, while the Provider Services segment's Medicaid dependency introduces regulatory uncertainty. Investors must also monitor the impact of U.S. tariffs on global supply chains, which could indirectly affect pharmaceutical costs[1].

Conclusion

BrightSpring Health's post-IPO performance demonstrates a rare combination of revenue growth, operational improvement, and strategic agility. While margin pressures and competitive dynamics pose challenges, the company's focus on high-growth segments and its planned divestiture position it to navigate these risks effectively. For investors, the key question is whether the current valuation reflects these long-term opportunities—or if the stock still offers upside as the company executes its transformation. With analysts raising their price targets and the healthcare sector poised for consolidation, BrightSpring appears well-positioned to deliver sustained value, provided it maintains its operational rigor and adapts to evolving market conditions.

Comentarios

Aún no hay comentarios