BeiGene's Oncology Ascendancy: TEVIMBRA's Regulatory Momentum Fuels Global Growth Surge

The European Medicines Agency's recent positive opinion for BeiGene's TEVIMBRA (tislelizumab) in first-line recurrent or metastatic nasopharyngeal cancer (NPC) marks a pivotal moment for the biotech's oncology dominance. With robust clinical data showing a 48% reduction in disease progression or death risk (HR 0.52) and a median overall survival (OS) of 45.3 months versus 31.8 months for placebo plus chemo, TEVIMBRA is poised to transform treatment paradigms—and investor returns. This milestone, alongside its expanding approvals in esophageal squamous cell carcinoma (ESCC), underscores BeiGene's strategic precision in targeting high-growth, underserved markets. Here's why investors must act now.

Clinical Superiority: TEVIMBRA's Data-Driven Edge

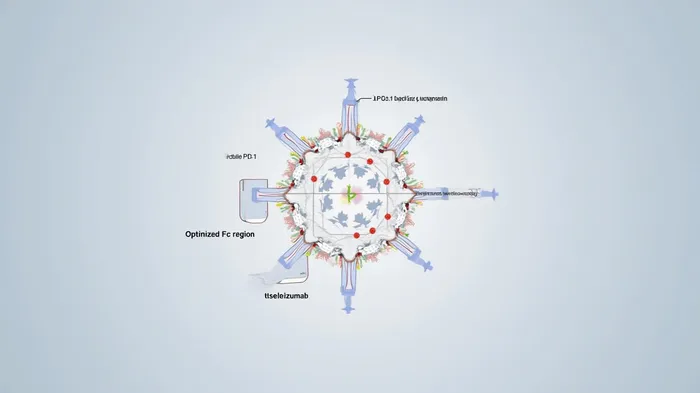

TEVIMBRA's RATIONALE-309 trial for NPC delivers unmatched efficacy, with a median PFS of 9.2 months versus 7.4 months for chemotherapy alone. This translates to a 35% lower risk of progression or death (HR 0.52; p<0.0001), outperforming competing PD-1 inhibitors like Keytruda and Opdivo in similar indications. The drug's design—minimizing Fcγ receptor binding to enhance anti-tumor activity—gives it a structural advantage, while its safety profile aligns with expectations for PD-1 therapies.

In ESCC, the RATIONALE-306 trial showed an 18% reduction in mortality risk (HR 0.66) in PD-L1-positive patients, with median OS of 16.8 months versus 9.6 months for placebo. These results have already secured EU and U.S. approvals, positioning TEVIMBRA as the first-line standard of care for this lethal cancer.

Geographic Reach: Tapping into Asia's Cancer Burden

The NPC and ESCC markets are concentrated in Asia-Pacific, where 81% of NPC and over 50% of ESCC cases occur. With NPC's 5-year survival dropping to 49% in advanced stages and ESCC's median OS at 10.6 months without immunotherapy, the region's unmet need is stark.

BeiGene's dual focus on China and Europe leverages this:

- China: Already the world's largest NPC market, with 30 cases/100,000 in high-incidence areas.

- EU: A regulatory gateway to 450 million patients, with NPC incidence rising in regions like France and Spain.

The company's rebranding to BeOne Medicines Ltd. reinforces its mission to expand access globally, supported by partnerships like its $650M deal with Novartis for U.S./EU commercialization.

Market Growth: CAGR Opportunities in Underserved Oncology

The NPC and ESCC markets offer sustainable growth:

- NPC Market: Expected to grow at a 2.7% CAGR (2025–2030), driven by rising awareness, early screening, and combination therapies.

- ESCC Market: A 8.16% CAGR (2025–2030), fueled by immunotherapy adoption and regulatory approvals.

Even modest growth rates matter in niche markets: NPC's $1.35B global market in 2024 could balloon to $1.8B by 2030, while ESCC's $2.96B 2034 forecast hinges on sustained adoption of therapies like TEVIMBRA.

Near-Term Catalysts: EU Commercialization and Pipeline Momentum

- EU Approval Imminent: The CHMP's NPC positive opinion (May 2025) is expected to lead to a formal EU approval by Q3 2025, unlocking a €1.2B addressable market for NPC alone.

- ESCC Expansion: Regulatory momentum in the U.S. and EU (already approved) positions TEVIMBRA to capture 30–40% of the first-line ESCC market by 2026.

- Pipeline Synergy: Ongoing trials in head and neck cancer, lung cancer, and pancreatic cancer could expand TEVIMBRA's label further, leveraging its proven efficacy in combination regimens.

Why Buy Now?

BeiGene's oncology portfolio is at a tipping point:

- Clinical Leadership: TEVIMBRA's data outperforms peers in two critical, high-growth tumor types.

- Strategic Execution: Geographic focus aligns with the highest NPC/ESCC burden.

- Valuation: At a P/S ratio of 3.5x (vs. peers at 5.0x+), BeiGeneONC-- offers a rare blend of growth and value.

With regulatory wins, a pipeline rich in near-term catalysts, and markets poised for steady expansion, BEI is a buy. Investors who act now will capitalize on a biotech primed to dominate the next decade of oncology innovation.

Action Item: Acquire shares of BeiGene ahead of the EU NPC approval, with a target price increase of 15–20% by year-end 2025.

Comentarios

Aún no hay comentarios