Beiersdorf's Undervalued Potential Amid Strong Fundamentals and Steady ROE

In the ever-shifting landscape of global equities, contrarian investors often seek opportunities where market sentiment diverges from a company’s intrinsic value. Beiersdorf AG (ETR: BEIG), the German skincare and consumer goods giant, presents such a case. Despite robust fundamentals—including a consistently strong Return on Equity (ROE), disciplined financial management, and outperforming revenue growth—its valuation metrics suggest untapped potential for those willing to look beyond short-term volatility.

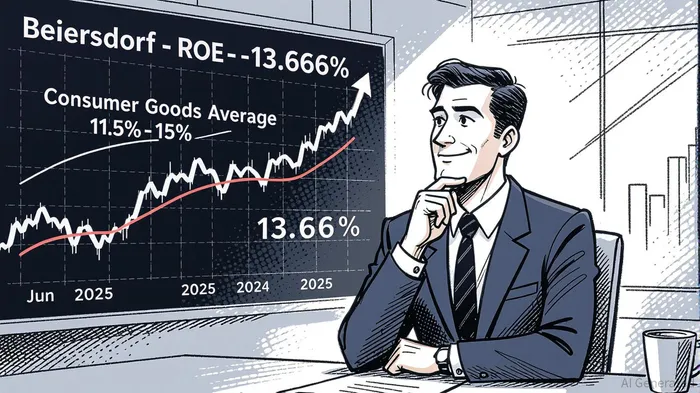

A Decade of ROE Stability and Growth

Beiersdorf’s ROE, a critical metric for assessing capital efficiency, has remained resilient. For the quarter ending June 2025, the company reported an ROE of 13.66%, driven by net income of €1.27 billion and average equity of €9.32 billion [1]. This marks a significant improvement from its 13-year median ROE of 11.58% and outperforms the industry’s typical benchmark of 15–20% [1]. While not in the stratosphere of tech darlings, this ROE underscores Beiersdorf’s ability to generate consistent returns in a sector known for its stable but moderate growth.

Analysts highlight that Beiersdorf’s ROE has remained within a healthy range of 10.4% to 11.03% over the past year, reflecting disciplined capital allocation and operational efficiency [2][3]. For context, the S&P 500 Consumer Staples Sector, a rough proxy for global consumer goods, has a P/E ratio of 22.47 as of September 2025 [4], suggesting that Beiersdorf’s trailing P/E of 25.06 [3] is only modestly premium. This discrepancy hints at a market that may be underappreciating the company’s long-term value.

Valuation Metrics: Contrarian Signals in a Stable Sector

Beiersdorf’s valuation multiples tell a nuanced story. Its Price-to-Book (P/B) ratio of 3.27 [2] appears elevated compared to the industry median of 1.49 [2], but this metric often fails to capture the intangible assets of consumer brands like NIVEA and Eucerin. Meanwhile, its EV/EBITDA of 11.98 [1] lags behind the U.S. soft beverages industry’s 18x multiple [5], a sub-sector that benefits from discretionary spending. Yet, in a world where global consumer goods and FMCG companies trade at an obscured but presumably competitive EV/EBITDA [6], Beiersdorf’s multiple appears conservative.

The company’s balance sheet further strengthens its case. With more cash than debt and gross profit margins of 58.5% [1], Beiersdorf is well-positioned to navigate macroeconomic headwinds—a rarity in today’s inflationary environment.

Analyst Consensus and Growth Catalysts

Despite the cautious valuation, 12 of 20 analysts rate Beiersdorf as a “Buy,” with a 12-month price target average of €136.35—implying a 28% upside from current levels [1]. This optimism is grounded in the company’s recent performance: organic sales grew 6.5% year-to-date 2024, with NIVEA’s 9.4% sales surge demonstrating brand resilience [7]. Analysts also note that Beiersdorf’s five-year revenue growth outpaces peers [1], a testament to its innovation pipeline and market share gains in Asia-Pacific and Latin America.

The Contrarian Case

The contrarian argument rests on two pillars. First, Beiersdorf’s valuation appears unloved by a market fixated on AI-driven or cyclical plays. Its P/E of 25.06 [3] is modest compared to the overvalued S&P 500 Consumer Discretionary Sector (P/E: 30.49) [4], yet it offers the defensive qualities of a staples company. Second, the stock’s P/B ratio, while high, reflects investor skepticism about tangible asset valuations—a bias that may reverse as brand equity gains greater recognition.

Risks and Considerations

No investment is without risk. Regulatory pressures in skincare, raw material costs, and currency fluctuations could temper margins. Additionally, the company’s reliance on the NIVEA brand—accounting for over 40% of sales—introduces concentration risk. However, these challenges are well within the capacity of a company with Beiersdorf’s balance sheet strength and R&D capabilities.

Conclusion

Beiersdorf AG embodies the classic contrarian profile: a company with durable competitive advantages, strong ROE, and conservative valuation metrics that the market has yet to fully price in. For investors with a 3–5 year horizon, the combination of analyst optimism, operational resilience, and a margin of safety makes it a compelling addition to a diversified portfolio. As the consumer goods sector stabilizes post-pandemic, Beiersdorf’s steady hand may prove to be its greatest asset.

Source:

[1] Beiersdorf AG (BDRFF) ROE % [https://www.gurufocus.com/term/roe/BDRFF]

[2] Beiersdorf AG (STU:BEIA) PB Ratio [https://www.gurufocus.com/term/pb-ratio/STU:BEIA]

[3] Beiersdorf AG - PE Ratio [https://www.wisesheets.io/pe-ratio/BEI.DE]

[4] S&P 500 Consumer Staples Sector: current P/E Ratio [https://worldperatio.com/sector/sp-500-consumer-staples/]

[5] United States: EV/EBITDA consumer goods & FMCG 2025 [https://www.statista.com/statistics/1030009/enterprise-value-to-ebitda-in-the-consumer-goods-and-fmcg-sector-in-united-states/]

[6] Global: EV/EBITDA consumer goods & FMCG 2025 [https://www.statista.com/statistics/1030134/enterprise-value-to-ebitda-in-the-consumer-goods-and-fmcg-sector-worldwide/]

[7] Earnings call: Beiersdorf reports robust growth amid challenges [https://uk.investing.com/news/stock-market-news/earnings-call-beiersdorf-reports-robust-growth-amid-challenges-93CH-3753661]

Comentarios

Aún no hay comentarios