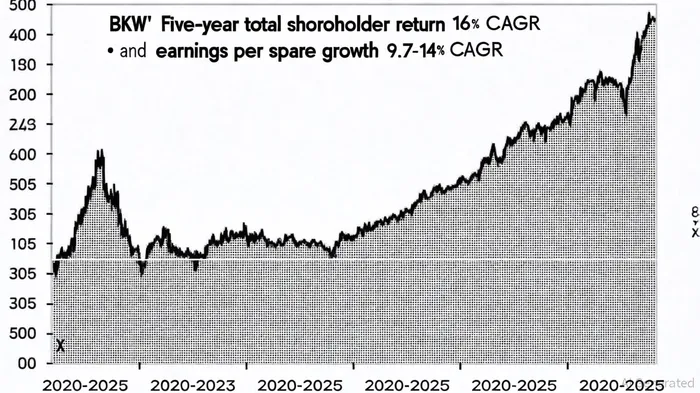

BKW's Earnings vs. Shareholder Return Divergence: Assessing the Sustainability of a 16% CAGR

The divergence between BKW AG (VTX:BKW)'s earnings growth and shareholder returns has become a focal point for investors seeking to assess the sustainability of its reported 16% compound annual growth rate (CAGR) in total shareholder returns (TSR). While the stock has delivered robust returns-driven largely by dividends and market optimism-its underlying earnings trajectory has shown signs of strain, raising critical questions about the alignment between financial performance and investor expectations.

Earnings Growth vs. TSR: A Tale of Two Metrics

According to a Simply Wall St report, BKW's five-year TSR has averaged 16%, outpacing its earnings per share (EPS) growth of 9.7–14%. This gap suggests that the market has priced in expectations of future growth, particularly through dividends and share price appreciation, rather than current earnings momentum. For instance, between 2020 and mid-2025, BKW's dividend payouts accounted for a significant portion of its TSR, with a payout ratio projected to rise to 43% in the coming years, according to MarketScreener. However, this optimism faces a reality check in 2025, as the company's first-half results revealed a sharp decline in EPS to CHF3.54 from CHF6.62 in the prior-year period, alongside a 4.2% revenue drop and a halved profit margin (BKW's half-year report).

The disconnect between TSR and earnings is further underscored by BKW's recent performance. Despite a 140–141% five-year TSR, the company's EBIT for 1H 2025 fell by 29.1% year-on-year to CHF310.7 million, driven by lower electricity prices and reduced hydro and wind generation in its Energy Solutions segment (BKW's half-year report). This highlights a key risk: the sustainability of high returns may depend on external factors, such as seasonal demand fluctuations and renewable energy output, rather than consistent operational improvements.

Strategic Investments and Analyst Projections: A Path to Reconciliation?

BKW's management has pointed to strategic investments in Energy Solutions and Infrastructure & Buildings as catalysts for future growth. The Infrastructure & Buildings segment, for example, saw a 26% EBIT increase in 1H 2025, driven by higher efficiency and demand for complex infrastructure projects (BKW's half-year report). Simply Wall St analysts note that BKW's focus on renewable energy-particularly wind, solar, and battery storage-positions it to benefit from long-term industry trends. However, these initiatives require time to materialize, and their impact on near-term earnings remains uncertain.

Dividend projections offer some reassurance. BKW's DPS is forecasted to rise from CHF3.7 in 2025 to CHF4.025 by 2027, with a stable yield of 2.21% (MarketScreener). This disciplined approach to shareholder returns, combined with a confirmed 2025 EBIT guidance of CHF650–750 million, suggests the company is balancing reinvestment and payouts (BKW's half-year report). Yet, with earnings growth projected at 7.6% annually-well below the historical 16% TSR CAGR-the question persists: Can BKW sustain its returns without stronger earnings momentum?

Risks and Realities: The CAGR Conundrum

The sustainability of BKW's 16% CAGR hinges on several factors. First, the company's reliance on seasonal effects in Energy Solutions and Infrastructure & Buildings introduces volatility. For example, while BKW expects stronger 2H 2025 results, this may not offset the first-half downturn, particularly if energy prices remain depressed. Second, the broader European utilities sector faces headwinds, including regulatory pressures and capital expenditure demands, which could constrain margins. An analysis on Yahoo Finance highlights that BKW's return on equity (ROE) of 8.7% is in line with industry averages but lacks differentiation.

Moreover, valuation metrics suggest caution. BKW's current P/E ratio of 18.7x is moderate, but its projected earnings growth of 7.1% annually-well below the market's 11%-raises concerns about whether the stock's intrinsic value of CHF256 (per a two-stage DCF model) is achievable. While the share price of CHF176 implies a 31% undervaluation, this assumes a recovery in earnings and stable demand for dividends-a scenario that remains unproven.

Conclusion: A Cautious Outlook

BKW's 16% CAGR in TSR reflects a blend of dividend discipline and market optimism, but its earnings trajectory casts doubt on the sustainability of this performance. The company's strategic investments and resilient Infrastructure & Buildings segment offer hope, yet near-term challenges-including earnings declines and sector-wide pressures-underscore the need for tempered expectations. For investors, the key takeaway is clear: while BKW's shareholder returns may persist in the short term, aligning them with earnings growth will require navigating operational headwinds and capitalizing on long-term energy transition opportunities.

Comentarios

Aún no hay comentarios