Berry Corporation's Merger with CRC: A Strategic and Financial Deep Dive for Investors

The recent 14.2% premarket surge in BerryBRY-- Corporation (BRY) shares following the announcement of its $717 million all-stock merger with California Resources CorporationCRC-- (CRC) has sparked significant investor interest[2]. This deal, which values the combined entity at over $6 billion, is not merely a transaction but a strategic recalibration of California's energy landscape. For investors, the question is no longer whether the merger will happen—regulatory and shareholder approvals are expected by Q1 2026[1]—but whether this consolidation represents a compelling long-term opportunity.

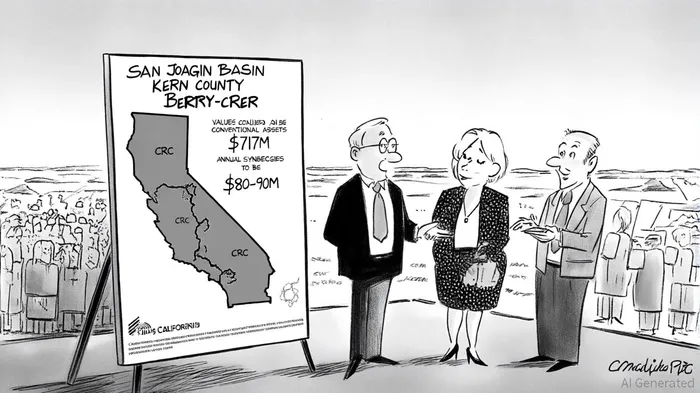

Strategic Rationale: Synergy Through Complementarity

The merger's strategic logic lies in geographic and operational alignment. CRCCRC--, a conventional oil and gas producer, gains access to Berry's high-quality, oil-weighted reserves in California's San Joaquin Basin and Kern County, areas critical to the state's energy security[5]. Conversely, Berry's Uinta Basin assets in Utah, while peripheral to CRC's California focus, offer monetization potential, adding flexibility to the combined company's capital structure[4]. This complementarity mirrors broader industry trends, where consolidation is driven by the need to streamline operations and reduce costs in a regulatory environment increasingly favorable to domestic energy production[3].

The deal also aligns with California's evolving policy landscape. Legislation like SB237, which streamlines permitting for new drilling, enhances the value of the merged entity's asset base[5]. CRC President Francisco Leon emphasized that the merger would create “a more efficient energy leader,” leveraging Berry's C&J Well Services subsidiary to improve well maintenance and abandonment capabilities[1]. Such operational synergiesTAOX-- are critical in an industry where cost per barrel of oil equivalent (BOE) has risen despite falling commodity prices[1].

Financial Implications: Accretion and Balance Sheet Strength

Financially, the merger is poised to deliver immediate value. CRC anticipates $80–90 million in annual cost synergies within 12 months post-closure, primarily from corporate efficiencies, supply chain optimizations, and debt refinancing[2]. These savings represent approximately 12% of the transaction value, a robust return for investors. The combined entity's pro forma leverage ratio is projected to remain below 1.0x, supported by 70% of its second-half 2025 oil production being hedged at a $68/Bbl Brent floor price[1]. This financial discipline positions the company to pursue new development opportunities without overleveraging.

Moreover, the all-stock structureGPCR-- ensures Berry shareholders receive 0.0718 shares of CRC stock per BRY share, a 15% premium based on September 12, 2025, closing prices[2]. This premium, coupled with the projected 10% per-share accretion to free cash flow in late 2025, suggests the merger is designed to reward both sets of shareholders[3].

Industry Trends: Consolidation as a Survival Strategy

The Berry-CRC merger is emblematic of a larger wave of consolidation in the U.S. oil and gas sector. From 2023 to 2024, M&A activity surged to $440 billion, with megadeals like ExxonMobil's $64.5 billion acquisition of Pioneer Natural Resources reshaping the competitive landscape[1]. These transactions are driven by the need to achieve economies of scale, secure unproved properties for future drilling, and navigate regulatory complexities[2].

However, consolidation is not without challenges. Post-merger integration has led to rising BOE costs, even as companies seek to realize synergies[1]. For example, Chevron's proposed $60 billion acquisition of Hess Corporation aims to expand production in Guyana but faces integration hurdles[2]. The Berry-CRC deal, however, appears better positioned to avoid such pitfalls, given its focus on complementary assets and a clear synergy roadmap.

Analyst Perspectives: Caution Amid Optimism

Despite the merger's strategic and financial merits, analyst sentiment remains cautiously neutral. As of September 2025, two Wall Street analysts have assigned a “Hold” rating to BRY, with an average 12-month price target of $4.00—slightly below the current $4.08 stock price[3]. This suggests skepticism about near-term upside, possibly due to integration risks or broader market volatility. However, the projected $80–90 million in annual synergies and the combined entity's strong balance sheet could justify a reevaluation of BRY's valuation over time[4].

Conclusion: A Reassessment for Long-Term Investors

For investors, the Berry-CRC merger represents a calculated bet on California's energy future. While short-term analyst caution is understandable, the deal's strategic alignment with industry trends, financial accretion, and regulatory tailwinds suggest a compelling long-term case. The key risks—integration challenges and regulatory delays—are mitigated by the transaction's all-stock structure and CRC's proven operational expertise. In a sector where consolidation is the new normal, this merger could serve as a blueprint for value creation. Investors who reassess their positions in BRY may find themselves well-positioned to capitalize on the next phase of the energy transition.

Comentarios

Aún no hay comentarios