Bitcoin Futures Funding Rates Near Neutral: A Signal for Strategic Positioning and Arbitrage Opportunities

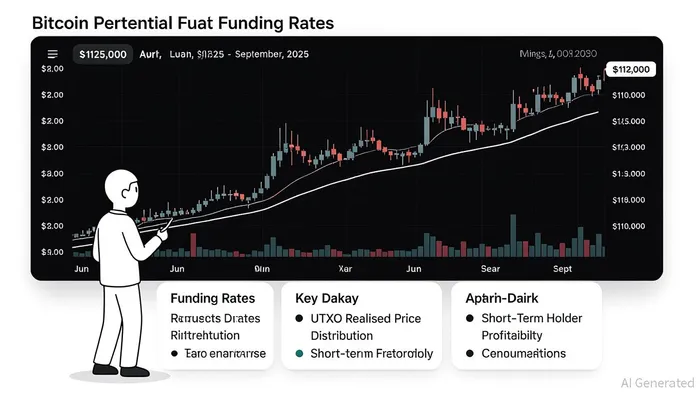

Bitcoin’s perpetual futures funding rates have entered a neutral phase in Q3 2025, presenting a unique inflection pointIPCX-- for traders and institutional investors. As of September 4, the daily funding rate stands at 1.73%, with a 7-day average of 1.21% and a 30-day average of 0.96% [3]. These figures, while positive, signal a moderation in speculative fervor compared to the hyper-bullish extremes seen earlier in the year. This neutrality—where longs pay shorts at a steady but non-excessive rate—creates fertile ground for delta-neutral strategies and arbitrage opportunities, allowing market participants to capitalize on funding rate differentials without directional price bets.

The Mechanics of Delta-Neutral Positioning

Delta-neutral trading, which balances long and short positions to eliminate directional exposure, has become a cornerstone of risk-adjusted returns in crypto derivatives. For example, a trader might buy BitcoinBTC-- spot on Binance while shorting a perpetual futures contract on Bybit, locking in funding rate payments while remaining insulated from price volatility [1]. This strategy thrives in neutral funding rate environments, where the cost of carry for longs remains predictable.

A backtested 3x leveraged delta-neutral approach, combining spot and perpetual futures, has demonstrated an annualized return of 16.0% and a Sharpe ratio of 6.1 over three years [5]. The key to success lies in dynamic rebalancing and systematic reinvestment of funding inflows. For instance, during Q3 2025, traders exploiting cross-exchange funding rate disparities—such as shorting on BitMEX (higher rates) while longing on Hyperliquid (lower rates)—have generated consistent yields without price exposure [2].

Arbitrage Opportunities in a Neutral Regime

Neutral funding rates also amplify arbitrage potential. Cash-and-carry strategies, where spot assets are bought and futures are shorted to capture basis differentials, have proven effective. For example, if Bitcoin spot trades at $108,000 on Binance and quarterly futures on Bybit are priced at $108,300, a trader can lock in a $300 premium at expiry while maintaining a delta-neutral stance [1].

Funding rate farming—holding spot longs and perpetual shorts to collect periodic payments—has similarly flourished. During Q2 2025, teams employing this tactic achieved 115.9% returns over six months, with losses capped at 1.92% [2]. The strategy’s low correlation with traditional HODLing makes it an attractive diversifier for institutional portfolios [2].

Risk-Adjusted Returns and Institutional Frameworks

Institutional investors are increasingly integrating Bitcoin into portfolios to enhance risk-adjusted returns. A 1% allocation to Bitcoin has been shown to improve Sharpe and Sortino ratios significantly, particularly when paired with delta-neutral strategies [1]. Advanced frameworks like the Mixture of Distributions Hypothesis (MDH) and Value-at-Risk (VaR) models are now standard tools for managing volatility and correlation risks [4].

For example, the Galaxy report highlights that reallocating from equities to Bitcoin reduces portfolio volatility while boosting risk-return profiles [1]. Meanwhile, options-based strategies—such as volatility selling and covered calls—are being layered into arbitrage frameworks to generate income from premiums [5].

Strategic Positioning for Q4 2025

With Bitcoin consolidating near $112,000 and the Federal Reserve’s September 17 meeting looming, traders must balance caution with opportunity. Neutral funding rates suggest a market in equilibrium, but fragile short-term holder profitability (dropping to 42% during selloffs) underscores the need for disciplined risk management [2].

Key actions for Q4:

1. Delta-Neutral Portfolios: Prioritize cross-exchange arbitrage and funding rate farming to exploit stable differentials.

2. Options Hedging: Use out-of-the-money (OTM) puts to protect against volatility spikes ahead of the Fed meeting [5].

3. Capital Efficiency: Leverage AI-driven execution tools to minimize slippage and optimize rebalancing [1].

Source:

[1] The Impact and Opportunity of Bitcoin in a Portfolio [https://www.galaxy.com/insights/research/bitcoin-in-a-portfolio-impact-and-opportunity-2025]

[2] Strategy Index III 2025 Q2 [https://blog.1token.tech/strategy-index-iii-2025-q2/]

[3] Something unusual is building in $9.81 billion of Bitcoin futures flows and it could break either way [https://cryptorank.io/news/feed/aeb68-something-unusual-is-building-in-9-81-billion-of-bitcoin-futures-flows-and-it-could-break-either-way]

[4] High-frequency dynamics of Bitcoin futures [https://www.sciencedirect.com/science/article/pii/S2214845025001188]

[5] A Delta-Neutral Long-Spot/Short-Future Strategy [https://papers.ssrn.com/sol3/Delivery.cfm/5292305.pdf?abstractid=5292305&mirid=1]

Comentarios

Aún no hay comentarios