Bitcoin's Institutional Ascendancy: Regulatory Shifts and the Future of Retirement Portfolios

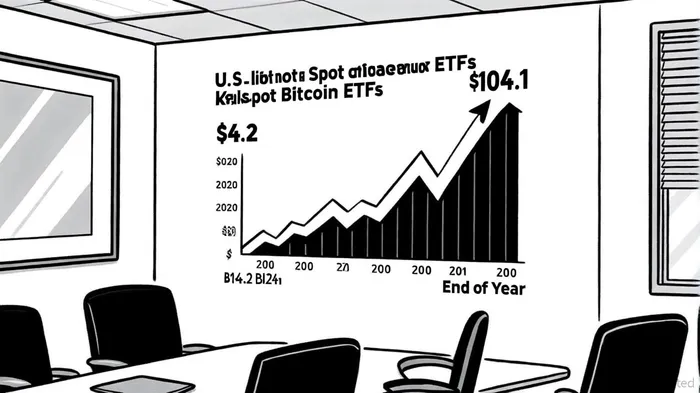

The U.S. Securities and Exchange Commission (SEC) approved the launch of spot BitcoinBTC-- ETFs in early 2024, providing a compliance-friendly vehicle for institutional investors to allocate capital into Bitcoin[1]. This regulatory breakthrough marked a pivotal shift, transforming Bitcoin from a speculative asset into a legitimate component of institutional investment strategies. By the end of 2024, U.S.-listed spot Bitcoin ETFs held $104.1 billion in assets, with $27.4 billion coming from institutions managing over $100 million in assets[1]. This influx of capital has unlocked the potential for a $3 trillion institutional capital influx into the crypto market[1], signaling a structural reorientation in how Bitcoin is perceived and utilized.

Regulatory Clarity: The Catalyst for Institutional Adoption

The regulatory landscape for cryptocurrencies has evolved dramatically in 2024–2025, with key developments enabling Bitcoin's integration into retirement vehicles. The Department of Labor (DOL) rescinded its 2022 guidance discouraging cryptocurrency investments in retirement plans, adopting a neutral stance under Compliance Assistance Release No. 2025-01[3]. This shift allows ERISA fiduciaries to evaluate cryptocurrencies on a case-by-case basis, considering their prudence and alignment with portfolio goals[3]. Simultaneously, the Internal Revenue Service (IRS) issued final regulations requiring custodial brokers to report digital asset transactions on Form 1099-DA, improving tax compliance while providing transitional relief for complex activities like staking[4].

President Donald Trump's August 2024 executive order further accelerated adoption by encouraging the inclusion of alternative investments, including Bitcoin, in retirement plans. The order mandated regulatory coordination among the SEC, DOL, and Treasury to streamline compliance[5]. These developments have created a permissive environment for institutional players to allocate Bitcoin within 401(k)s and IRAs, with major asset managers like Fidelity and BlackRockBLK-- already introducing Bitcoin ETF options in retirement plans[2].

Institutional Case Studies: From Experimentation to Mainstream

The institutional adoption of Bitcoin in retirement vehicles is no longer theoretical. For instance, the State of Michigan Retirement System invested $6.6 million in the ARK 21Shares Bitcoin ETF, while the Houston Firefighters' Relief and Retirement Fund holds approximately $99 million in Bitcoin and ether[2]. These examples underscore a growing trend of pension funds diversifying into digital assets, with 94% of state and government pension plan sponsors now considering or already investing in cryptocurrencies[2].

BlackRock's iShares Bitcoin Trust ETF, which attracted over $50 billion in assets, exemplifies the scale of institutional demand[2]. Meanwhile, Fidelity's integration of Bitcoin ETFs into select 401(k) plans highlights how traditional financial infrastructure is adapting to accommodate crypto. These moves are not merely about chasing returns but about redefining Bitcoin's role as a hedge against inflation and a store of value in an era of macroeconomic uncertainty.

Implications for Long-Term Portfolio Strategy

The inclusion of Bitcoin in retirement portfolios reflects a broader rethinking of asset allocation. Institutional investors are increasingly viewing Bitcoin as a non-correlated asset that can enhance diversification and mitigate risks in traditional equity and bond-heavy portfolios. However, this shift is not without challenges. ERISA fiduciaries must navigate custodial complexities, regulatory uncertainties, and Bitcoin's inherent volatility[6].

The institutional adoption of Bitcoin is expected to follow an S-curve, with rapid acceleration in the next few years as more pension funds and asset managers allocate a portion of their portfolios to Bitcoin ETFs[1]. This transition will likely reshape the crypto market's dynamics, reducing volatility and increasing liquidity. For individual investors, the normalization of Bitcoin in retirement accounts could democratize access to an asset class once reserved for speculative traders.

The Road Ahead: Structural Changes and Risks

While regulatory clarity has been a game-changer, the journey is far from complete. The IRS's delayed reporting rules for staking and lending activities[4] and the DOL's permissive but non-prescriptive stance[3] highlight the need for ongoing regulatory coordination. Additionally, the risks associated with custodial security and market volatility remain significant[6].

Nevertheless, the trajectory is clear: Bitcoin is no longer a fringe asset. Its inclusion in institutional retirement vehicles signals a maturation of the crypto market and a recognition of its potential to serve as a long-term store of value. As the S-curve of adoption accelerates, the next few years will likely see Bitcoin cement its place alongside gold and real estate as a cornerstone of diversified institutional portfolios.

Comentarios

Aún no hay comentarios