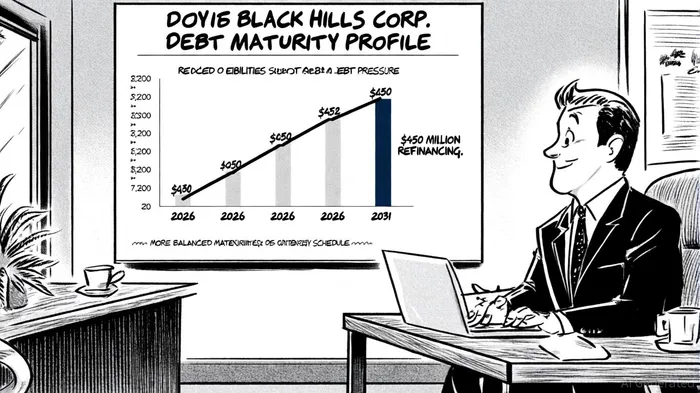

Black Hills' $450 Million Public Debt Offering: Strategic and Financial Implications for Long-Term Investors

Black Hills Corp.'s recent $450 million public debt offering represents a pivotal strategic move to optimize its capital structure and align with long-term growth objectives in the utilities sector. The offering, priced at 4.550% senior unsecured notes due January 31, 2031, is set to close on October 2, 2025, and will directly retire $300 million of its 3.950% notes maturing in January 2026, with remaining proceeds allocated to general corporate purposes [1]. This refinancing initiative underscores the company's proactive approach to managing debt maturities and reducing short-term liquidity risks, a critical consideration for investors evaluating its financial resilience.

Strategic Rationale: Extending Maturity and Cost Stability

The decision to refinance short-term debt with longer-term capital reflects a disciplined strategy to mitigate refinancing volatility. By replacing 2026 obligations with 2031 liabilities, Black HillsBKH-- extends its debt horizon, providing greater flexibility to navigate potential interest rate fluctuations. While the coupon rate of 4.550% is higher than the retired 3.950% notes, the extended maturity reduces immediate cash flow pressures and aligns with the company's focus on long-term infrastructure investments. For instance, the proceeds will support ongoing projects such as the 260-mile Ready Wyoming transmission expansion, which is expected to stabilize costs for customers and enable future growth [2].

Financial Implications: Credit Metrics and Leverage

Black Hills' debt-to-equity ratio, a key metric for assessing leverage, has shown gradual improvement. As of June 30, 2025, the ratio stood at 1.71, down from 1.80 in 2024, indicating progress toward its long-term capitalization targets [3]. This trend aligns with S&P Global Ratings' affirmation of the company's 'BBB+' long-term credit rating, which reflects confidence in its operational performance and financial stability [4]. However, Fitch Ratings' recent withdrawal of its 'BBB+' rating—despite an initial affirmation—introduces a layer of caution, as it highlights the need for continued monitoring of leverage trends and cash flow generation [5].

The company's capital structure remains balanced, with regional subsidiaries like Nebraska Gas and Kansas Gas targeting equity-debt splits of approximately 50:50. These structures, coupled with rate case approvals seeking incremental revenues (e.g., $35 million annually in Nebraska), provide a robust foundation for financing growth while maintaining acceptable risk levels [6].

Growth and Earnings Outlook: A Foundation for Long-Term Value

Black Hills has reaffirmed its 2025 earnings guidance of $4.00 to $4.20 per share, with a 4-6% EPS growth rate outlook, driven by regulatory approvals and infrastructure projects [7]. The transmission expansion in Wyoming, now in its final phase, exemplifies the company's commitment to long-term value creation. Additionally, investments in renewable energy and data center demand position Black Hills to capitalize on decarbonization trends and technological advancements, which are critical for sustained profitability in the evolving utilities sector [8].

Risks and Considerations for Investors

While the refinancing strengthens Black Hills' liquidity profile, investors must weigh the company's elevated leverage against its growth prospects. A debt-to-equity ratio of 1.71 remains above industry averages, necessitating consistent cash flow generation to service obligations. Furthermore, regulatory risks—such as delays in rate case approvals or cost overruns for infrastructure projects—could impact margins. However, the company's proactive capital structure management and alignment with long-term regulatory frameworks suggest a measured approach to risk mitigation.

Conclusion: A Strategic Move with Long-Term Potential

Black Hills' $450 million debt offering is a calculated step to enhance financial flexibility while funding strategic growth initiatives. For long-term investors, the transaction underscores the company's ability to balance debt management with infrastructure investment—a critical dual focus in the utilities sector. With a stable credit rating, improving leverage metrics, and a clear roadmap for earnings growth, Black Hills appears well-positioned to navigate macroeconomic uncertainties and deliver value over the next decade.

Comentarios

Aún no hay comentarios