Becton, Dickinson and Company (BDX): A Defensive Dividend Play in Undervalued Healthcare Infrastructure

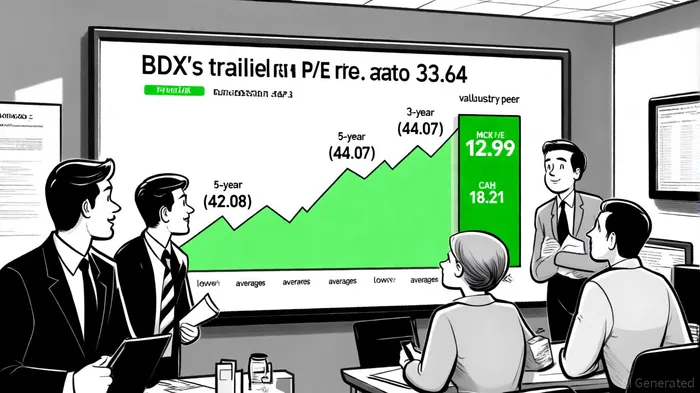

In the evolving landscape of healthcare infrastructure, BectonBDX--, Dickinson and Company (BDX) emerges as a compelling case study for investors seeking undervalued equities with resilient dividend profiles. With a trailing price-to-earnings (P/E) ratio of 33.64 as of September 19, 2025—well below its 3-year average of 42.08 and 5-year average of 44.07—BDX appears to trade at a discount relative to its historical valuation metrics [1]. This divergence is further amplified by the broader sector's compressed valuation multiples, with the healthcare industry's median TEV/EBITDA ratio falling to 12.37x in Q2 2025 from 14.78x in the prior year [2]. While peers like McKessonMCK-- (MCK) and Cardinal HealthCAH-- (CAH) trade at P/E ratios of 20.61 and 18.21, respectively [3], BDX's forward P/E of 12.99 suggests its valuation may be misaligned with its operational strength [1].

A Defensive Dividend Profile Anchored by Creditworthiness and Payout Sustainability

BDX's appeal as a defensive dividend play is underscored by its 2.22% yield, a decade-high level that reflects its status as a Dividend King—having raised payouts for 53 consecutive years [4]. The company's annual dividend of $4.16 per share, paid quarterly, corresponds to a payout ratio of 74.42% based on earnings and 80.62% using cash flow metrics [5]. While the latter figure approaches conservative thresholds for sustainability, BDX's robust free cash flow generation—$1.668 billion in Q2 2025 [6]—and its commitment to returning $1 billion to shareholders by year-end via buybacks [6] reinforce confidence in its ability to maintain and grow distributions.

Credit ratings further bolster the defensive narrative. Despite a recent downgrade from Standard & Poor's to 'BBB+' (from 'A') due to increased debt leverage post-CareFusion acquisition [7], Fitch and Moody's have affirmed BDX's 'BBB' and 'A2' ratings, respectively, with stable outlooks [8]. This bifurcated assessment highlights the company's strong market position in medical devices and healthcare infrastructure, offsetting concerns about short-term leverage [7]. Analysts project dividend growth at an 8% annualized rate over the next five years, driven by aging demographics and rising demand for healthcare services861198-- [4].

Financial Stability and Revenue Resilience in a Challenging Sector

BDX's debt-to-equity ratio of 0.76 as of June 30, 2025—moderate relative to the healthcare sector's 0.92 average [9]—demonstrates prudent capital structure management. This is critical in an industry grappling with policy shifts, tariff disruptions, and margin pressures. For instance, Q2 2025 saw healthcare services sector volatility, including a “Liberation Day” tariff slump, yet BDX's earnings per share (EPS) grew 19% year-over-year to $2.00, with trailing twelve months (TTM) EPS up 13.22% to $5.48 [10]. Such resilience positions BDXBDX-- to outperform peers as the sector navigates regulatory and macroeconomic headwinds.

Revenue growth projections also support the undervaluation thesis. Analysts forecast $21.85 billion in 2025 revenue, with a 7.95% year-over-year increase expected [11]. This growth is underpinned by BDX's diversified portfolio—spanning medical devices, diagnostics, and laboratory equipment—and its strategic acquisitions, which have expanded its footprint in high-growth areas like point-of-care testing.

Conclusion: A Strategic Buy for Income and Growth Investors

BDX's combination of a discounted valuation, defensive dividend profile, and strong financial fundamentals makes it an attractive candidate for investors seeking stability in the healthcare sector. While near-term concerns about debt leverage and sector-wide valuation compression persist, the company's operational efficiency, credit ratings, and long-term earnings growth trajectory suggest its current price may not fully reflect its intrinsic value. With a median price target of $211.44 (13.72% upside from current levels) [12], BDX offers a rare blend of income security and growth potential in an otherwise volatile industry.

Comentarios

Aún no hay comentarios