Bonds Positioning for Aggressive Fed Easing Amid Cooling Growth and Geopolitical Risks

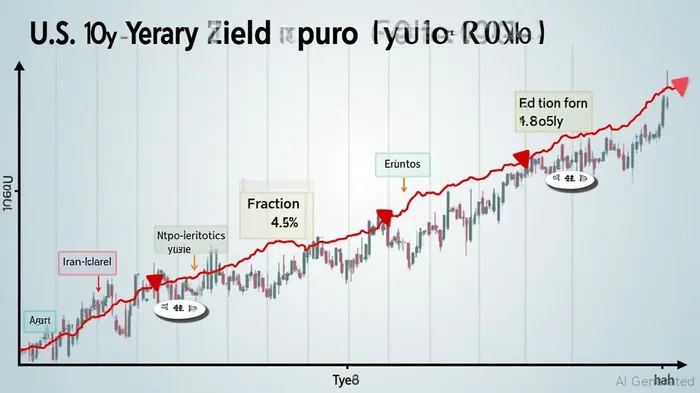

As traders bet on a historic U.S. 10-year Treasury yield decline to 4% by August 2025, markets are pricing in an aggressive pivot toward accommodative monetary policy. With the yield at 4.38% on June 19—its lowest since late April—this tactical maneuver reflects a confluence of dovish Federal Reserve signals, weakening economic data, and geopolitical de-escalation in the Middle East. Yet beneath the surface, the path to 4% remains fraught with fiscal policy uncertainty and lingering inflation risks. For investors, the question is clear: How to position for this rally without overestimating the Fed's speed—or underestimating its constraints?

The Rally to 4%: Traders' Playbook and Market Dynamics

Traders are aggressively leveraging August call options to lock in gains if yields fall to 4%, a level not seen since early 2025. Over $38 million in premiums have flowed into these contracts, targeting strike prices equivalent to a 4% yield (e.g., the 113.00 level). This positioning reflects three key catalysts:

Fed Dovishness Gains Momentum: Federal Reserve officials like Christopher Waller and Michelle Bowman have signaled openness to rate cuts as early as July, even as Chair Jerome Powell emphasized “patience.” Swaps markets now price in ~4 basis points of easing at the July FOMC meeting, with cumulative expectations rising to 60 basis points by year-end.

Economic Data Weakens: A disappointing consumer confidence reading and a 0.1% rise in May's Producer Price Index (PPI)—below forecasts—have eased inflation fears. This has emboldened traders to bet on a Fed pivot, with Treasury yields falling in tandem.

Geopolitical De-Risking: The Iran-Israel ceasefire has reduced regional volatility, boosting demand for Treasuries as a safe haven. Meanwhile, U.S.-China trade talks show incremental progress, though tariffs remain a wildcard.

Tactical Opportunities: Duration and SOFR Hedging

The race to 4% presents two strategic opportunities:

1. Long-End Duration Plays

Investors can profit from the steepening yield curve by buying long-dated Treasuries (e.g., 10- or 30-year notes). The 10-year yield's recent dip to 4.275% (June 27) underscores this trade's viability. However, duration exposure demands caution:

- Risk Management: Pair long positions with SOFR options to hedge against unexpected Fed tightening. For example, buying put options on SOFR futures protects against rate hikes.

- Key Metrics: Monitor the 2-year/10-year yield spread, which has inverted to -69 bps, signaling recession risks that could further depress yields.

2. SOFR-Linked Hedging Strategies

The Secured Overnight Financing Rate (SOFR) is now a critical benchmark for floating-rate instruments. Traders are using SOFR options to capitalize on Fed easing expectations:

- Example: Buying SOFR call options at the 95.625 strike (equivalent to a 4.375% Fed Funds Rate) provides downside protection if rates drop faster than anticipated.

Risks to the 4% Target

While momentum favors the 4% yield target, three risks could disrupt the rally:

1. Debt Ceiling Politics: Treasury Secretary Scott Bessent's warnings about August's debt ceiling deadline could reignite fiscal uncertainty, spiking yields.

2. Inflation Resurgence: A pickup in wage growth or oil prices (driven by Middle East instability) could force the Fed to slow its easing pace.

3. Global Growth Concerns: A slowdown in China's manufacturing sector (as seen in May's PMI data) might spill into U.S. markets, complicating Fed decisions.

Investment Recommendation: Balance Aggression with Prudence

For Income-Oriented Investors:

- Allocate 20% of fixed-income portfolios to 10-year Treasury futures, targeting a 4.35% entry point. Use stop-loss orders at 4.45% to limit downside.

For Speculative Traders:

- Deploy 5–10% of capital into August 10-year call options (113.00 strike). Pair with SOFR put options (95.625 strike) to mitigate rate-hike risks.

For Hedgers:

- Use SOFR-linked inverse floaters or interest rate collars to insulate portfolios against Fed policy whiplash.

Conclusion: The Fed's Tightrope and the Bond Market's Gamble

Traders are betting that the Fed will prioritize growth over inflation, driving yields to 4%. Yet markets must navigate a minefield of fiscal, geopolitical, and economic risks. The path to 4% is not guaranteed—but for investors willing to layer in hedges and duration exposure, the reward-to-risk calculus tilts favorable. As always, the Fed's next move will decide whether this rally becomes a reality or a fleeting mirage.

Stay vigilant, stay hedged, and let the yield curve do the talking.

Comentarios

Aún no hay comentarios