Biomea Fusion's Icovamenib: A Dual Catalyst of Therapeutic Innovation and Market Rebound?

Biomea Fusion (NASDAQ:BMEA) has emerged as a focal point in the diabetes therapeutics landscape following the release of 52-week results from its Phase II COVALENT-111 trial of icovamenib, a covalent menin inhibitor targeting pancreatic beta-cell dysfunction. The data, which demonstrated sustained glycemic control and a favorable safety profile, has reignited investor optimism, even as the stock remains in a multi-year slump. This article examines the clinical and market implications of these results, assessing whether icovamenib's therapeutic potential can catalyze a meaningful rebound for the company.

Therapeutic Potential: A Disease-Modifying Paradigm

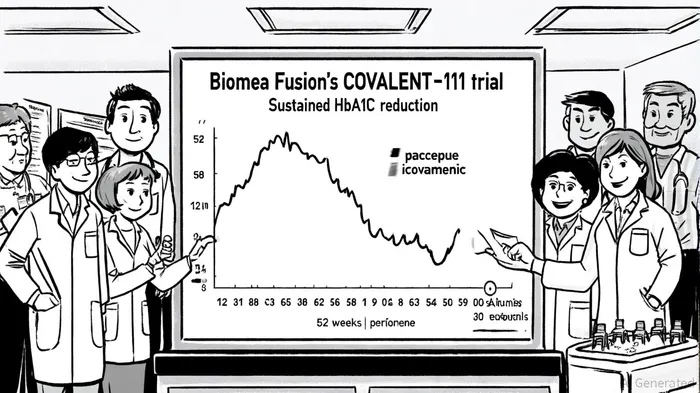

According to the Biomea Fusion press release, icovamenib achieved a 1.8% placebo-adjusted mean reduction in HbA1c in patients with severe insulin deficiency and those on GLP-1-based therapies, with durable effects observed as early as 12 weeks post-treatment. Notably, the drug's mechanism-restoring beta-cell mass and function-positions it as a potential disease-modifying therapy, a rare attribute in the type 2 diabetes (T2D) market, as highlighted in a Clarivate report.

The COVALENT-111 trial also highlighted icovamenib's ability to increase C-peptide levels, a biomarker of endogenous insulin production, suggesting long-term metabolic benefits. This differentiates it from existing therapies, which primarily focus on glycemic control without addressing the underlying pathophysiology of insulin deficiency. Analysts at Clarivate note that the T2D market remains underserved by disease-altering treatments, creating a significant unmet need.

Market Momentum: Analyst Optimism vs. Stock Volatility

Despite a 68% year-to-date decline in Biomea Fusion's stock price, MarketBeat reported that the trial results have spurred a wave of positive analyst ratings. Jefferies initiated coverage with a Buy rating and a $5.00 price target, citing the drug's potential to disrupt the T2D market. Piper Sandler and H.C. Wainwright followed suit, raising their price targets to $19.00 and $40.00, respectively. EF Hutton's $128.00 target, while ambitious, underscores the high expectations for icovamenib's commercial potential.

The stock's current valuation at $2.67-well below the average 12-month target of $14.80-reflects lingering skepticism. However, institutional ownership remains robust at 96.72%, indicating confidence in the company's long-term prospects. The upcoming Phase IIb trials, expected to begin in Q4 2025, could serve as a critical inflection point, providing further validation of icovamenib's efficacy in specific patient subtypes.

Competitive Landscape: Complementing GLP-1 Therapies

Icovamenib's ability to enhance the effectiveness of GLP-1 agonists like semaglutide and tirzepatide adds another layer of strategic value. Clinical data suggests that the drug increases GLP-1 receptor expression and intracellular insulin, potentially allowing for lower doses of these agents and improving tolerability. In a market where polypharmacy is increasingly common, icovamenib could act as a foundational therapy, addressing the root cause of insulin deficiency while complementing existing treatments.

Investment Thesis: Balancing Risk and Reward

While the clinical data is compelling, Biomea FusionBMEA-- faces significant hurdles. The stock's volatility and the high bar set by analysts' price targets highlight the risks inherent in late-stage development. However, the drug's novel mechanism, positive safety profile, and potential to redefine T2D treatment create a strong foundation for long-term growth.

For investors, the key catalysts will be the outcomes of Phase IIb trials and regulatory milestones. If icovamenib demonstrates consistent efficacy in larger trials, Biomea Fusion could attract partnerships or acquisition interest, further accelerating its path to commercialization.

Comentarios

Aún no hay comentarios