BNDI and the Tax Implications of Its Distributions: A Deep Dive for Income Investors

For income-focused investors, the (BNDI) has emerged as a compelling option, blending core fixed-income exposure with a data-driven options overlay. But here's the catch: its distribution structure and tax treatment are far from ordinary. Understanding how BNDI's returns are classified—and how they interact with the IRS's arcane rules—can mean the difference between a tax-efficient windfall and an unwelcome surprise come April 15.

The BNDI Blueprint: Return of Capital and Section 1256 Contracts

BNDI's strategy hinges on two pillars: a representative slice of the U.S. Aggregate Bond Market and a systematic sale of SPX Index put options[1]. These options, classified as , , 40% short-term capital gains), regardless of holding period[2]. This is a stark contrast to traditional fixed-income funds, where distributions are often taxed as ordinary income.

But the real twist lies in BNDI's distributions. According to its prospectus, . While this reduces investors' taxable income in the year received, it also erodes their cost basis. For example, , . If you later sell the shares for $12,000, , amplifying your tax liability[3].

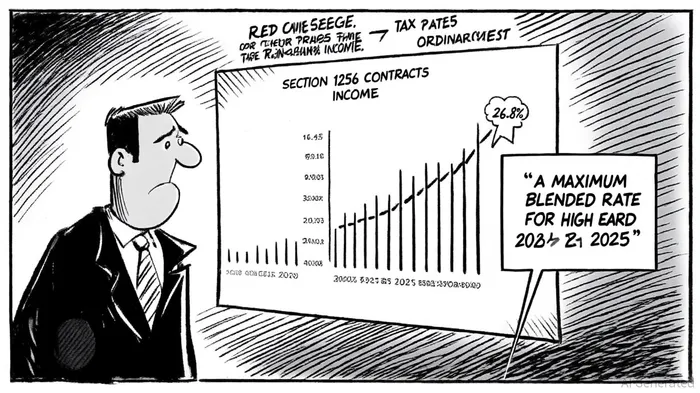

The Double-Edged Sword of Section 1256 Contracts

The SPX options sold by BNDI fall under , which mandates mark-to-market accounting at year-end. This means gains or losses are recognized even if the contracts aren't closed[2]. For 2025, this rule remains unchanged, , .

This structure provides two key advantages:

1. Tax Loss Harvesting Flexibility: If BNDI's options strategy incurs losses, , potentially securing refunds[4].

2. Predictability: The 60/40 split simplifies tax planning compared to the variable rates of ordinary income or traditional capital gains.

However, the complexity arises when distributions are misclassified. If a return of capital is erroneously reported as ordinary income, investors may overpay taxes. For small amounts, the IRS might overlook the error, . Tools like taxr.ai can help parse these nuances, ensuring accurate reporting[3].

Investor Takeaways: Balancing Risk and Reward

BNDI's tax-efficient design appeals to investors seeking income while minimizing drag from taxes. Yet, its success depends on two critical factors:

- Market Volatility: The SPX options strategy thrives in stable markets but could face pressure during sharp downturns, affecting both returns and tax outcomes[1].

- : Recent IRS rulings, such as designating the Bourse de Montreal as a qualified exchange, expand Section 1256 eligibility[1]. Future changes could alter the tax landscape for such strategies.

The Bottom Line

BNDI's blend of bond exposure and options-driven income is innovative, but its tax implications demand scrutiny. For investors, the key is to treat BNDI not just as a yield play but as a strategic tool in a broader tax-aware portfolio. As always, consult a tax professional to navigate the intricacies of return of capital and Section 1256 contracts—because in the game of taxes, even small miscalculations can cost big.

Comentarios

Aún no hay comentarios