BioCardia's (BCDA) Q2 2025 Earnings and Strategic Pivots in Cardiac Regeneration: A Deep Dive into Long-Term Investment Potential

In the rapidly evolving landscape of regenerative medicine, BioCardiaBCDA-- (BCDA) has positioned itself as a pivotal player with a unique blend of technological innovation, strategic partnerships, and regulatory momentum. The company's Q2 2025 earnings report and business updates reveal a firm navigating the challenges of capital efficiency while advancing a pipeline with transformative potential in cardiac cell therapy. For investors, the question is not just whether BioCardia can survive its current financial constraints but whether it can leverage its innovations to dominate a market projected to grow at a 16.83% CAGR through 2030.

Financial Constraints and Strategic Prioritization

BioCardia's Q2 2025 net loss of $2 million, up from $1.6 million in Q2 2024, reflects a deliberate shift in resource allocation. R&D expenses surged to $1.4 million, a 75% increase year-over-year, underscoring the company's commitment to advancing its CardiAmp Heart Failure II trial and the HelixHLXB-- Biotherapeutic Delivery System. While cash reserves stood at $1.1 million as of June 2025, the company raised an additional $769,000 via its ATM facility, extending its runway to October 2025. CEO Peter Altman's emphasis on a $6 million annual burn rate highlights the need for disciplined capital management—a critical factor in a sector where clinical milestones often dictate valuation.

Historically, BCDA's stock has shown mixed performance around earnings releases, with the latest event in August 2025 resulting in a 6.15% decline.

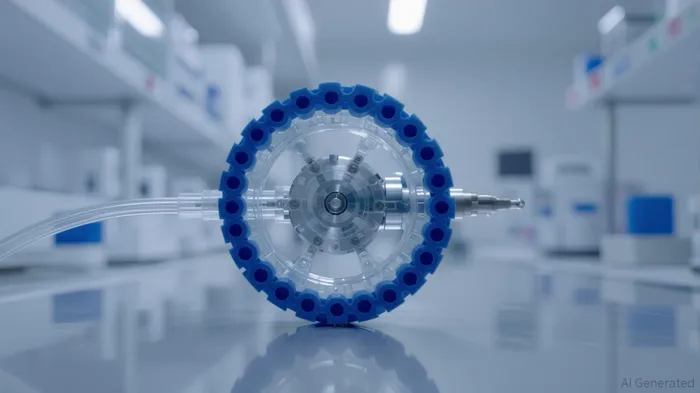

Innovation Momentum: Helix and CardiAmp as Dual Engines

BioCardia's core differentiator lies in its proprietary Helix Biotherapeutic Delivery System, a platform designed to deliver cell and gene therapies with unprecedented precision. The system's morphDNA steerable introducer technology prevents whip-in during procedures, a critical advantage in ventricular ablation and other high-risk cardiac interventions. Clinical data from the CardiAmp Heart Failure trial—showing a 30% improvement in cell delivery efficiency—has already positioned Helix as a potential first-in-class transcatheter delivery system in the U.S.

The Helix system is not just a standalone product but a strategic enabler for BioCardia's broader pipeline. By offering a scalable, cost-effective delivery mechanism, the company is attracting partnerships with cell and gene therapy firms seeking to reduce operational costs and accelerate clinical timelines. This “platform-as-a-service” model could unlock recurring revenue streams, particularly as the global regenerative medicine market expands.

Strategic Partnerships and Market Positioning

BioCardia's focus on Japan and the electrophysiology (EP) market represents a shrewd alignment with unmet needs and cultural preferences. Japan's PMDA has shown a favorable regulatory environment for autologous therapies, and BioCardia's prior approval for orthopedic applications (via its point-of-care cell processing platform) provides a credibility boost. The company's plans for a PMDA meeting in Q4 2025 and an FDA submission for Helix in Q3 2025 are critical inflection points.

In the $10 billion EP market, BioCardia's morphDNA technology is being positioned as a solution for both atrial and ventricular tachyarrhythmias. The ability to integrate Helix into existing EP workflows could attract partnerships with major medical device firms, creating a bridge between BioCardia's niche expertise and broader market demand.

Competitive Landscape and Long-Term Potential

While competitors like BlueRock Therapeutics and Frequency Therapeutics are advancing iPSC-based and PCA platforms, BioCardia's strength lies in its dual focus on delivery systems and cost-effective cell manufacturing. The company's CardiAllo allogeneic cell therapy, with a lower cost profile than peers, could disrupt the market for off-the-shelf therapies. Additionally, BioCardia's ability to manufacture clinical-grade cells at scale—combined with its regulatory expertise—positions it to attract non-dilutive funding and strategic collaborations.

Investment Thesis: Balancing Risk and Reward

For long-term investors, BioCardia's Q2 2025 results present a compelling case. The company's regulatory milestones in the U.S. and Japan, coupled with its strategic partnerships, could catalyze a valuation re-rating if key trials succeed. However, the path is not without risks: cash burn, reliance on partnerships, and the high bar for FDA approval in regenerative medicine remain significant hurdles.

A prudent approach would involve monitoring BioCardia's September 2025 financing round and the outcomes of its PMDA and FDA submissions. Success in these areas could unlock partnerships, non-dilutive funding, and commercialization pathways in Japan—a market where cultural and regulatory alignment with autologous therapies could drive rapid adoption.

Conclusion

BioCardia's Q2 2025 earnings underscore a company at a pivotal juncture. While its financials remain lean, its technological innovations and strategic pivots position it to capitalize on the explosive growth of the regenerative medicine sector. For investors willing to navigate the risks of a high-stakes clinical and regulatory environment, BioCardia represents a unique opportunity to participate in the next wave of cardiac regeneration. The coming months will be critical, but if the company can execute on its roadmap, the rewards could be substantial."""

Comentarios

Aún no hay comentarios